Airlines lock in fuel prices. Farmers lock in crop prices. Banks lock in exchange rates. This article explains how futures and forward contracts make that possible, and what margin calls, contango, and daily settlement really mean in practice.

In Summary

First and foremost, a futures contract is a standardised, exchange-traded agreement to buy or sell an asset at a set price on a specific future date. Both parties are legally obligated to fulfil it.

Moreover, a forward contract serves the same purpose but is privately negotiated OTC. As a result, it is more flexible but carries higher counterparty risk.

Notably, margin is not a down payment. Instead, it is a performance bond. Daily mark-to-market settlement means gains and losses are settled every business day.

Additionally, a margin call is issued when an account falls below the maintenance margin level. The trader must deposit additional funds immediately or face forced closure of the position.

By contrast to spot markets, futures prices reflect the expected future value of an asset. Contango means futures prices are above spot; backwardation means they are below.

Furthermore, the April 2020 oil price event showed that WTI crude fell to -$37.63 per barrel when storage ran out. Physical delivery obligations drove this extreme outcome.

For instance, airlines, miners, farmers, and multinationals all use futures and forwards every day to eliminate price uncertainty from their business operations.

Finally, both hedgers and speculators are essential. Hedgers reduce real-world risk. Speculators provide the liquidity that makes the market function efficiently for everyone.

Table of Contents

- Table of contents will be generated automatically when the page loads.

The Airline CFO’s Problem

It is early 2023. Sarah Chen is the chief financial officer of a major airline. Jet fuel, in fact, accounts for nearly 30% of her company’s total operating costs. However, oil prices are volatile and unpredictable. A sudden spike could wipe out the airline’s annual profit in a matter of weeks. Meanwhile, shareholders demand certainty in every quarterly forecast.

Consequently, Sarah’s treasury team turns to futures contracts. By locking in fuel prices three months ahead, the airline eliminates that uncertainty. In other words, the airline trades the chance of lower costs for the guarantee of known costs. This is precisely what futures and forwards were designed to do. Together, they are among the most widely used financial instruments in the world.

According to the CME Group, futures markets enable businesses across every industry to manage risk, discover prices, and plan with confidence. Indeed, without these instruments, global commerce would be far more uncertain and expensive to manage.

What Exactly Is a Futures Contract?

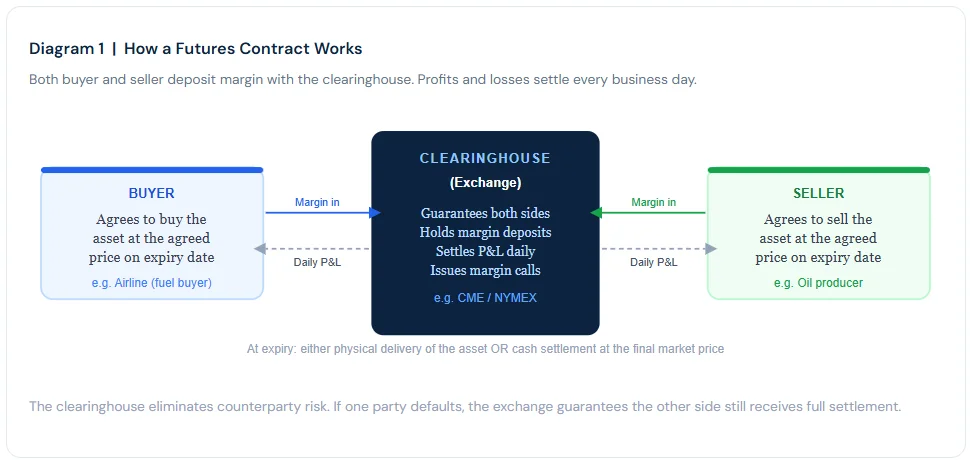

A futures contract is a standardised agreement to buy or sell a specific asset at a specific price on a specific future date. Both parties are specifically legally obligated to fulfil the contract upon expiry. Furthermore, all futures contracts trade on a regulated exchange, such as the Chicago Mercantile Exchange (CME) or the New York Mercantile Exchange (NYMEX).

Three features, moreover, make futures distinct from most other financial instruments. First, standardisation means every contract has fixed specifications, including the quantity of the underlying asset, the delivery location, and the settlement date. Second, exchange trading ensures full price transparency and regulatory oversight. Third, daily mark-to-market settlement means profits and losses are calculated and collected every single business day, not just at expiry.

This daily settlement mechanism, in fact, is what prevents losses from accumulating silently until they become catastrophic. Instead, the clearinghouse collects losses each day and credits gains. Consequently, risks are managed in real time rather than deferred to the contract’s end date.

Contract Specifications: A Practical Example

Every futures contract has a defined specification sheet. For example, one WTI crude oil futures contract on NYMEX represents exactly 1,000 barrels of West Texas Intermediate crude. Similarly, one COMEX gold futures contract represents 100 troy ounces of gold. Standardisation, therefore, allows traders worldwide to buy and sell the same instrument with complete clarity about what they are trading.

What Is a Forward Contract?

A forward contract serves the same fundamental purpose as a futures contract. However, it is privately negotiated between two parties rather than traded on an exchange. As a result, the terms are fully customisable. An importer expecting a large payment in Japanese yen, for instance, might agree with a bank to sell those yen at a fixed rate in 90 days. The exact amount, the settlement date, and all other terms can be tailored to specific needs.

Nevertheless, this flexibility carries an important trade-off. Forwards involve counterparty risk, since there is no clearinghouse to guarantee performance. Additionally, exiting a forward contract early is far more complex than closing a futures position. Most commonly, corporates use forwards through their relationship banks for currency, interest rate, and commodity hedging purposes.

According to the BIS Triennial Central Bank Survey 2022, the global OTC foreign exchange forward market sees daily turnover of approximately $1.1 trillion. Indeed, this scale underscores just how essential forward contracts are to international trade and finance.

How Margin Works: The Performance Bond

Margin is one of the most misunderstood concepts in futures trading. Many new investors assume it works like a mortgage down payment. Instead, margin is best understood as a performance bond. It ensures both parties will honour their contract obligations regardless of price movements.

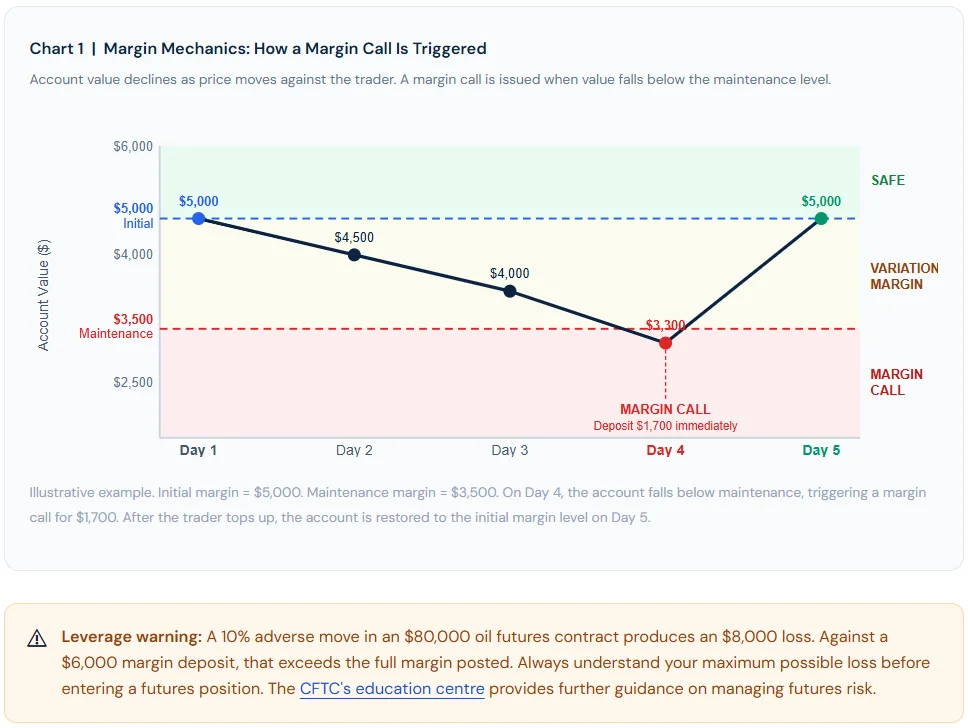

When a trader opens a futures position, the exchange requires an initial margin deposit. This is typically a small percentage of the contract’s total notional value. For example, one WTI crude oil futures contract at $80 per barrel has a notional value of $80,000 (1,000 barrels x $80). However, the initial margin requirement is approximately $5,000 to $7,000, depending on current volatility.

The Margin Call

Every day, the exchange recalculates the account’s value based on the latest market price. This process is called mark-to-market settlement. If the price moves against the trader, the account value falls. Moreover, if it falls below the maintenance margin level (typically set at around 70-80% of the initial margin), the exchange issues a margin call. The trader must then deposit additional funds immediately. Furthermore, failure to meet a margin call results in the exchange forcibly closing the position at the prevailing market price.

Consequently, margin amplifies both gains and losses. A 10% adverse move in oil prices on a $80,000 contract produces an $8,000 loss. Against a $6,000 margin deposit, that represents a loss exceeding the entire margin posted. As a result, futures traders must monitor their positions closely every single trading day.

Contango and Backwardation

These two terms describe the shape of the futures price curve. Understanding them, moreover, is essential for any investor using futures markets for hedging or investment purposes.

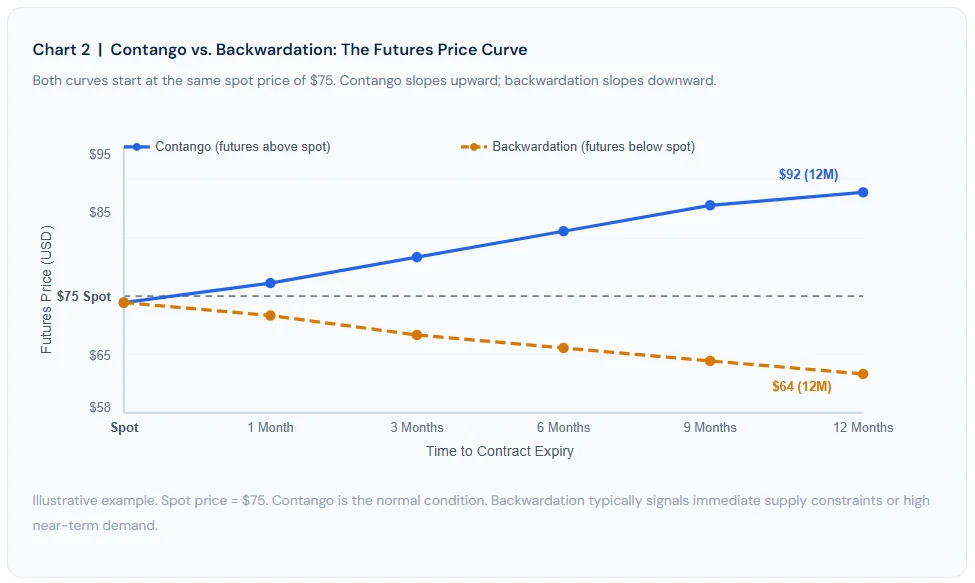

Contango: Normal Market Conditions

Contango occurs when futures prices are higher than the current spot price. This is, in fact, the most common condition for commodity markets. Storage costs, insurance, and financing expenses explain the premium. For example, if oil is trading at $75 today, a futures contract for delivery in 12 months might be priced at $82. Consequently, the futures curve slopes upward over time. Gold and oil futures, notably, typically trade in contango during normal market conditions.

Backwardation: When Supply Is Tight

By contrast, backwardation occurs when futures prices are lower than the current spot price. This happens when the immediate supply is severely constrained or the demand is urgent. Oil futures entered backwardation during periods of Middle East supply disruptions, for instance. Similarly, agricultural futures can enter backwardation during drought seasons when current supplies are scarce. Furthermore, backwardation can signal that the market expects future supply conditions to ease.

Real-World Use Cases

Futures and forwards are used across virtually every major asset class and industry. Below are the most significant examples of how these instruments work in the real world.

The April 2020 Moment: When Oil Went Negative

The most dramatic illustration of futures mechanics in modern history occurred in April 2020. The COVID-19 pandemic crushed global oil demand almost overnight. Storage facilities, moreover, were rapidly filling to capacity. Consequently, traders holding long positions in WTI crude oil futures faced an extraordinary problem.

On 20 April 2020, WTI crude oil futures for May delivery fell to -$37.63 per barrel. In other words, sellers were actually paying buyers to take delivery of the oil. This negative price was not merely symbolic. Instead, it revealed a fundamental truth about the physical delivery of futures contracts.

Traders holding futures contracts at expiry must either deliver the commodity or accept physical delivery. Without available storage, those holding long positions had no choice but to sell at any price available. As a result, oil prices fell below zero for the first time in recorded history. Indeed, this event remains the starkest example of how futures mechanics can produce extreme and unexpected outcomes.

“The oil market is telling us something stark: we have too much oil and nowhere to put it.”

-Market commentary, April 2020, widely reported across Reuters, Bloomberg, and the Financial Times

Hedgers vs. Speculators: Two Vital Groups

Two distinct groups participate in futures markets. Each, furthermore, plays a vital and complementary role in making the entire system work efficiently.

Specifically, hedgers use futures to reduce an existing risk. They have a genuine, real-world financial exposure, such as an airline needing jet fuel, a farmer growing wheat, or an exporter expecting payment in a foreign currency. Futures allow them to lock in prices and eliminate that uncertainty. However, in doing so, they give up the potential benefit of a favourable price move.

Speculators, by contrast, take on that very risk in exchange for potential profit. They have no underlying exposure to the commodity or asset at all. Instead, they simply take a position on whether prices will rise or fall. Without speculators, futures markets would lack the depth and liquidity that hedgers require. Furthermore, their participation ensures that hedgers can always find a willing counterparty when they need to enter or exit a position.

Up Next: Options Explained: The Right, But Not the Obligation