From a wheat farmer’s handshake deal to a $700 trillion global market, derivatives are everywhere. This guide explains what they are, why they exist, and why every investor needs to understand them.

Table of Contents

- Table of contents will be generated automatically when the page loads.

In Summary

A derivative is a financial contract whose value comes from an underlying asset such as a stock, currency, commodity, or interest rate index.

The four main types are forwards, futures, options, and swaps. Each suits different needs and risk profiles.

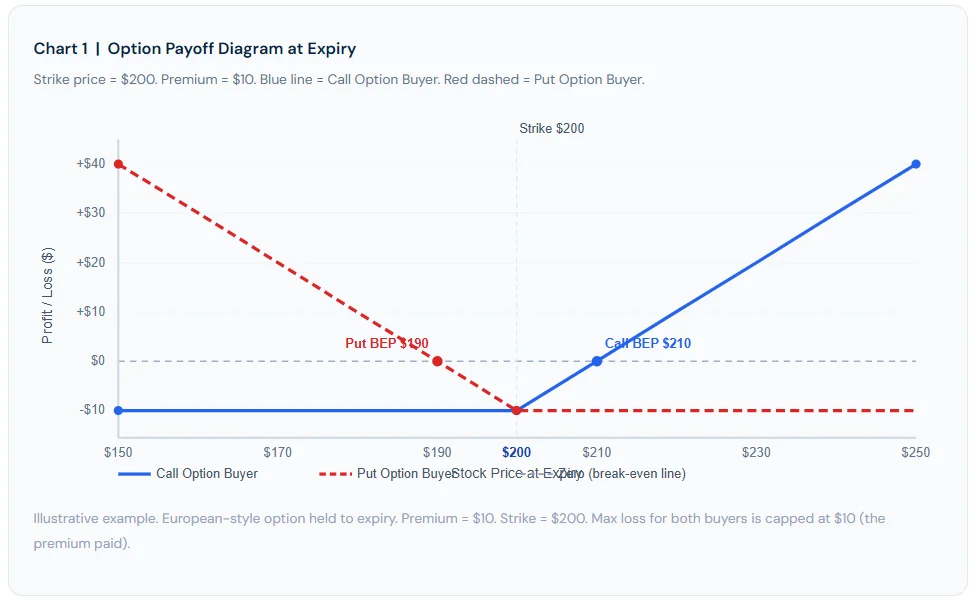

Options uniquely cap the buyer’s maximum loss at the premium paid. This makes them powerful tools for managing downside risk.

Derivatives serve three core purposes: hedging risk, enabling speculation, and supporting price discovery in financial markets.

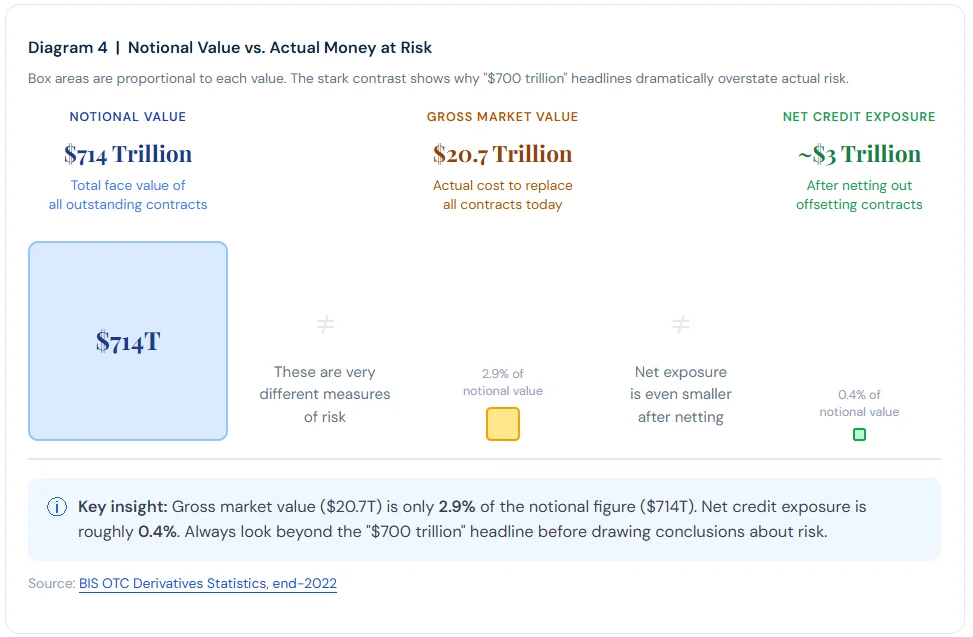

The global OTC derivatives market has a notional value of approximately $714 trillion (BIS, end-2022). However, gross market value is only about $20.7 trillion. Net credit exposure is smaller still.

Notional value and market value are entirely different measures. Always check both before drawing any conclusions about risk.

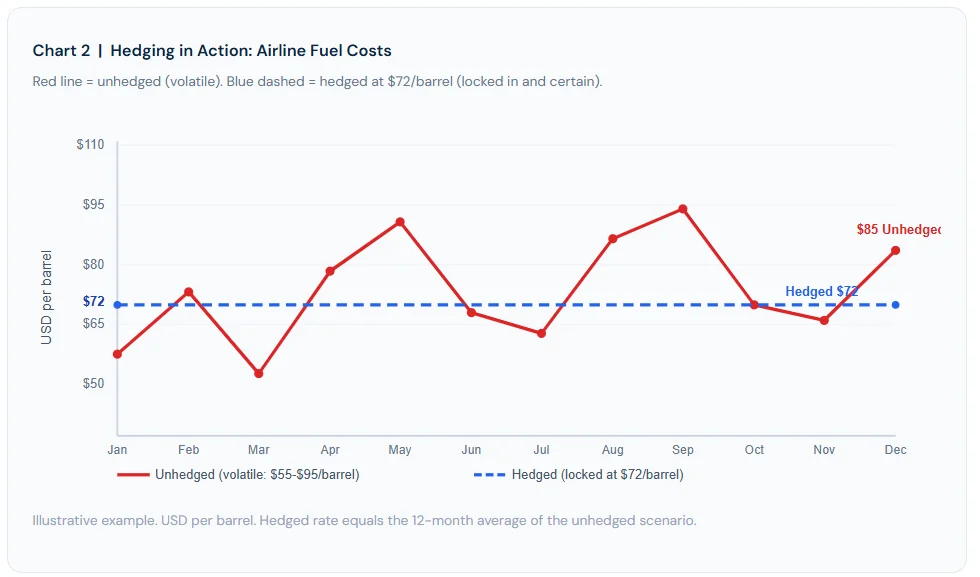

Hedging smooths out uncertainty. Locking in a price eliminates volatile swings in operating costs, as shown in the airline fuel example.

Derivatives can amplify both gains and losses. Their danger lies in misuse, excessive leverage, and opaque OTC markets, not in the instruments themselves.

A Farmer, a Merchant, and a Simple Deal

Picture a wheat farmer in rural Kansas. It is early spring. The harvest is months away. However, the farmer worries: what if wheat prices crash before October? A merchant faces the opposite concern. What if prices rise sharply and wheat becomes too expensive to buy?

So they strike a deal. The farmer agrees to sell 1,000 bushels of wheat at $5 per bushel in three months. The merchant agrees to buy at that price. Both parties now have certainty about the future. This simple agreement is the world’s oldest derivative contract.

Today, that same logic underpins a global market worth hundreds of trillions of dollars. According to the Bank for International Settlements (BIS), the global over-the-counter (OTC) derivatives market held a notional value of approximately $714 trillion at end-2022. That figure dwarfs the entire world economy many times over.

What Exactly Is a Derivative?

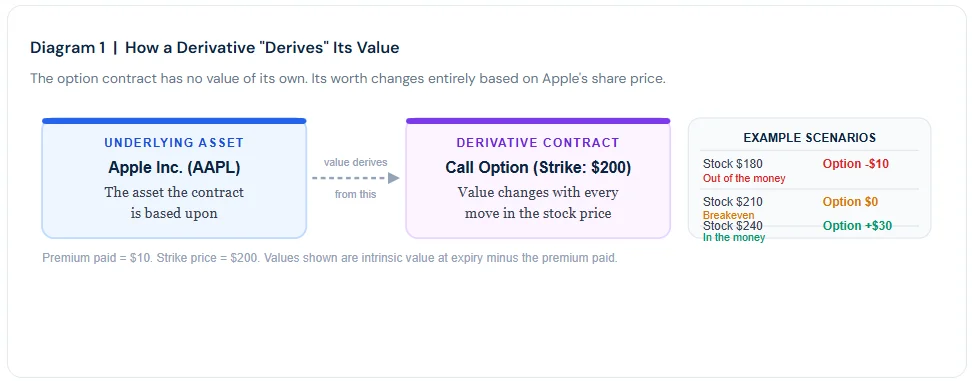

A derivative is a financial contract whose value depends on an underlying asset. This asset can be almost anything. It can be a stock, a bond, a currency, a commodity like oil or gold, or even an interest rate index.

Think of it this way. A derivative does not own the underlying asset. Instead, it draws its value from that asset’s price movements. The word “derive” is the key. The contract derives its value from something else entirely.

A derivative is “a contract between two or more parties whose value is based on an agreed-upon underlying financial asset, index, or security.” The interactive widget below makes this relationship concrete.

The Four Building Blocks of Derivatives

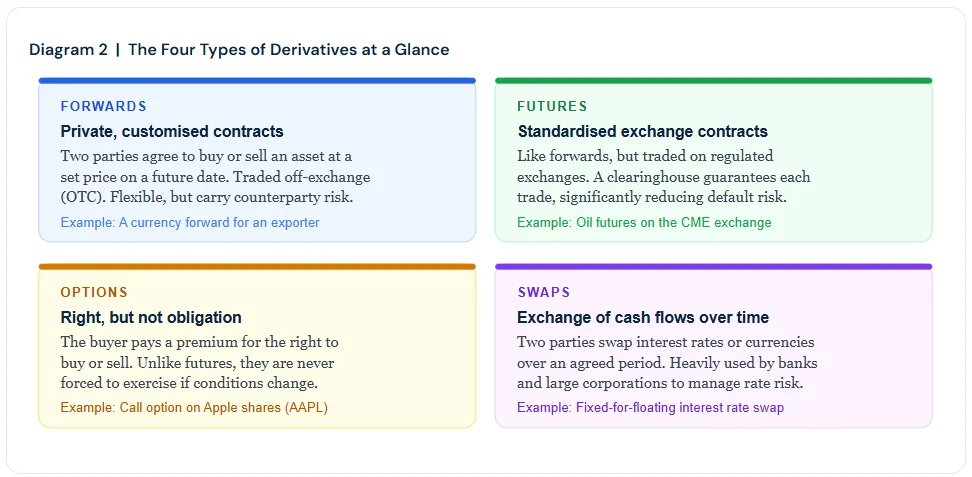

Derivatives come in four main forms. Understanding these forms builds a strong foundation for everything in this series. Each type serves a distinct purpose and suits different market participants.

Forwards

A forward contract is a private agreement between two parties. They agree to buy or sell an asset at a specific price on a future date. Forwards are customisable and trade outside official exchanges. This provides flexibility, but it creates counterparty risk. One side could potentially default on its obligations.

Futures

Futures are similar to forwards, but they trade on regulated exchanges. The Chicago Mercantile Exchange (CME) is one of the world’s largest futures markets. A central clearinghouse stands between buyer and seller. Therefore, the risk of default is significantly lower than that of forwards.

Options

An option gives the buyer the right, but not the obligation, to buy or sell an asset at a set price before a specific date. The buyer pays a fee called a premium for this flexibility. The Chicago Board Options Exchange (CBOE) first standardised options trading in 1973. This transformed access for ordinary investors worldwide. The payoff diagram below shows how an option’s profit and loss changes with the asset price.

Swaps

A swap involves two parties exchanging cash flows over time. The most common type is an interest rate swap. One party pays a fixed interest rate while the other pays a variable rate. Banks and corporations use swaps extensively. They help manage exposure to changing interest rates and foreign currencies. According to ISDA’s 2024 Annual Review, interest rate swaps continue to account for the largest share of global derivatives activity by notional value.

Why Do Derivatives Exist?

Derivatives serve three core purposes in financial markets. Each purpose addresses a real-world need for investors, businesses, and the broader economy.

1. Hedging: Reducing Risk

Hedging means using a derivative to reduce an existing risk. Airlines, for instance, use oil futures to lock in fuel prices for the coming months. This protects them from sudden price spikes. Consequently, companies gain greater certainty over their future costs. The interactive chart below shows the impact of hedging on an airline’s fuel costs.

2. Forward Contract: Who Wins in Each Scenario?

The farmer-and-merchant example illustrates a classic forward contract. However, who actually benefits depends on where prices end up. The three scenarios below clarify this important point. Additionally, they reveal why both parties willingly enter the deal: each values certainty over the uncertain chance of a better outcome.

3. Speculation: Profiting From Price Movements

Some investors use derivatives to profit from expected price changes. They do not own the underlying asset. Instead, they bet on the direction of its price. Speculation adds vital liquidity to markets. However, it also amplifies risk when used without proper discipline and risk management.

4. Price Discovery: Signalling the Future

Derivatives markets reflect the beliefs of millions of participants about future prices. Gold futures, for instance, signal what traders expect gold to be worth in six months. Therefore, they help establish fair market prices and give businesses valuable information for planning ahead.

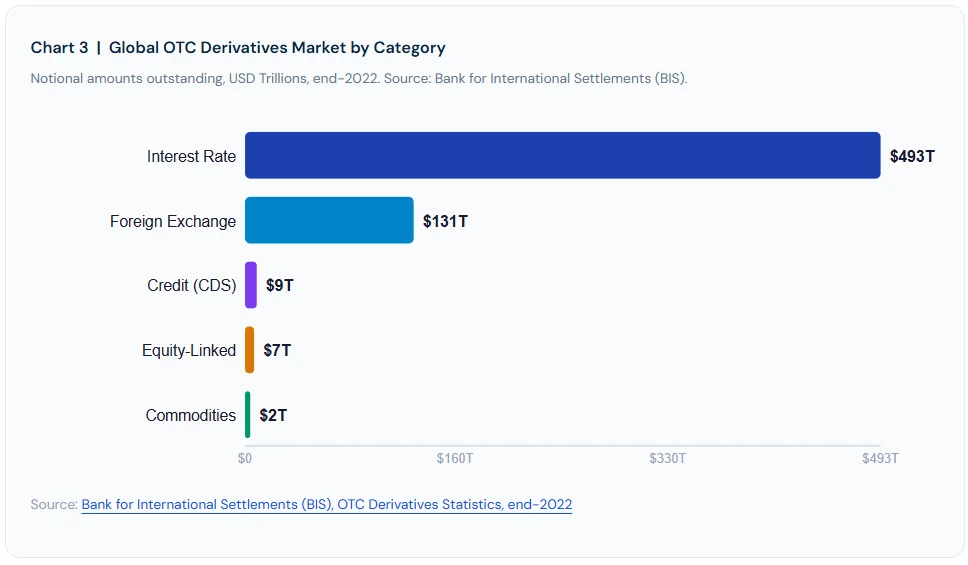

How Big Is the Derivatives Market?

The derivatives market is the largest financial market in the world. According to the BIS OTC Derivatives Statistics, interest rate derivatives dominate the market, followed closely by foreign exchange derivatives. The chart below shows the full composition by notional value.

However, it is critical to distinguish between notional value and actual money at risk. Notional value represents the total face value of all contracts. The actual funds at stake are far smaller. The BIS reports that gross market value stood at approximately $20.7 trillion at end-2022. After netting, the net credit exposure is smaller still. The visualisation below makes this size difference dramatically clear.

Therefore, always look beyond the headline number when reading about derivatives. Many media reports exaggerate risk by citing notional values alone. Furthermore, the net credit exposure figure most closely reflects systemic risk in the system.

A Brief History: From Grain to Global Finance

Derivatives are far from a modern invention. Historians trace derivative-like contracts back to ancient Mesopotamia and classical Greece. However, the modern derivatives market truly began in Chicago in the mid-nineteenth century.

The Chicago Board of Trade (CBOT), founded in 1848, was the world’s first organised futures exchange. It standardised grain contracts and transformed agricultural commerce. Modern financial derivatives emerged in the early 1970s. The collapse of the Bretton Woods fixed exchange rate system in 1971 created severe currency volatility. Additionally, rising inflation made interest rates unpredictable. As a result, banks and corporations urgently needed new risk management tools.

Are Derivatives Dangerous?

Derivatives have earned a reputation for danger. The celebrated investor Warren Buffett once called them “financial weapons of mass destruction” in his 2002 letter to Berkshire Hathaway shareholders. That warning gained enormous relevance during the 2008 global financial crisis.

“Derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal.”

-Warren Buffett, Berkshire Hathaway Annual Letter, 2002

Credit default swaps (CDS) played a central role in the 2008 crisis. These instruments allowed banks to bet on mortgage defaults without owning the underlying mortgages. When the US housing market collapsed, these bets went catastrophically wrong. Additionally, the opacity of OTC markets made it nearly impossible to measure total losses in real time.

However, derivatives themselves are neutral instruments. Their danger lies entirely in misuse, excessive leverage, and inadequate regulation. Used correctly, they remain essential tools for managing financial risk. We will explore this tension in much greater depth in Articles 4 and 5 of this series.

Who Uses Derivatives?

Derivatives markets attract a wide range of participants. Each group enters the market for a different reason. Understanding these participants helps clarify how the market functions as a whole.t functions as a whole.

Specifically, each group plays a distinct and complementary role. Hedgers bring real economic needs to the market. In contrast, speculators provide the liquidity that hedgers need to transfer their risk. Similarly, arbitrageurs keep prices aligned across markets and exchanges. Consequently, all three groups make the derivatives market function efficiently and fairly.

Glossary of Key Terms

Derivative

In essence, a derivative is a financial contract whose value is based on an underlying asset, index, or interest rate. The contract derives its value from price movements in that asset.

Underlying Asset

Specifically, this is the financial asset underlying a derivative contract. Examples include stocks, bonds, currencies, commodities, and interest rates.

Forward Contract

In practice, a forward is a private, customised agreement to buy or sell an asset at an agreed price on a future date. It is traded OTC, not on a regulated exchange.

Futures Contract

By contrast, a futures contract is standardised and traded on a regulated exchange. A clearinghouse guarantees performance, significantly reducing default risk.

Option

In short, an option gives the buyer the right (not the obligation) to buy or sell an asset at a set price. To obtain this right, the buyer pays a premium upfront.

Strike Price

Also known as the exercise price, this is the pre-agreed price at which an option buyer may buy or sell the underlying asset.

Premium (Options)

Simply put, this is the fee paid upfront by the option buyer. It is non-refundable regardless of whether the option is eventually exercised.

Swap

In essence, a swap is a contract in which two parties exchange cash flows over a period. Common types include interest rate swaps and currency swaps.

Notional Value

Specifically, this is the face value of a derivatives contract. It represents the total size of the position but does not reflect the actual money at risk.

Gross Market Value

By contrast, gross market value is the actual cost of replacing all outstanding contracts at current prices. It is a far more accurate measure of real risk than notional value.

Hedging

In practice, hedging means using a financial instrument such as a derivative to reduce the risk of adverse price movements in an asset or liability.

OTC (Over the Counter)

In other words, OTC trading occurs directly between two parties, outside a formal exchange. It offers flexibility but carries greater counterparty risk.

Counterparty Risk

Simply put, this is the risk that the other party in a contract will fail to fulfil their obligations. It is generally higher in OTC markets than on regulated exchanges.

Clearinghouse

In practice, a clearinghouse is an intermediary that stands between buyer and seller in exchange-traded markets. It guarantees performance and reduces default risk for both sides.

In/Out of the Money

Specifically, these terms describe an option’s intrinsic value. A call option is “in the money” when the stock price exceeds the strike price, and “out of the money” when it is below it.