After four years of telling the world to never sell, Strategy’s founder has opened the door to selling Bitcoin. Here is what changed, the maths behind it, and why investors should care.

In Summary

Saylor reframed his slogan from “never sell” to “never be a net seller” of Bitcoin. He plans to buy far more than the company ever sells.

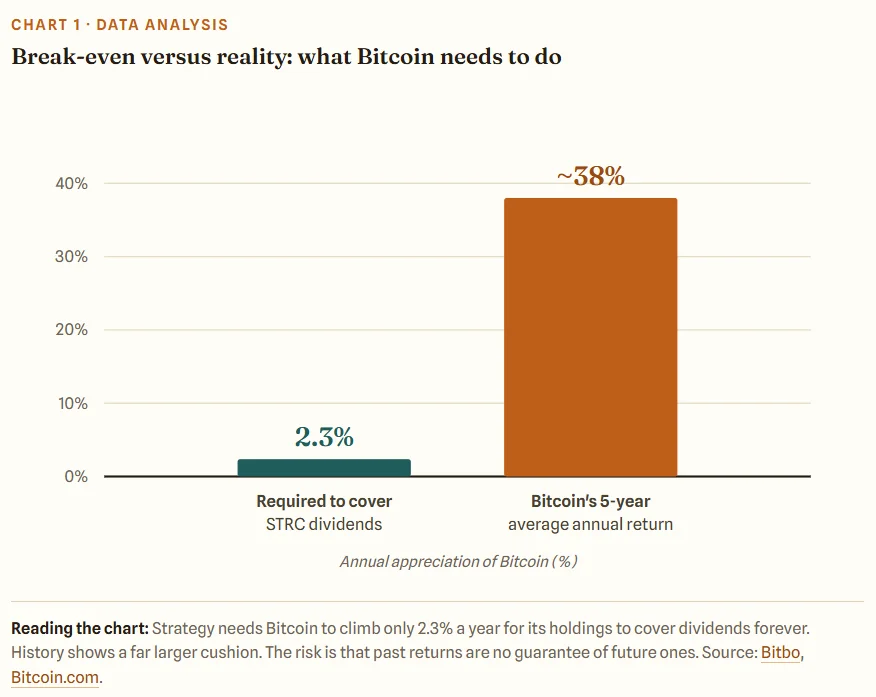

Strategy says its Bitcoin only needs to rise about 2.3% a year to cover dividend obligations forever. Bitcoin has averaged near 38% over five years.

The funding engine is STRC, a preferred stock paying an 11.5% monthly cash dividend. It has raised $8.5 billion in under a year.

Critic Peter Schiff calls STRC a “centralized Ponzi” and wants an SEC probe. Saylor counters that Strategy discloses everything in public filings.

The model depends entirely on Bitcoin continuing to appreciate. A long bear market is the central risk.

Table of Contents

- Table of contents will be generated automatically when the page loads.

For four years, Michael Saylor delivered one message with near-religious consistency: never sell your Bitcoin. In May 2026, that message shifted. Speaking with David Lin and Bonnie Chang at Consensus 2026, and on Strategy’s first-quarter earnings call, Saylor confirmed that the company is now prepared to sell Bitcoin. The reaction was instant. MSTR shares fell roughly 4% and Bitcoin slipped below $81,000. Much of the internet called it a U-turn. This analysis cuts through the noise. It explains what Saylor actually said, the maths that supports it, the sharp criticism it drew, and what the change means for everyday investors and students of markets.

From “Never Sell” to “Never Be a Net Seller”

The headline came from Strategy’s Q1 2026 earnings call. Saylor said the firm will probably sell some Bitcoin to fund a dividend “just to inoculate the market”. The word “inoculate” was chosen with care. He framed a possible sale as a signal to investors rather than a forced liquidation. CEO Phong Le added the guardrail: Strategy will sell Bitcoin only when that move is more accretive than issuing new stock.

Days later, Saylor refined his famous slogan. The precise version, he explained, is “never be a net seller of Bitcoin”. Sell one coin, he says, and the company aims to buy ten to twenty more. Strategy currently holds 818,869 BTC, acquired for roughly $61.9 billion. It also reported a $12.54 billion net loss for the quarter, driven almost entirely by a $14.46 billion unrealized markdown on those holdings. The loss was an accounting figure tied to Bitcoin’s price, not a cash shortfall.

The Math Behind the Reframe

Saylor’s defence rests on scale. Strategy carries about $1.5 billion in annual preferred-stock dividend obligations, against a Bitcoin treasury worth tens of billions. He argues the holdings only need Bitcoin to appreciate 2.3% per year to cover those dividends indefinitely, without ever touching common stock. Over the past five years, Bitcoin has returned close to 38% annually.

That gap between what is required and what history has delivered is the core of the bull case. A small, tax-efficient sale can fund a dividend while fresh capital buys far more Bitcoin than was sold. Saylor describes the trade plainly: “You would be buying 30 Bitcoin, selling one Bitcoin.” The company also holds an estimated $2.2 billion reserve fund and roughly 18 months of dividend coverage at the current run rate. There is even a tax angle. Some early Bitcoin was bought at higher prices, so selling those specific coins can trigger a tax loss while the overall stack continues to grow. The chart below shows why management frames the maths as comfortable rather than desperate. The weakness of the argument is simple: it leans on an average. A 38% return is not earned smoothly, and a multi-year slump well below 2.3% would quickly change the picture.

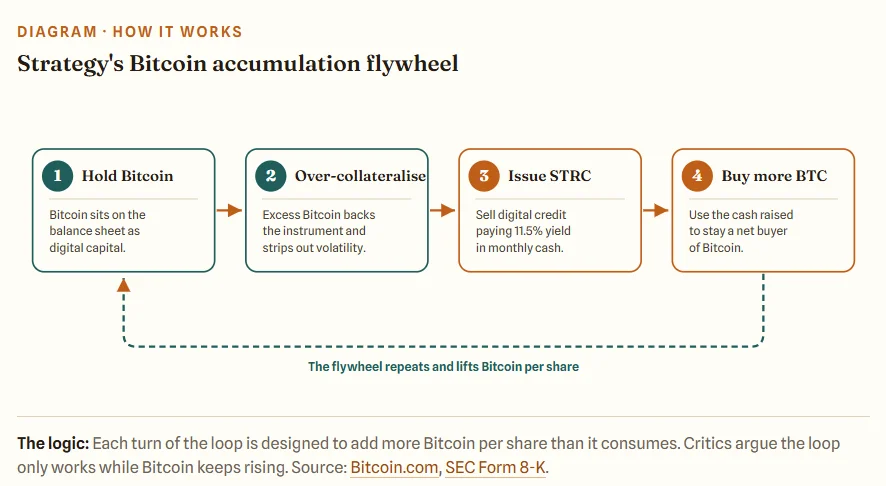

STRC and the Digital Credit Engine

To understand the strategy, you have to understand STRC. STRC, nicknamed “Stretch,” is a perpetual preferred stock. It pays an 11.5% annual dividend in monthly cash and is engineered to trade near its $100 par value. Investors buy it for predictable income. Strategy uses the cash raised to buy Bitcoin. The instrument has pulled in $8.5 billion in roughly nine months, making it the largest preferred stock by market value in the world.

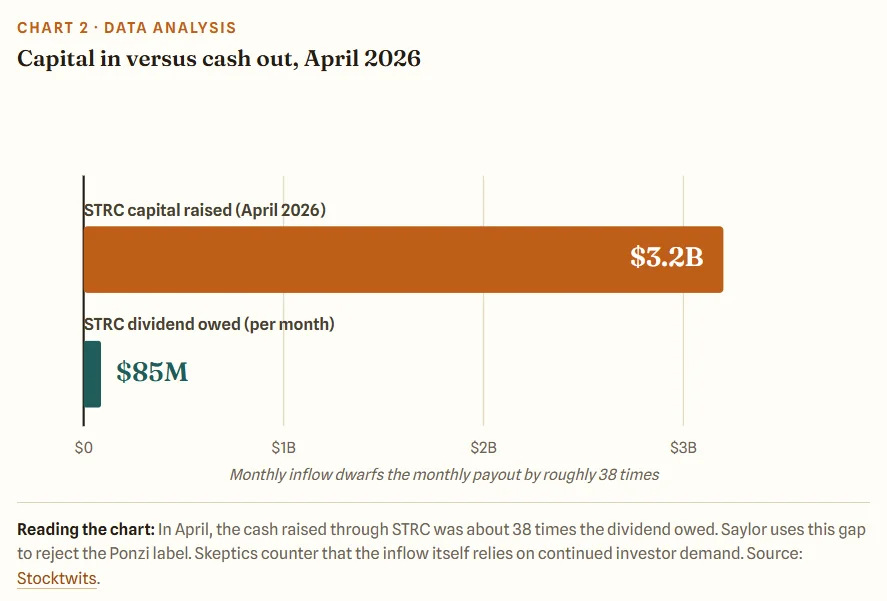

In April 2026 alone, Strategy issued about $3.2 billion of STRC against a monthly dividend bill of nearly $85 million. Saylor calls this the company’s “Bitcoin accretion engine.” His framework divides the business into three clear layers: Bitcoin as digital capital, STRC as digital credit, and MSTR shares as digital equity. The diagram below traces how cash cycles through that engine, and the chart that follows shows why the inflow dwarfs the payout.

The Ponzi Accusation

Not everyone is convinced. Veteran gold advocate Peter Schiff calls STRC “a classic centralized Ponzi” and has urged the SEC to investigate. His argument runs like this: Strategy’s software business cannot generate the $80 million to $90 million needed each month, so dividends depend on new investor money and a perpetually rising Bitcoin price.

Saylor rejects the label outright. A genuine Ponzi, he notes, has a central operator who hides the books and promises guaranteed returns. Strategy discloses its holdings, costs, and obligations in public filings that anyone can read. Schiff’s sharper warning is about the future, not the present. He predicts that in a deep downturn, Saylor would suspend the STRC dividend rather than sell Bitcoin, leaving income-focused investors exposed. The honest answer sits between the two camps. Independent analysts told Decrypt that disciplined treasury management could actually strengthen confidence in Bitcoin treasury companies. Others warn that the structure is genuinely fragile if Bitcoin trades flat or falls for an extended period. The label matters less than the mechanics, and the mechanics still depend on a rising asset.

What Actually Moves Bitcoin

Saylor insists his own buying barely moves the market. Bitcoin, he claims, can absorb $100 million to $200 million per hour without a meaningful price shift. The real drivers, he argues, lie elsewhere: global liquidity, central bank policy, exchange-traded fund flows, and broad investor adoption.

A tight Federal Reserve and geopolitical tension have pressured prices since the October 2025 crypto crash. This macro backdrop matters directly for Strategy. When Bitcoin and MSTR fall together, raising money through new shares becomes more dilutive. That is precisely when selling a slice of Bitcoin becomes the cheaper funding option. Viewed this way, the “prepared to sell” stance is a financial tool that responds to market conditions, not a loss of conviction.

Digital Capital, Digital Credit, and AI

Saylor’s wider thesis reaches well beyond a single company. He sees Bitcoin as the collateral base for an entirely new credit system. The global private credit market exceeds $3.5 trillion, yet remains opaque and illiquid. Digital credit, he argues, is transparent, liquid, and free of heavy fees. Capturing even 10% of that market would unlock around $350 billion.

He ties this vision to artificial intelligence and an economy that increasingly runs on programmable, on-demand capital. Strategy’s stated goal is concrete: double its Bitcoin per share within seven years. Saylor now calls Bitcoin per share the firm’s true performance metric, describing it as “EPS on the Bitcoin Standard.”

What Investors Should Weigh

The reframe is clever, but it is not free of risk. The entire model assumes that Bitcoin continues to compound well above 2.3% per year. A long, grinding bear market would test that assumption hard. MSTR trades as a high-beta Bitcoin proxy, so every price swing is amplified by leverage.

Sentiment reflects the uncertainty. The prediction market Polymarket now gives roughly an 82% chancethat Strategy sells Bitcoin at some point in 2026. The slogan has quietly moved from “never sell” to “never be a net seller,” and that shift is meaningful. For investors and students alike, the takeaway is steady rather than dramatic. Read the filings, follow the maths, and judge the engine on its mechanics, not its marketing. Strategy has turned Bitcoin into a financial platform. Whether that platform proves durable depends, as it always has, on the price of one famously volatile asset.

Glossary: Key Terms Explained

| Strategy (MSTR) | The company, formerly named MicroStrategy. It is the world’s largest publicly traded corporate holder of Bitcoin and also sells analytics software. |

| STRC (“Stretch”) | A perpetual preferred stock issued by Strategy. It pays an 11.5% annual dividend in monthly cash and is designed to trade near its $100 par value. |

| Preferred stock | A type of share that ranks above common stock for dividends and pays a fixed yield, behaving more like a bond than ordinary equity. |

| Dividend | An entity that sells more of an asset than it buys over a period. Saylor pledges that Strategy will never be a net seller of Bitcoin. |

| Net seller | A transaction that increases value for existing shareholders, in this case, measured as more Bitcoin per share. |

| Accretive | Backing a financial instrument with more asset value than it owes creates a safety buffer against price falls. |

| Bitcoin per share (BPS) | The amount of Bitcoin backing each MSTR share. Strategy treats it as its main performance metric. |

| Over-collateralisation | A fraud that pays earlier investors with money from new ones, with no real underlying returns. Saylor argues that strategy does not fit this definition because it discloses its finances publicly. |

| Unrealized loss | A paper loss from an asset falling in value while it is still held. It becomes a real loss only if the asset is sold. |

| High-beta proxy | An asset whose price moves more sharply than the thing it tracks. MSTR often swings harder than Bitcoin itself. |

| Ponzi scheme | A fraud that pays earlier investors with money from new ones, with no real underlying returns. Saylor argues Strategy does not fit this definition because it discloses its finances publicly. |

| Convertible notes | A regular cash payment that a company makes to certain shareholders. STRC holders receive theirs monthly. |