An analytical look at the standoff between Wall Street’s optimism and the world’s most powerful policymakers.

Table of Contents

- Table of contents will be generated automatically when the page loads.

In Summary

Markets and central banks disagree. Investors expect cuts; policymakers urge caution.

Inflation is sticky. U.S. CPI jumped to 3.3% in March 2026, well above the 2% target.

The Iran war reset the clock. Energy prices spiked, forcing central banks to pause.

The Fed, ECB, and BoE are on hold. All three signal a “meeting-by-meeting” approach.

Japan moves the other way. The Bank of Japan is debating more hikes, not cuts.

Watch for three triggers. Oil prices, services inflation, and a new Fed Chair will set the tone.

Investors keep asking the same question this year. Will central banks finally cut interest rates? Markets desperately want a “yes.” Central bankers, however, keep saying “not so fast.”

This tug-of-war defines 2026. On one side, traders are betting on cheaper money to fuel stocks, crypto, and risky bets. On the other hand, central banks are stuck watching inflation tick higher due to the war, oil shocks, and tariffs.

So who is right? And what does it mean for your portfolio?

Let’s break it down in plain English.

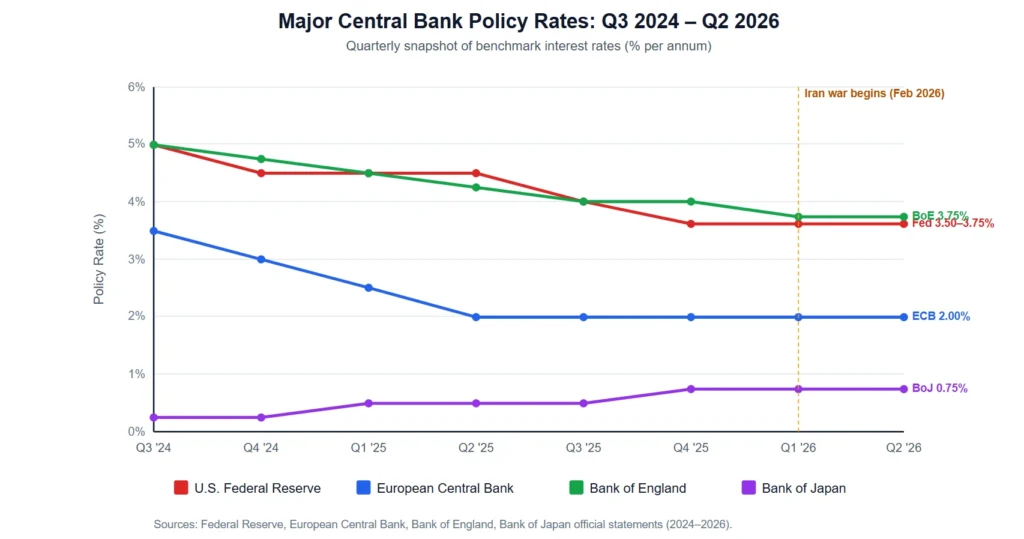

Where Global Rates Stand Today

First, the snapshot. After two years of cuts, most major central banks have paused. The U.S. Federal Reserve held its target rate at 3.50%–3.75% on March 18, 2026, and has kept it there all year. The Fed has now cut by 175 basis points since its first reduction in September 2024.

Across the Atlantic, the European Central Bank kept its deposit rate at 2.00% in March. The Bank of England held Bank Rate at 3.75% by a unanimous vote. Meanwhile, Japan is moving in the opposite direction. The Bank of Japan kept rates at 0.75%, the highest level since 1995, and is debating more hikes.

The chart below shows how these decisions have unfolded.

In short, the easing cycle has stalled. Almost everywhere, rates are on hold.

The Market’s Bet: Why Investors Smell a Cut

So why are markets still betting on cuts?

The simple answer is that investors look forward, not backwards. They watch growth slow, jobs cool, and consumers tighten their belts. That combination usually leads to lower rates.

The CME FedWatch tool currently shows a 99.5% probability of no change at the April Fed meeting. Yet beyond April, traders see a window opening. Most expect at least one Fed cut later this year, with overnight rates drifting toward the 3.00%–3.25% range once a new chair takes over.

Political pressure adds fuel. President Trump has openly demanded lower rates, and Fed Chair Jerome Powell’s term expires on May 15, 2026. His likely replacement, Kevin Warsh, is now before the Senate Banking Committee. Investors think a new chair could mean a softer touch.

Finally, growth is weakening. The IMF recently cut its UK forecasts sharply, and ECB staff expect the Eurozone’s GDP to grow by just 0.9% in 2026. Slower economies, the thinking goes, will eventually force rates down.

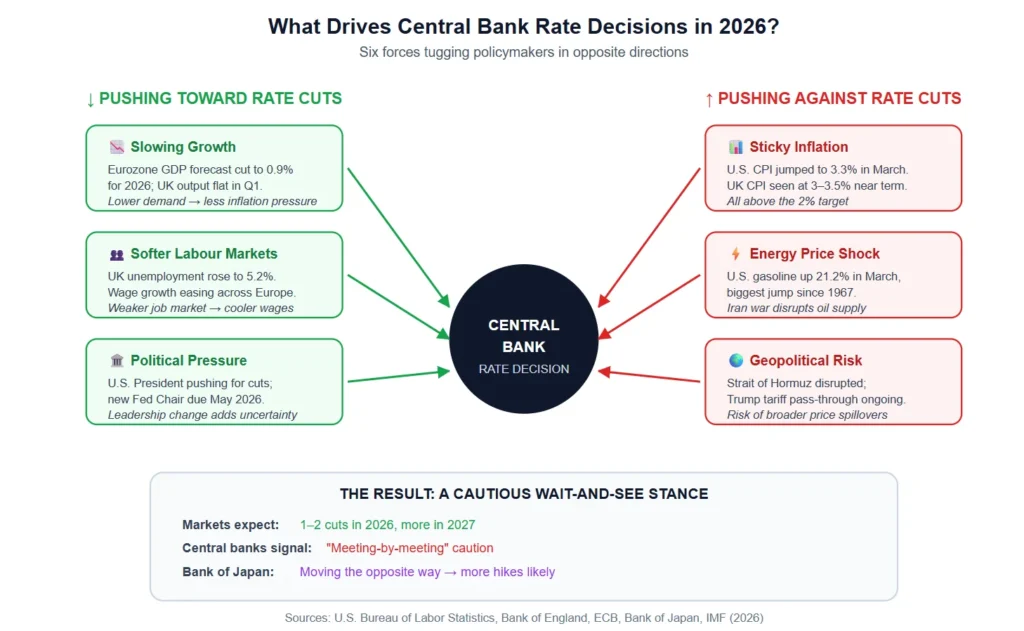

Why Central Banks Are Hitting the Brakes

Central banks see a different picture. Inflation is not dead. In fact, it is staging a comeback.

In the United States, the annual CPI jumped to 3.3% in March 2026 from 2.4% in February. That is the highest level since May 2024. The biggest culprit was gasoline, which surged 21.2% in a single month. According to the Bureau of Labour Statistics, this was the largest monthly jump in gas prices since 1967.

The picture is similar in Europe. The ECB raised its 2026 inflation forecast to 2.6%, up from 2.0% only three months earlier. The Bank of England warned that UK inflation could climb to between 3% and 3.5% over the next couple of quarters. Both targets sit well above the 2% goal.

Cutting rates into rising inflation would be a serious gamble. It risks letting prices spiral and damaging credibility. That is why policymakers keep using the same phrase: “meeting-by-meeting.” In other words, no promises.

The diagram below shows the competing forces shaping every rate decision today.

As you can see, the doves and the hawks are pulling in opposite directions. The result is paralysis.

The Geopolitical Wild Card: How War Rewrote the Script

Then came the bombshell. On February 28, 2026, conflict broke out between the United States and Iran. Almost overnight, the rate-cut narrative collapsed.

Iran disrupted shipping through the Strait of Hormuz, the waterway that handles about a fifth of the world’s oil supply. Brent crude surged past $100 per barrel. U.S. gasoline crossed $4 per gallon for the first time in three years.

The shock spread quickly. The ECB warned that the war created upside risks for inflation and downside risks for growth. Bundesbank President Joachim Nagel called the Strait of Hormuz the “heel” of the world economy (a play on Achilles’ heel). Bank of England Governor Andrew Bailey said the world was facing a very big energy shock.

Importantly, oil shocks affect rate decisions through three channels. First, they directly push up energy bills. Second, they raise input costs for businesses, which often pass them on. Third, they can de-anchor inflation expectations, meaning consumers begin to expect higher prices as normal.

A two-week ceasefire announced in mid-April brought some relief. Yet, until oil tankers flow normally again, central banks will not feel safe cutting. The risk of a second-round inflation wave is too high.

Layer this on top of Trump’s tariffs, and the Fed has every reason to wait.

What Investors Should Watch From Here

For investors, the message is clear: patience pays.

Three indicators matter most in the months ahead. First, oil prices. A reopened Strait of Hormuz could pull headline inflation back below 3% by year-end. Second, services inflation. Goldman Sachs Asset Management noted that the Fed has room to be patient as long as core inflation remains under control. Third, the new Fed Chair. A confirmed Warsh appointment could unlock the next cut cycle.

Investors should also watch Japan as the outlier. Bloomberg reported that BoJ board members are debating a larger-than-usual rate hike. A surprise from Tokyo could shake global bond markets and weaken the yen carry trade.

Finally, remember the rule of thumb. Bond markets reward those who anticipate cuts. Equity markets celebrate when the cuts actually arrive. Crypto and other risk assets often surge later, once liquidity floods in.