In March 2023, one of America’s biggest banks vanished over a weekend. On Wednesday, it looked healthy. By Friday, regulators had seized it. The story of Silicon Valley Bank is a clean lesson in how interest rates, bonds, accounting, and human panic connect.

In Summary

Banks borrow short and lend long. That maturity mismatch is the core fragility.

Bond prices fall when interest rates rise, and long-dated bonds fall hardest.

Held-to-maturity accounting hid about $15bn of losses, near SVB’s entire $16bn equity.

Selling bonds turned a hidden paper loss into a real $1.8bn loss, which sparked the run.

With 94% of deposits uninsured, customers pulled $42bn in a single day.

Solvency and liquidity differ. A solvent bank can still fail without ready cash.

Regulators backstopped deposits and launched the Bank Term Funding Program to stop contagion.

Table of Contents

- Table of contents will be generated automatically when the page loads.

Silicon Valley Bank, known as SVB, held more than $200 billion in assets. It was the 16th largest bank in the United States. Yet a sudden wave of withdrawals destroyed it in barely two days. How can a giant fall so fast? The answer demystifies several core ideas in economics. Let us unpack them, one step at a time.

First, how a bank actually works

Picture what a bank really does. It takes deposits from customers. Then it lends or invests most of that money. Crucially, deposits can be withdrawn at any moment. However, loans and bonds stay locked away for years. Economists call this maturity transformation. In plain words, a bank borrows short and lends long.

This model is useful, yet fragile. It works only as long as most depositors stay calm. SVB pushed the risk to an extreme. By the end of 2022, it held about $120 billion in bonds. Meanwhile, it owed roughly $173 billion to depositors, against just $16 billion of equity.

The trigger: cheap money turned expensive

Now follow the wider backdrop. During the pandemic, money was cheap. Interest rates sat near zero. Tech startups raised huge sums and parked the cash at SVB. So the bank’s deposits more than tripled in two years. SVB poured that flood into long-term government bonds.

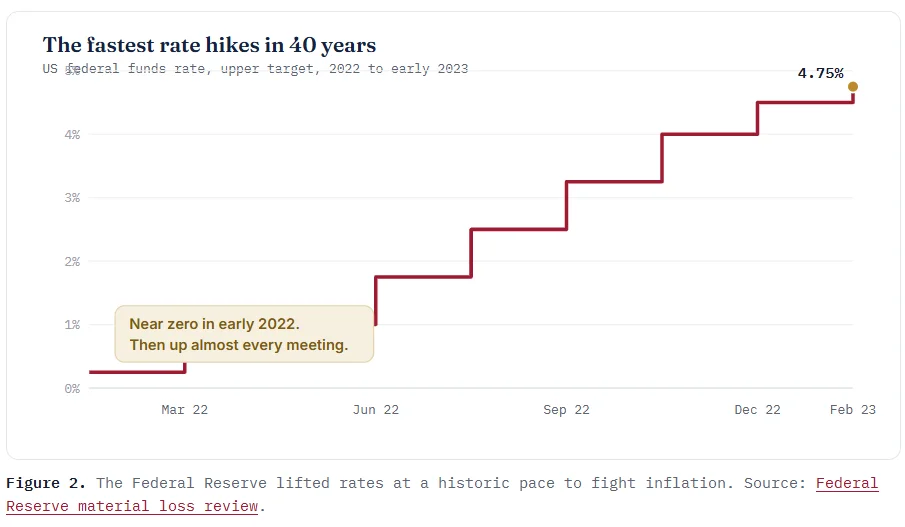

Then inflation arrived. To cool it, the Federal Reserve raised rates rapidly. The federal funds rate climbed from about 0.25% in March 2022 to 4.75% by early 2023. Furthermore, that was the steepest pace in four decades. This is monetary policy at work. Higher rates slow spending, yet they also reprice every bond on the planet.

The hidden danger: interest rate risk

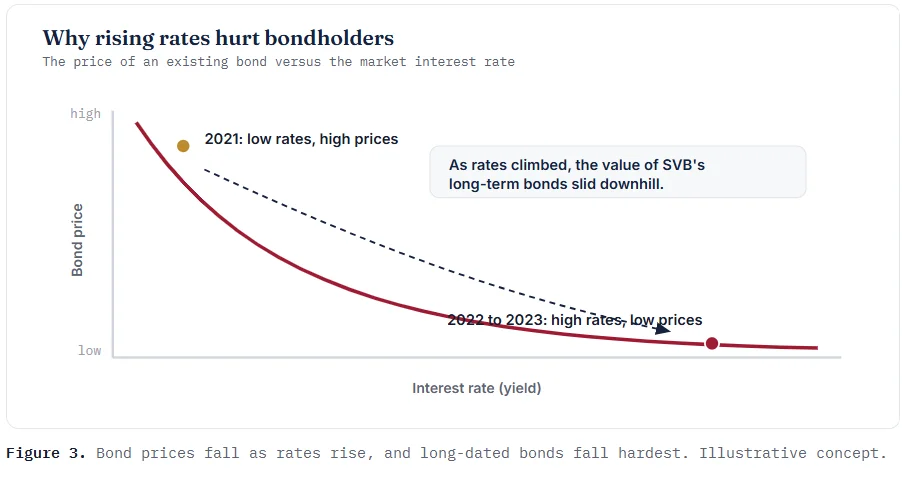

Here lies the heart of the story. Bond prices and interest rates move in opposite directions. When fresh bonds pay more, older low-rate bonds look worse. Therefore, their market price falls. This single rule explains most of what followed.

Moreover, the longer a bond’s life, the harder it drops. SVB owned bonds with very long maturities. So rising rates carved deep holes in their value. The chart below shows the relationship that trapped the bank.

A tale of two accounting buckets

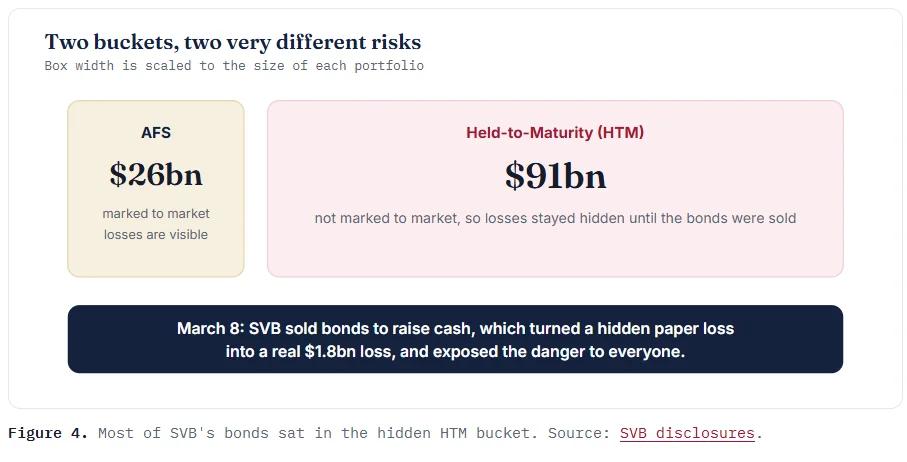

Now meet a quirk of bank accounting. Banks sort their bonds into two buckets. The first is available-for-sale, or AFS. These holdings are marked to market, so losses appear on the books quickly. The second is held-to-maturity, or HTM. These are not marked to market. Their losses stay hidden until the bonds are actually sold.

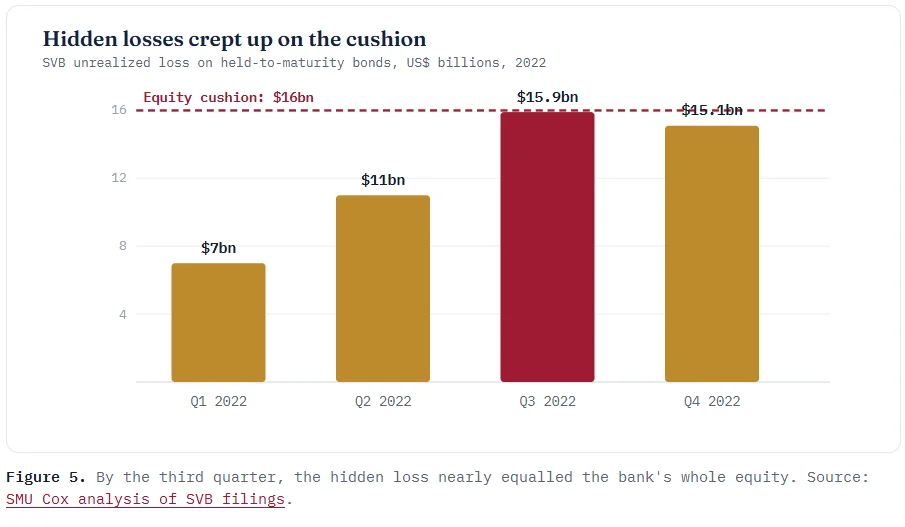

SVB kept most of its bonds in the HTM bucket. As a result, its reported figures looked calmer than reality. Yet the hidden paper losses kept growing all year. By the end of 2022, the HTM loss reached about $15 billion. Remember, the bank’s total equity was only $16 billion. In short, one forced sale could wipe out the entire cushion.

The paper losses did not appear overnight. Instead, they climbed quarter by quarter as the Fed kept hiking. The next chart tracks that slow rise toward the cliff edge.

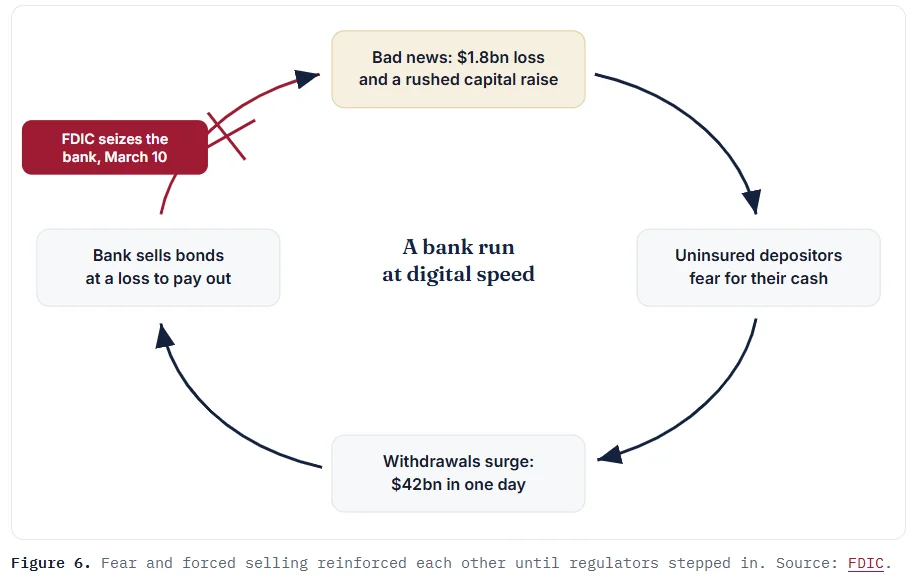

The spark and the run

On 8 March 2023, SVB lit the spark itself. It sold $21 billion of bonds at a $1.8 billion loss. At the same time, it tried to raise fresh capital. The plan was meant to strengthen the bank. Instead, it signalled distress.

Depositors reacted within hours. Remember, about 94% of SVB’s deposits sat above the $250,000 insurance limit. Uninsured money is nervous money. Venture investors urged founders to pull out fast. The warnings spread through group chats and banking apps. On 9 March, customers tried to withdraw $42 billion in a single day, nearly a quarter of all deposits.

This is a classic bank run, now supercharged by technology. Each withdrawal forced more bond sales. Each sale deepened the real losses. Each loss fed more fear. The cycle below spun faster than any rescue could move.

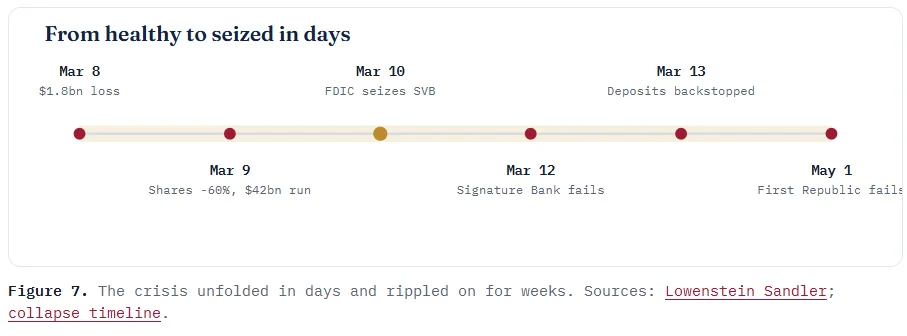

Six days in March

From the first warning, events moved at breakneck speed. On 10 March, regulators seized SVB. It became the second-largest bank failure in US history. Two days later, Signature Bank fell as well. The timeline below maps the whole collapse.

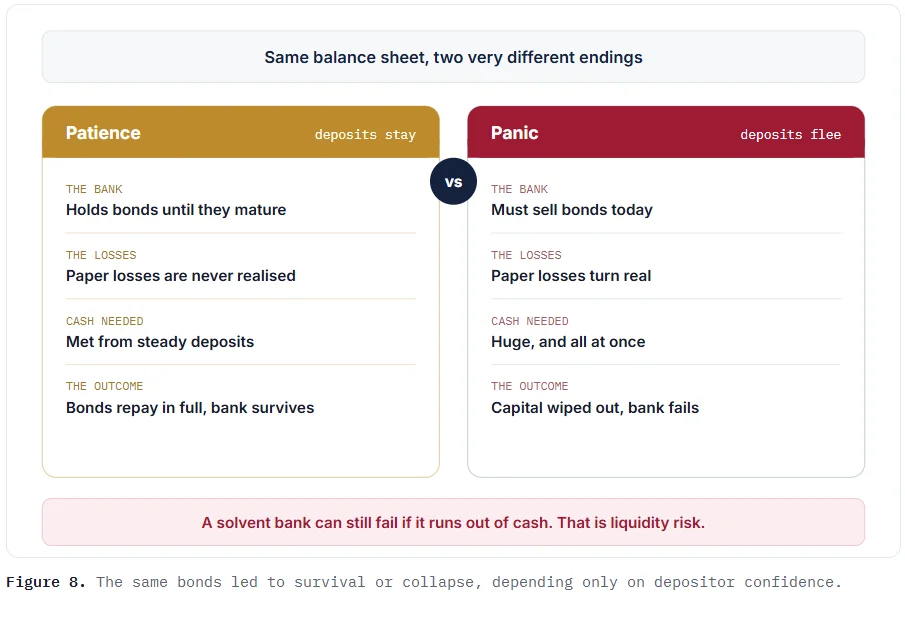

Two endings from one balance sheet

Here is the subtle part. SVB’s bonds were not worthless. Most were US government debt, almost certain to be repaid at maturity. If depositors had stayed calm, SVB could have waited. Those paper losses might never have turned real.

However, the bank could not hold on. A flood of withdrawals demanded cash immediately. So it had to sell bonds early and lock in the losses. This reveals two different risks. Solvency asks whether assets beat debts over the long run. Liquidity asks whether cash is on hand right now. Crucially, a solvent bank can still die from a liquidity squeeze.

The rescue and the ripples

Regulators feared a wider panic. So they acted hard over the weekend. The government guaranteed all SVB deposits, even the uninsured ones. The Federal Reserve also launched a new tool. Its Bank Term Funding Program lets banks borrow against bonds at full face value, not at their market-value price. That move calmed the contagion.

Even so, the shock kept spreading. First Republic Bank failed weeks later, on 1 May 2023. The Federal Reserve’s vice chair, Michael Barr, later called SVB a “textbook case of bank mismanagement”. The rescue also raised a hard question about moral hazard. If the state protects uninsured depositors, does it quietly encourage future risk-taking?

The lessons for investors and students

Several insights stand out from this episode. First, interest rate risk is real, even for “safe” government bonds. Second, accounting rules can hide danger in plain sight. Third, confidence is the true capital of any bank. Once trust evaporates, speed finishes the job.

Above all, SVB shows how tightly the system connects. A central bank fights inflation. Bond prices fall in response. A balance sheet quietly weakens. Then a rumour turns paper losses into collapse. One thread runs through the entire story: interest rates.