Michael Saylor’s Strategy built the largest corporate Bitcoin hoard on a single promise: never sell. A new capital framework quietly retires that promise, and the reason it had to is written all over the balance sheet.

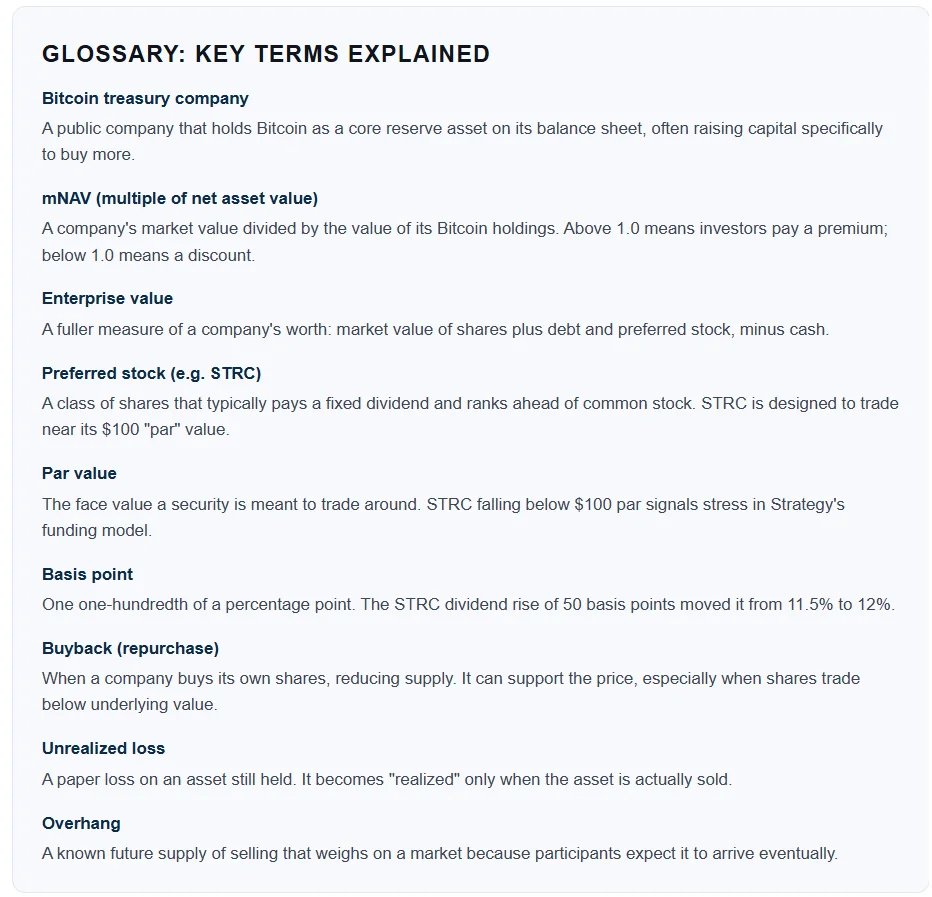

For five years, the loudest voice in corporate Bitcoin had one rule. Michael Saylor would buy Bitcoin, hold Bitcoin, and never sell it. That single line built Strategy Inc. (Nasdaq: MSTR) into the world’s largest corporate Bitcoin holder. On June 29, 2026, that rule changed. The company unveiled a “Digital Credit Capital Framework” that, for the first time, formally authorizes the sale of up to $1.25 billion of Bitcoin to fund dividends, interest, and buybacks.

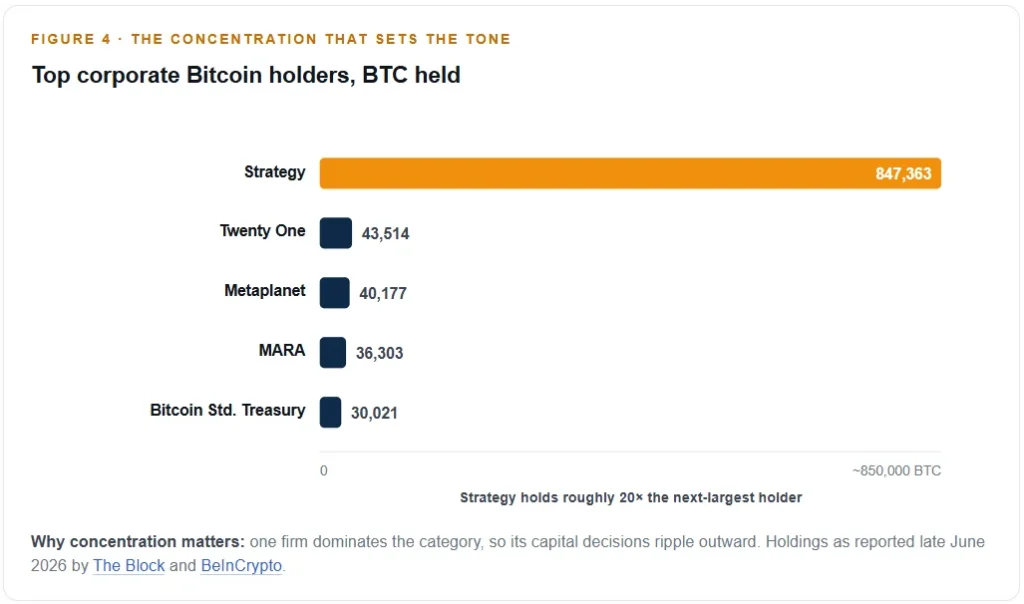

This Bitcoin monetization plan matters far beyond one company. Strategy holds more Bitcoin than the next nineteen public treasury firms combined, so its choices set the tone for an entire sector. To understand why a self-described “diamond hands” investor would build a selling mechanism at all, you have to follow the money through a balance sheet under real strain. Let us demystify what changed, why it changed, and what investors and students should watch next.

In Summary

The “never sell” era is over. Strategy’s new Bitcoin monetization plan authorizes the sale of up to $1.25 billion in BTC to fund obligations, though it does not commit the firm to any sale.

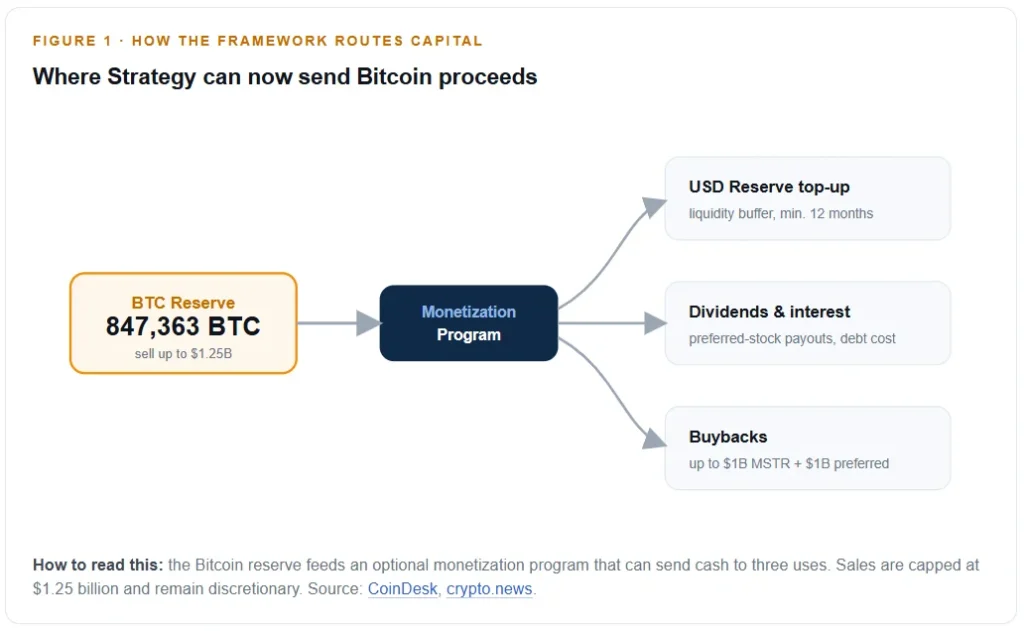

The trigger is a broken premium. Strategy’s mNAV fell below 1.0 for the first time, meaning the market values the company at less than the Bitcoin it owns. That ended the cheap-financing advantage that powered years of buying.

Bitcoin is near $58,500 on June 30, 2026, roughly 53% below the October 2025 record of about $126,000, leaving most of Strategy’s recent purchases underwater.

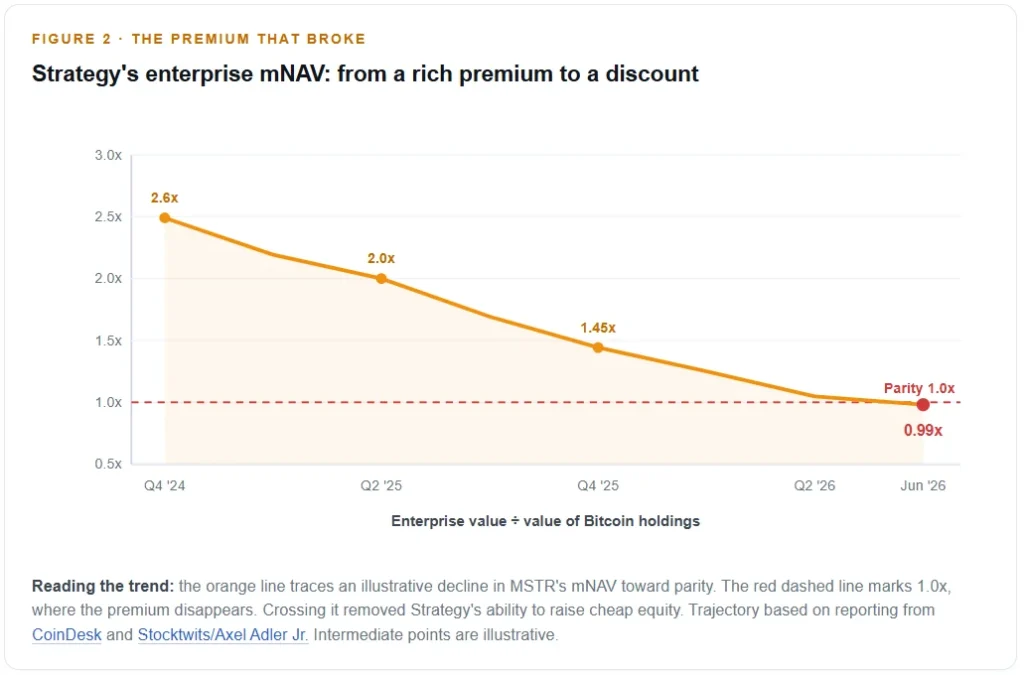

Liquidity is the real story. A $2.55 billion USD reserve plus the new $1.25 billion BTC capacity gives Strategy about 25.9 months of dividend and interest coverage.

Contagion risk is sector-wide. With 199 public companies now holding Bitcoin, a leader trading below its coins tests the entire treasury-company model.

Table of Contents

- Table of contents will be generated automatically when the page loads.

What Strategy actually announced

The headline number is $1.25 billion for a “BTC Monetization Program.” However, the announcement is broader than a single sale limit. Strategy introduced a layered capital plan with several moving parts, and reading them together is the only way to grasp the intent.

First, the company can now sell Bitcoin to top up its USD Reserve, cover dividend and interest payments, and fund buybacks of its securities. Second, it authorized two repurchase programs of up to $1 billion each, one for common stock (MSTR) and one for its preferred “Digital Credit” securities. Third, it raised the dividend on its STRC preferred shares to 12% annually, effective July 2026.

Crucially, the plan authorizes rather than commits. CFO Andrew Kang framed the Bitcoin program as a tool, not a directive. In other words, Strategy is buying optionality. Furthermore, Saylor stressed that Bitcoin remains the firm’s primary treasury reserve asset, positioning the change as disciplined capital management rather than surrender.

Why the “never sell” promise had to bend

To see why this Bitcoin monetization plan appeared now, follow one metric: mNAV. This ratio compares a Company’s market value to the value of the Bitcoin it holds. For years, MSTR traded at a large premium to its coins, sometimes well above 2x. That premium was the engine of the whole model.

The flywheel that stopped spinning

Here is the mechanism in plain terms. When MSTR’s shares trade above the value of its Bitcoin holdings, the company can issue new stock, raise cash above “fair” value, and buy more Bitcoin. That raises Bitcoin per share, supporting the premium and enabling the next raise. Analysts called this the “flywheel”. Therefore, the premium was not a vanity metric. It was the funding source.

In late June 2026, the flywheel jammed. Strategy’s enterprise mNAV fell below 1.0, slipping to about 0.99 and lower on some readings. Consequently, issuing new shares now means selling equity at a discount to the value of the underlying Bitcoin, which destroys value for existing holders rather than creating it. When the cheap-financing tap closes, a company still owing dividends needs another source of cash. That source is the Bitcoin itself.

Bitcoin’s price did the rest

The premium collapse did not happen in a vacuum. Bitcoin sat near $58,500 on June 30, 2026, according to Fortune’s daily price tracker. That is roughly 53% below the October 2025 all-time high near $126,000. Because Strategy’s average purchase price sits around $75,651 per coin, its more recent buying tranches now show unrealized losses of roughly $10.6 billion. A falling asset and a vanishing premium hit the funding model from both sides at once.

The liquidity math behind the decision

Strip away the narrative and the framework is a liquidity exercise. Preferred-stock dividends and debt interest are fixed obligations. They do not pause when Bitcoin falls. So Strategy needs reliable cash to meet them, and it has now stacked several layers to do so.

The company reports a USD Reserve of about $2.55 billion, which it says covers roughly 17.4 months of preferred dividends and interest on its own. Add the newly authorized $1.25 billion of Bitcoin selling capacity, and management says total coverage rises to about 25.9 months, per CCN and cryptonews.net. The reserve carries a floor: it must stay at a minimum of 12 months of coverage.

The STRC pressure point

One security explains much of the urgency. STRC is a preferred stock designed to trade near its $100 par value while paying a high yield. When Bitcoin fell below $60,000, STRC collapsed to about $71, well under par. That break matters because Strategy funds itself partly by issuing STRC. Once it trades below par, that channel narrows. Raising the dividend to 12% is an attempt to pull STRC back toward $100, but a richer dividend also means a larger cash bill, which loops back to the need for liquidity.

The debate: discipline or capitulation?

Reasonable analysts read this move in opposite directions. Both readings deserve a fair hearing because the framework genuinely supports either interpretation depending on what happens next.

The bullish reading: removing an overhang

Supporters argue the plan strengthens the company. Crypto analyst Ran Neuner said authorizing sales actually removes a major uncertainty, because the market no longer has to fear a disorderly, forced liquidation later. Grayscale research head Zach Pandl had earlier urged Strategy to sell Bitcoin to meet cash needs. By this logic, a controlled, capped selling tool is a sign of maturity, not weakness. Notably, the market reacted well at first: MSTR jumped about 13% on the news, its biggest one-day gain in four months.

The bearish reading: the model is cracking

Critics see something more serious. Ripple CEO Brad Garlinghouse has argued that issuing securities to buy Bitcoin does not create lasting value. Longtime Bitcoin skeptic Peter Schiff warned that the company might eventually have to sell coins to fund buybacks. More pointedly, analyst Charles Edwards of Capriole Investments has called the broader treasury-company chart a “textbook bubble”, while cautioning that STRC, unlike an algorithmic stablecoin, is backed by a real balance sheet. The bear case is simple: a company built on never selling has now built the machinery to sell.

“Strategy remains committed to Bitcoin as its primary treasury reserve asset. At the same time, Digital Credit requires liquidity, discipline, and active capital management.”

-Michael Saylor, Executive Chairman, Strategy Inc., June 29, 2026

Why this echoes across the whole sector

Strategy is not an isolated case. It is the anchor of a category. As of late June 2026, 199 public companies held Bitcoin on their balance sheets, together owning around 1.26 million BTC. Because Strategy holds about 20 times as much Bitcoin as the next-largest firm, its behavior effectively sets the playbook for everyone else.

The same pressure is visible down the league table. Japan’s Metaplanet, the second-largest corporate holder, saw its stock fall roughly 85% over twelve months and is now pivoting toward Bitcoin-yield products to survive. Tether-backed Twenty One Capital fell from about $47 to $5.50. The shared thread is the financing edge, not belief in Bitcoin. When a treasury company’s premium disappears, fresh equity stops paying for itself, and the entire accumulation model has to adapt.

What investors and students should watch next

This story is not settled. It is a live test of whether the corporate Bitcoin model can survive its first sustained downturn without the premium that built it. A few clear signals will tell you which way it resolves.

First, watch whether Strategy actually sells. Authorization is not an action. If the company taps the program lightly or not at all, the bullish “optionality” reading gains ground. Heavy use would suggest cash pressure is winning. Second, watch the mNAV and the STRC price. A return of STRC toward $100 and MSTR back above its Bitcoin value would ease contagion fears. Third, watch Bitcoin’s price itself, since everything above ultimately keys off it. A recovery repairs balance sheets across all 199 holders; further weakness deepens the strain.

For students of finance, the lesson is cleaner than any price target. A strategy that depends on a premium is only as durable as that premium. Leverage and reflexivity work beautifully on the way up and painfully on the way down. Strategy’s new framework is, at heart, an admission that even the most committed holder needs a cash plan when the market stops paying a premium for conviction.