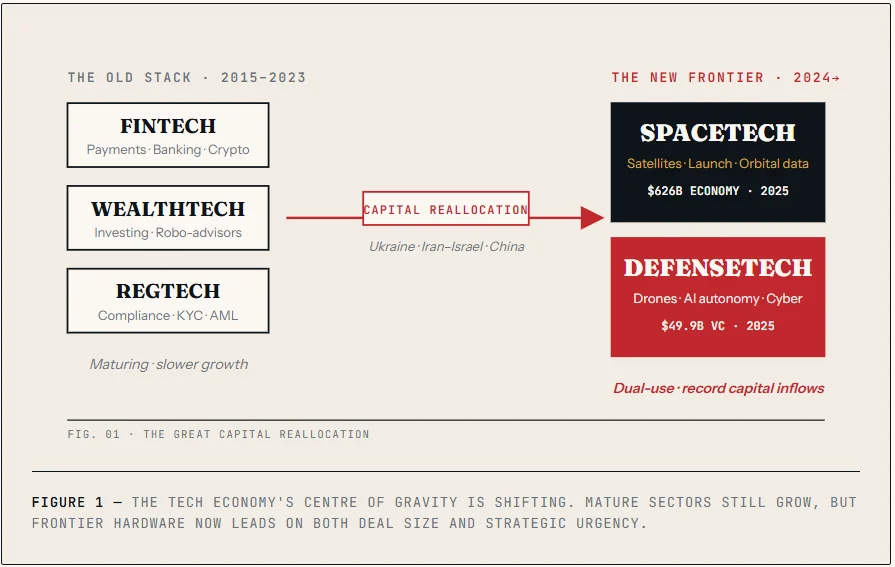

For a decade, venture money chased fintech, wealthtech, and regtech. In 2025, capital found a new frontier, and a $2.72 trillion geopolitical tailwind came with it.

In Summary

The capital map has moved. Defensetech VC hit $49.9 billion in 2025; spacetech private investment jumped 48% to $12.4 billion.

Geopolitics is the engine. Ukraine, the Iran–Israel war, and NATO’s new 5% GDP spending target are pulling capital toward hardware.

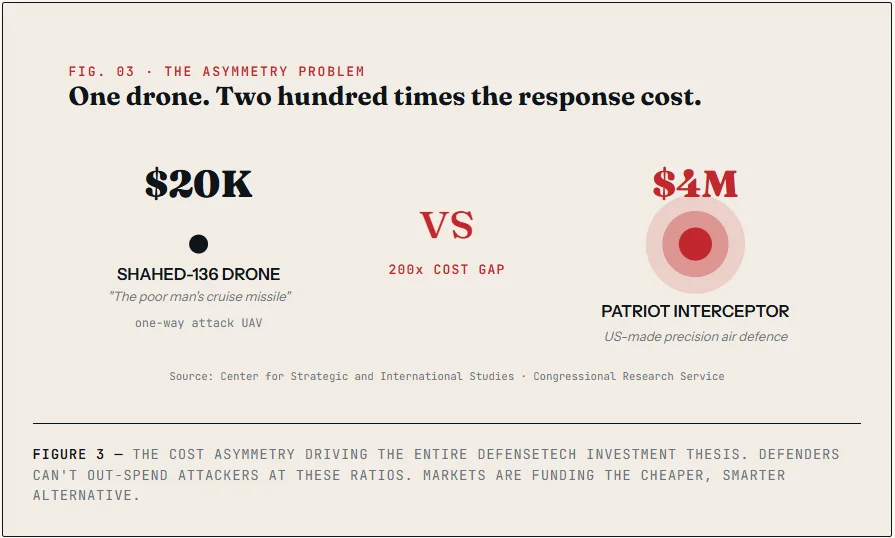

Cost asymmetry changed warfare. $20,000 drones forcing $4 million responses exposed the urgent need for cheaper, smarter defence.

Fintech is not dying; it is maturing. Global fintech reached $116 billion in 2025, but growth has cooled relative to frontier sectors.

Dual-use is the edge. Startups serving both civilian and defence markets are attracting the largest rounds.

Execution will beat invention. 2026 winners will be firms that scale manufacturing, not just prototype.

Table of Contents

- Table of contents will be generated automatically when the page loads.

In March 2026, a Shahed drone that cost roughly $20,000 cruised into Gulf airspace. To shoot it down, a United States Patriot battery fired an interceptor worth about $4 million. One cheap weapon forced a response two hundred times its value.

That single math problem captures a shift quietly reshaping global tech investing. For a decade, venture money chased fintech, wealthtech, and regtech, software that moves money, manages money, or keeps money legal. In 2025, capital moved. It started flowing hard into spacetech and defensetech, sectors that used to sit at the edges of the startup map.

This is not a fringe story anymore. It is a structural reset of where the world’s smartest capital believes growth will live over the next decade. Here is what is changing, why it matters, and how to read it.

What these words actually mean

Spacetech covers anything built to work beyond Earth’s atmosphere. Think satellites, launch vehicles, space-based internet, and Earth-observation platforms. Defensetech builds dual-use systems for national security drones, autonomous vehicles, cyber tools, AI targeting, and counter-drone shields.

Both overlap. A low-orbit satellite constellation can sell broadband to farms and surveillance to generals. A drone factory can serve agriculture and artillery. This “dual-use” quality is exactly why investors like them.

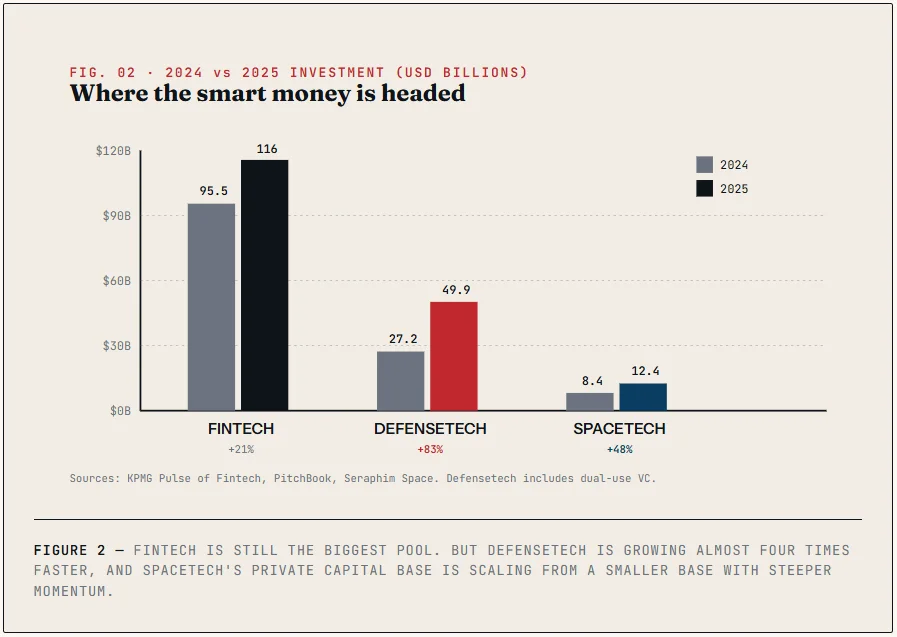

Compare them with their older cousins. Fintech digitises banking. Wealthtech builds investing tools. Regtech automates compliance. These sectors are maturing, but growth has cooled. Global fintech investment reached $116 billion in 2025, a modest rebound from a seven-year low. Wealthtech funding fell to a three-year low of $1.4 billion.

Meanwhile, capital in frontier tech is moving in the opposite direction, upward and fast.

The numbers are no longer subtle

Defensetech had its biggest year ever. PitchBook recorded venture investment of $49.9 billion across 966 deals in 2025. Anduril Industries, the autonomous-systems firm, closed a $2.5 billion Series G at a $30.5 billion valuation. Around one in every twelve venture dollars now flows into defence-linked startups.

Spacetech is compounding too. Global private space investment jumped 48% to $12.4 billion in 2025, per Seraphim Space. The broader space economy reached $626 billion in 2025 and is on course for over $1 trillion by 2034.

State money is pushing the wave even harder. Global military spending hit $2.72 trillion in 2024, the steepest rise since the Cold War. NATO members agreed at the 2025 Hague Summit to lift spending to 5% of GDP by 2035, more than double the old target.

“Ukraine demonstrated drone and autonomous system effectiveness in real combat, fundamentally shifting how VCs view defense investments.”

— JASON SALTZMAN, CB INSIGHTS

Why now? The geopolitical trigger

Three shocks pulled capital out of consumer apps and into hardware.

Ukraine proved the model. Russia’s invasion forced a rapid battlefield test of cheap drones, AI targeting, and software-defined warfare. Investors watched startups outperform legacy contractors in real combat.

The Middle East multiplied the point. Iran’s Twelve-Day War with Israel in June 2025 and the broader 2026 Iran War revealed a brutal cost asymmetry. Iran launched thousands of Shahed drones at $20,000 to $50,000 each. Defenders shot them down with Patriot missiles costing $4 million per interceptor and Iron Dome rounds at roughly $50,000. Even Israel’s layered shield struggled with the math.

China accelerated the rest. Export controls on rare earths and strategic minerals forced Western governments to rebuild industrial capacity at home. Beijing controls about 70% of global rare-earth production and 90% of processing, according to Bessemer Venture Partners. When hardware is strategic, capital follows.

Who is actually winning?

The names to know sit at the intersection of software and steel.

In defence tech, Anduril leads with autonomous platforms and the Pentagon’s $22 billion IVAS contract. Helsing in Europe, Shield AI, Saronic (autonomous ships), and Epirus (counter-drone microwaves) are attracting billions. Israeli defence tech had a breakout year in 2025, with eight companies raising over $360 million.

In spacetech, SpaceX still dominates launch economics. Rocket Lab, Firefly Aerospace, and Voyager went public in 2025 to strong demand. Satellite firms like ICEYE (radar imagery) and Loft Orbital (satellite-as-a-service) are scaling fast.

Capital allocators have shifted, too. Andreessen Horowitz’s American Dynamism fund, Founders Fund, 8VC, and NATO’s €1 billion Innovation Fund now treat this space as a core allocation rather than a side bet.

What it means for you

For investors: The risk profile differs from that of fintech. Defence contracts are long, procurement cycles are slow, and regulatory exposure is real. Execution, not invention, will decide 2026 winners. Look for companies converting funding into real manufacturing throughput.

For students and builders: The skill stack has shifted. AI, robotics, computer vision, satellite engineering, and supply-chain hardware are now in demand alongside software. Dual-use startups hire from both commercial and defence backgrounds.

For general readers: This shift touches consumer life, too. Starlink-style internet reshapes rural connectivity. Earth observation powers climate tracking and insurance. AI-driven logistics spills from defence into shipping.

The same pattern that turned fintech into a multi-hundred-billion-dollar industry is now starting in spacetech and defensetech, at an earlier stage, higher risk, and potentially much bigger.