Solana’s spot ETFs are attracting institutional capital, and its network is processing billions in trading volume. Yet the SOL token keeps sliding. Here is what explains the disconnect, and what could fix it. Solana presents one of the most puzzling contradictions in crypto today. Its spot ETFs are attracting institutional money. Its network is processing billions in volume. Yet the SOL token keeps sliding. So what explains this disconnect, and what would it take to fix it?

This analysis breaks down the gap between network success and token performance. Moreover, it explains the tokenomics debate now unfolding in the open. The goal is simple: help investors, students, and curious readers understand exactly why a thriving blockchain can host a struggling asset.

In Summary

Solana’s network is booming, but the token is not. SOL fell from the $76 to $98 range into the mid-$60s during May and early June 2026, even as ETF assets crossed $1 billion.

Activity does not equal value capture. Fees, stablecoins, tokenized equities, and ETF flows reward validators, issuers, and platforms before they reach SOL holders.

Inflation is the core bear case. Solana mints roughly 60,000 SOL daily but burns only about 648, so dilution remains a structural headwind.

Two reform proposals aim to close the gap. SIMD-0550 targets inflation, while SIMD-0547 targets weak fee burn. Both face validator uncertainty.

Macro pressure amplified the drop. The record SpaceX IPO pulled capital toward equities, repricing high-beta assets like SOL and Bitcoin.

Recovery has started. By June 18, 2026, SOL had climbed back to roughly $73.79, showing the selloff may have been partly cyclical.

The Core Contradiction: Strong Network, Weak Token

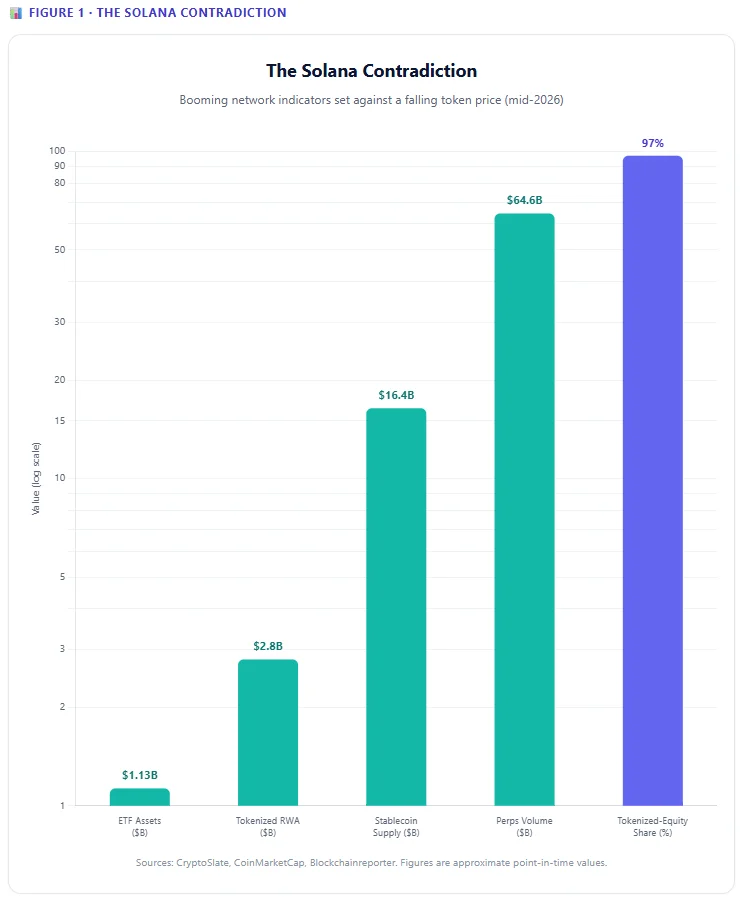

Let’s start with the numbers that make Solana so confusing. By late May 2026, Solana spot ETF assets crossed $1 billion. Furthermore, cumulative inflows reached about $1.13 billion by mid-June, according to data tracked on CoinMarketCap. Solana ETFs also posted their best month of 2026 in May, led by Bitwise, while Bitcoin and Ethereum funds saw heavy outflows.

The on-chain story looked equally strong. Tokenized real-world assets on Solana surpassed $1 billion in market cap, and stablecoin supply crossed $16 billion. In addition, Solana dominated on-chain tokenized-equity trading, capturing roughly 97% of cumulative spot volume in that niche.

Yet the token told a different story. SOL slid toward the mid-$60s in early June. So why did the price ignore the fundamentals? The answer, according to Jake Kennis, senior research analyst at Nansen, is that activity does not equal value capture.

Here’s how the disconnect looked at the time of the original reporting. The chart below contrasts thriving network metrics against a sliding token price.

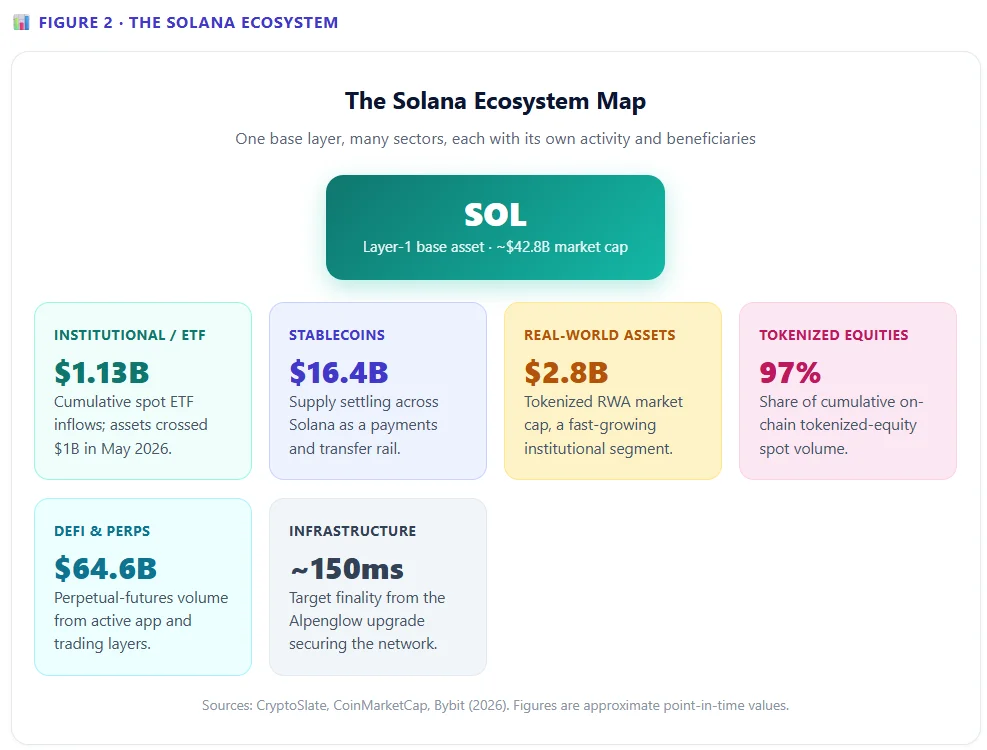

The Solana Ecosystem at a Glance

Before unpacking the price puzzle, it helps to see the full ecosystem that sits behind it. Solana is not a single product. Rather, it is a base layer that supports many distinct sectors, each generating its own activity and revenue. The map below shows the major pillars and a headline figure for each.

Notice a pattern. Every pillar feeds the network, yet each one routes value to a different group first. That structure is exactly what creates the value-capture gap we explore next.

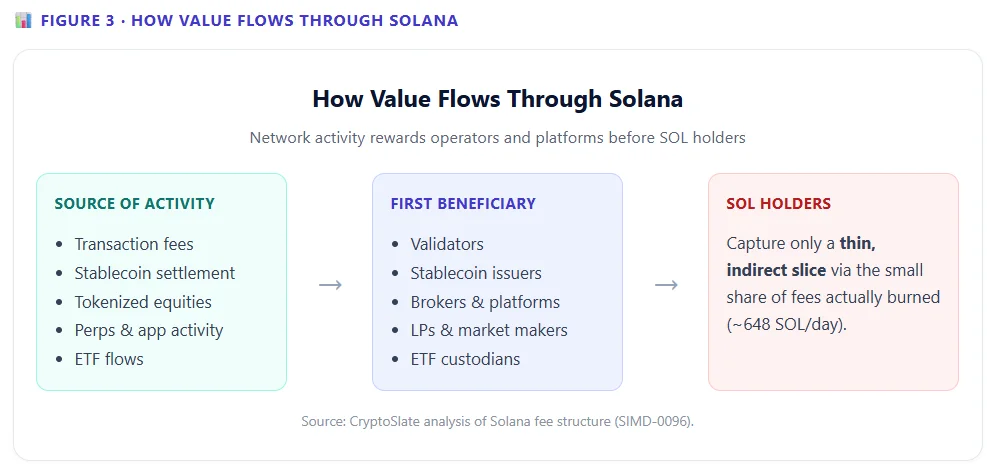

Why Network Activity Skips SOL Holders

To understand the gap, you need to follow the money. On Solana, most network revenue reaches other parties before it ever touches SOL holders. Therefore, the headline activity numbers overstate the value flowing to the token itself.

Consider stablecoin settlement. Users can move $16 billion in stablecoins while holding only the tiny amount of SOL needed to pay transaction fees. Likewise, tokenized equity trading rewards brokers and platforms, not token holders. App revenue, meanwhile, accumulates at the protocol and frontend layer.

The fee structure makes this concrete. Solana splits base fees evenly: 50% burned, 50% to block producers. However, priority fees, which dominate during busy periods, flow entirely to validators after a change called SIMD-0096. As a result, a high-traffic day routes most of the fee revenue to validators, while the burn stays flat.

The diagram below maps how value moves through Solana, showing why SOL capture stays indirect.

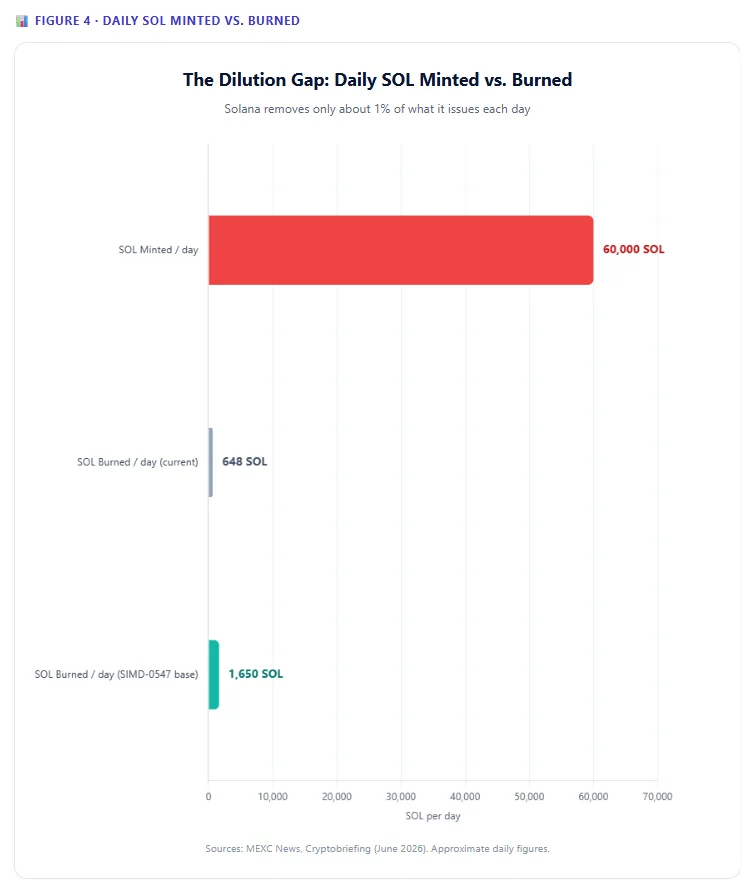

The Inflation Problem at the Heart of the Bear Case

Now we reach the strongest argument against SOL. Ryan Day, CMO of Solstice, points to Solana’s tokenomics as the structural weak spot. The network launched with an 8% initial inflation rate, a 15% annual disinflation rate, and a 1.5% long-term floor.

As of June 2026, inflation sits at 3.82%. That figure is well below the original 8% but still years from the floor. Under the current schedule, terminal inflation arrives in roughly 5.7 years. Throughout that period, supply keeps growing.

The imbalance becomes stark when you compare minting against burning. Solana mints about 60,000 SOL per day but burns only around 648. In other words, the network removes barely 1% of what it creates. Consequently, dilution becomes the dominant force regardless of how busy the chain gets.

The chart below visualizes this gap. Notice how small the burn looks next to daily issuance.

Day also pushes back on one common criticism. Solana often gets singled out for its memecoin reputation, driven by platforms like Pump.fun. However, he argues that every major chain chased the same memecoin cycle, including Ethereum, Base, and BNB Chain. The inflation critique rests on hard numbers. By contrast, the memecoin critique is more of a reputational hangover.

The Macro Layer: A Record IPO Drains Liquidity

Tokenomics explain the structural pressure. Yet timing matters too, and the macro backdrop turned hostile in June 2026. The driving force was the largest IPO in history.

SpaceX priced its IPO after market close on June 11, 2026, and debuted on the Nasdaq the next day. The company targeted a $1.75 trillion valuation and a $75 billion raise at $135 per share. Demand was enormous. By June 9, the deal had attracted more than $250 billion in investor interest, roughly three to four times the target.

When capital of that scale moves to market, risk assets reprice to raise cash. SOL absorbed that pressure alongside Bitcoin, which traded near $61,500 at the time of the original article’s publication. The SpaceX stock then surged 19% on its first day, reaching about $171.91 by June 15. A strong debut tends to keep speculative capital parked in equities for longer.

Notably, more mega-cap listings are queued behind it, including OpenAI and Anthropic. Each one extends the period during which capital stays rotated away from crypto. The timeline below maps how this liquidity event unfolded.

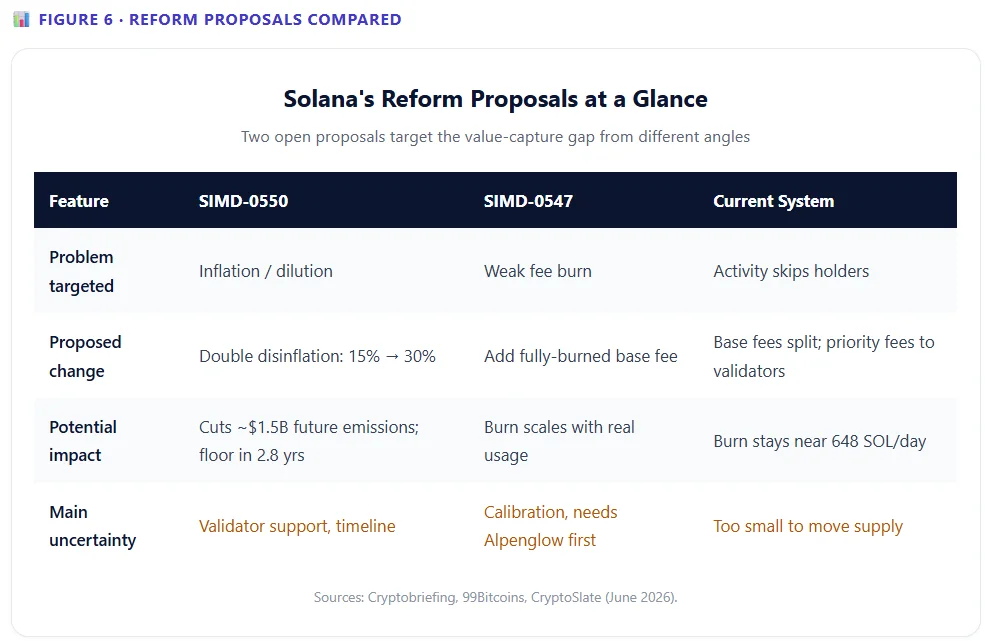

What the Community Is Voting On

Here’s the encouraging part. Solana’s community is not ignoring these problems. Instead, developers have put forward two reform proposals that directly target the value-capture gap. Both are being debated openly.

The first is SIMD-0550, submitted by a Helius engineer. It proposes doubling the annual disinflation rate from 15% to 30%. This change would compress the path to terminal inflation from 5.7 years to about 2.8 years. At current prices, backers estimate it would eliminate roughly $1.5 billion in future SOL emissions. Solana co-founder Anatoly Yakovenko has publicly backed the direction.

The second is SIMD-0547, introduced by a developer known as cavemanloverboy. It adds a resource-based base fee that gets fully burned. Importantly, the burn would scale with real network consumption. Current estimates suggest the daily burn could rise from 648 SOL to between 1,500 and 1,800 SOL under normal conditions. During heavy network stress, one researcher calculated burns could climb to between 10,800 and 64,800 SOL if activity rose sharply.

However, neither proposal is a sure thing. History offers a warning. An earlier inflation proposal, SIMD-0228, went to a vote in March 2025 and failed. Only 61% of validator stake voted in favor, short of the 66.67% supermajority required. The reason is straightforward: validators earn revenue from inflation, so they have an incentive to resist cuts. Token holders, meanwhile, prefer less dilution. That tension sits at the center of every Solana governance fight.

The comparison below summarizes both proposals and the status quo.

One practical detail matters here. SIMD-0547 can only activate after the Alpenglow consensus upgrade, Solana’s major protocol rewrite targeting roughly 150-millisecond finality. No activation timeline has been set. Therefore, even broad support could leave the proposal waiting in the queue.

Signs of Recovery: The Price Bounce

The original CryptoSlate analysis captured a moment of deep pessimism, with SOL near $63. Since then, however, the picture has improved. By June 18, 2026, SOL had recovered to about $73.79, with a market cap near $42.83 billion, according to Bybit data. That marks a meaningful bounce off the early-June lows.

This recovery supports a key idea from the original reporting. Much of the selloff reflected macro risk-off pressure rather than a permanent verdict on Solana. Assets with documented real usage often reprice first when risk appetite returns. The chart below tracks SOL’s path through this volatile period.

The Bottom Line: What Investors Should Watch

So where does this leave Solana? The chain has built something real. It now hosts institutional ETF demand, settlement rails for stablecoins, and dominance in tokenized equities. Despite all that, the SOL token captures only a shrinking share of the value of that activity.

Two paths now lie ahead. On the bullish side, macro liquidity could return as the IPO wave clears. Meanwhile, SIMD-0550 and SIMD-0547 could move toward activation. If both happen, SOL gains a credible route to re-rating through lower future dilution and higher burn per unit of activity. On the bearish side, the reforms could stall. In that case, inflation stays the dominant force, and the contradiction deepens.

For investors and students alike, the lesson is broader than one token. A blockchain can succeed as infrastructure, even as its native asset struggles to capture that success. The crucial question for Solana is whether its tokenomics can evolve to reward the holders who fund its security. Proving that SOL captures what the network is becoming is exactly what the market is now waiting to see.