Swaps are the largest segment of the global derivatives market, yet most investors have never heard of them. This article explains interest rate swaps, currency swaps, and the credit default swaps that triggered the worst financial crisis in a generation.

In Summary

First and foremost, a swap is an agreement between two parties to exchange a series of cash flows over time. Unlike futures, swaps are privately negotiated and traded OTC rather than on regulated exchanges.

Moreover, interest rate swaps are the most common type, allowing one party to exchange fixed interest payments for floating ones. As a result, companies can match their preferred rate structure regardless of how they originally borrowed.

Notably, in an interest rate swap, only the net difference in interest payments changes hands. The notional principal itself is never actually exchanged between the parties.

By contrast, currency swaps DO exchange principal amounts. This makes them the right tool for companies that need to raise capital in one currency while operating in another.

Additionally, credit default swaps function like insurance on a bond or loan. The protection buyer pays premiums. The protection seller pays out only if a credit event, such as default, occurs.

In particular, CDS played a central role in the 2008 financial crisis. AIG sold over $440 billion of CDS protection without adequate reserves, requiring a $182 billion government bailout when housing defaults surged.

Furthermore, the Dodd-Frank Act 2010 in the US and EMIR in Europe responded by requiring most standardised swaps to be centrally cleared and reported to trade repositories for regulatory oversight.

Finally, swaps serve legitimate purposes for banks, corporations, pension funds, and governments. The instruments themselves are not inherently dangerous. The 2008 crisis demonstrated that the danger lies in opacity, excessive leverage, and inadequate collateral practices.

The Corporate Treasurer’s Problem

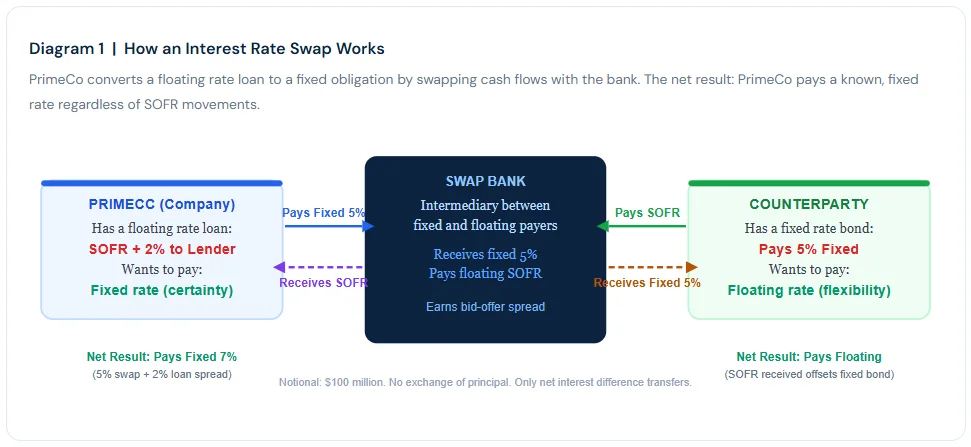

PrimeCo, a UK manufacturing company, has just secured a $100 million loan to expand its factory. The loan carries a floating interest rate set at SOFR plus 2%, which resets every 3 months. However, PrimeCo’s CFO is deeply concerned. If SOFR rises sharply over the next five years, the company’s interest costs could become unmanageable. Furthermore, the board has demanded predictable, fixed costs for financial planning and investor presentations.

Consequently, the CFO calls the company’s bank. The solution is straightforward: an interest rate swap. PrimeCo agrees to pay the bank a fixed 5% rate on a notional amount of $100 million. In return, the bank pays PrimeCo the floating SOFR rate each quarter. As a result, PrimeCo’s net interest cost becomes effectively fixed, regardless of how much rates move. The floating-rate loan is converted into a fixed-rate obligation without altering the underlying loan agreement.

This is the essence of a swap. Indeed, according to ISDA’s 2024 Annual Review, interest rate swaps remain the largest category of derivatives activity globally, underscoring how universal this problem is for businesses of all sizes.

What Exactly Is a Swap?

A swap is a private agreement between two parties to exchange a series of cash flows over a specified period. Specifically, each party pays the other according to a pre-agreed formula. In other words, rather than transferring ownership of any asset, the two sides simply exchange financial obligations. Furthermore, the principal amount, called the notional, is generally not exchanged between parties. It is used only to calculate the size of the cash flow payments.

Swaps fall into three main categories. First, interest rate swaps exchange fixed interest payments for floating ones. Second, currency swaps exchange cash flows denominated in different currencies. Third, credit default swaps transfer the credit risk of a bond or loan from one party to another. Each type, moreover, serves a distinct purpose and attracts different users across the financial system.

Interest Rate Swaps: Converting Fixed to Floating

An interest rate swap (IRS) is the most common type of swap worldwide. In a standard IRS, one party agrees to pay a fixed interest rate while the other pays a floating rate, such as the Secured Overnight Financing Rate (SOFR). Both payments are calculated on the same notional principal. However, only the net difference between the two payments actually changes hands at each settlement date.

Why Companies Use Interest Rate Swaps

Companies use IRS for two broad reasons. First, they may prefer one rate structure but can only access the other in the market. Specifically, a highly-rated company might borrow at a very competitive fixed rate but prefer floating payments to match its floating-rate revenues. Second, they may simply need to change their interest rate exposure after market conditions change. Furthermore, banks and pension funds use the IRS to manage the interest-rate sensitivity of their entire balance sheets, often running swap books worth hundreds of billions of dollars.

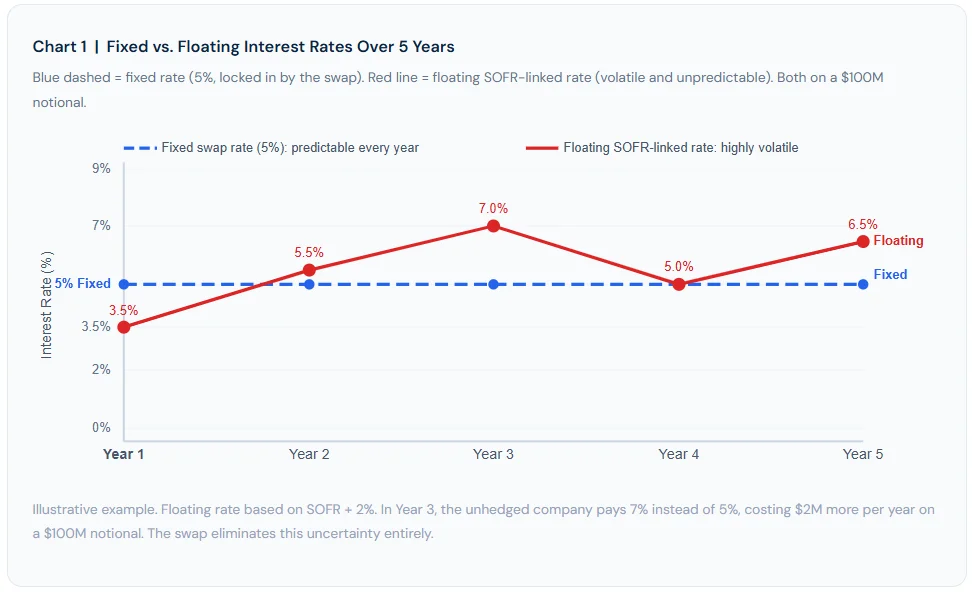

The chart below shows why rate certainty matters so much. Floating rates can be highly volatile over a five-year period. As a result, a company without an IRS faces genuine budget uncertainty every single quarter.

Currency Swaps: Bridging Borders

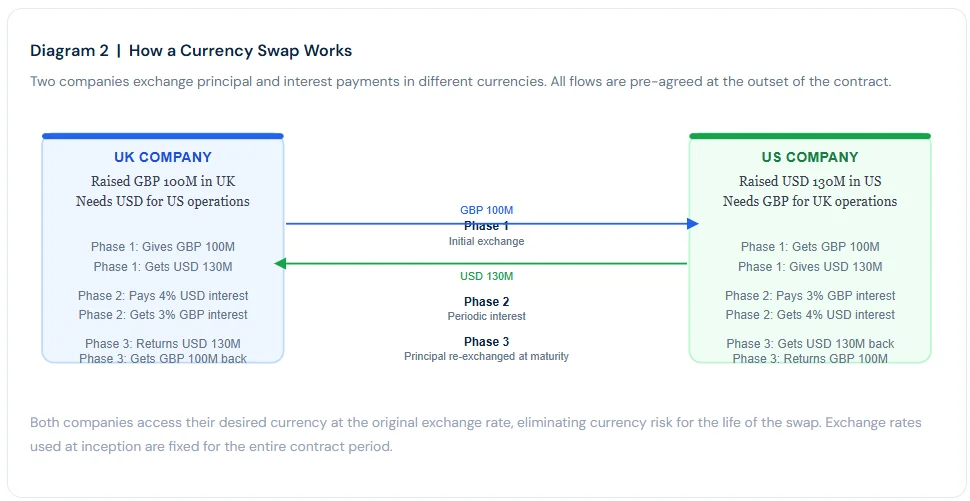

A currency swap involves the exchange of both principal and interest payments in two different currencies. By contrast with interest rate swaps, the principal amount IS exchanged at the start and reversed at maturity. This structure makes currency swaps ideal for companies raising capital in one country while operating in another.

The world’s first major currency swap occurred in 1981. IBM had issued bonds in Swiss francs and Deutsche marks. Meanwhile, the World Bank needed those currencies but had issued only dollar-denominated bonds. Consequently, they agreed to swap their respective cash flow obligations. IBM paid dollars to the World Bank; the World Bank paid Swiss francs and Deutsche marks to IBM. Both parties achieved their funding needs without re-entering bond markets. Furthermore, this landmark transaction established the template for the modern currency swap market.

Today, multinational corporations, central banks, and governments all use currency swaps. A Japanese exporter earning US dollars, for instance, might swap those dollars for yen to fund its domestic operations, locking in the exchange rate for the entire swap period. Additionally, central banks use currency swap lines with foreign counterparts to provide emergency liquidity in foreign currencies during financial stress.

Credit Default Swaps: Insurance on Debt

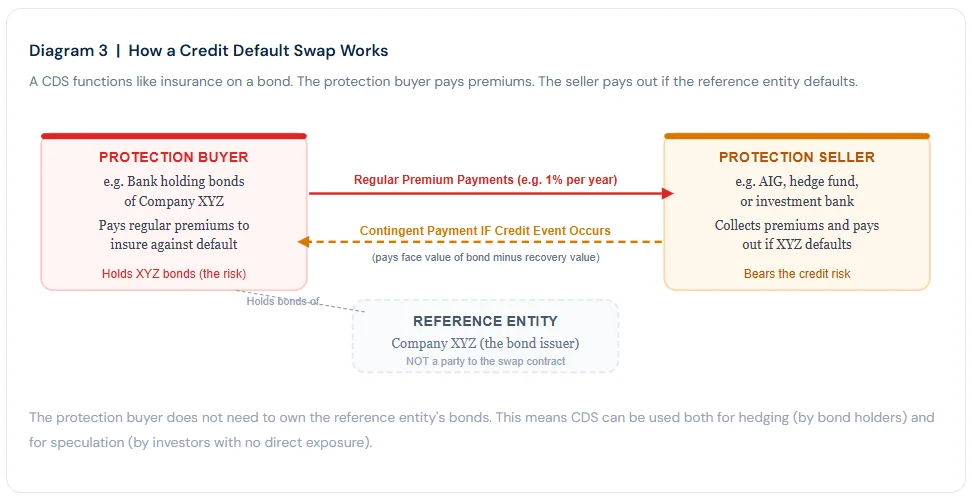

A credit default swap (CDS) is the most controversial member of the swap family. In essence, it functions like an insurance policy on a bond or loan. Specifically, the protection buyer pays regular premiums to the protection seller. In return, the seller agrees to compensate the buyer if a defined “credit event” occurs, such as a default, bankruptcy, or debt restructuring of a third-party entity called the reference entity.

However, unlike conventional insurance, the protection buyer does not need to own the underlying bond. As a result, investors can use CDS to bet on the creditworthiness of a company, government, or asset-backed security without holding any actual debt. Furthermore, this feature means that the total CDS exposure for a given reference entity can vastly exceed the actual debt outstanding, since many different parties can take positions on the same reference entity.

CDS and the 2008 Financial Crisis

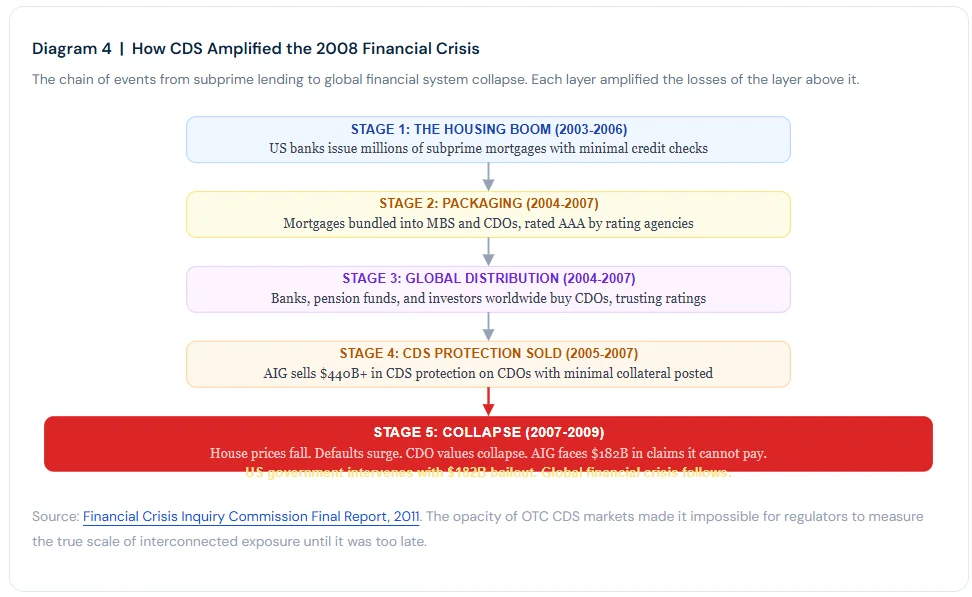

The 2008 global financial crisis is impossible to understand without understanding credit default swaps. Specifically, the interconnected web of CDS contracts transformed a US housing market downturn into a global systemic catastrophe. As the Financial Crisis Inquiry Commission concluded in its 2011 report, CDS played a central role in amplifying the crisis beyond what housing losses alone could have caused.

The Chain of Events

In the years before 2008, US banks packaged millions of subprime mortgages into securities called collateralised debt obligations (CDOs). Moreover, rating agencies assigned high credit ratings to many of these products. Consequently, banks and investors around the world eagerly bought them, believing the risk was low. Additionally, they purchased CDS protection from sellers, primarily AIG, to further reduce their apparent risk.

AIG, in particular, sold hundreds of billions of dollars worth of CDS protection on mortgage-backed securities. Furthermore, AIG posted almost no collateral against these obligations, since its own AAA credit rating made collateral unnecessary under the contracts of the time. As a result, AIG was effectively acting as an insurer that had collected vast premiums without holding any reserves.

When US house prices began falling in 2007 and accelerated in 2008, mortgage defaults surged. Subsequently, CDO values collapsed. Consequently, CDS protection buyers simultaneously began making claims on AIG. Nevertheless, AIG had nowhere near enough capital to pay. By September 2008, AIG faced imminent bankruptcy. The US Federal Reserve and Treasury intervened with an emergency bailout totalling $182 billion, concluding that AIG’s failure would trigger cascading defaults across the global financial system.

“AIG operated like no insurance company in the world. It wrote hundreds of billions in insurance on assets it barely understood, with almost no capital to back its commitments.”

-Financial Crisis Inquiry Commission, Final Report, 2011

Regulation After 2008: Bringing Swaps Into the Light

The 2008 crisis exposed a critical flaw in OTC derivatives markets: opacity. Regulators had no visibility into the total size or interconnectedness of the global CDS market. As a result, governments moved quickly to impose new rules on the swaps industry.

Dodd-Frank Act 2010 (United States)

The Dodd-Frank Wall Street Reform and Consumer Protection Act, signed in 2010, fundamentally changed how swaps are traded and regulated. Specifically, it required most standardised OTC derivatives, including interest rate swaps and CDS, to be cleared through central counterparties (CCPs). Furthermore, it mandated that they be reported to swap data repositories, giving regulators full visibility for the first time. Additionally, it required major swap dealers to register with the CFTC and maintain minimum capital standards.

EMIR in Europe

Similarly, the European Market Infrastructure Regulation (EMIR), implemented from 2012 onwards, imposed comparable requirements across European Union markets. Consequently, the global swaps market became significantly more transparent and better capitalised after both sets of reforms. Nevertheless, critics argue that systemic risks in swap markets persist, particularly in the less standardised corners of the market where CCP clearing does not yet apply.

Who Uses Swaps Today?

Swaps are used by an extraordinarily wide range of participants. Each group, moreover, uses them for distinct and legitimate purposes that are essential to modern financial markets.

Specifically, banks use interest rate swaps to manage the gap between the fixed-rate loans they issue and the floating-rate deposits they hold. Corporations, furthermore, use both IRS and currency swaps to manage the risk profile of their debt and international cash flows. Pension funds and insurance companies use swaps to match the duration of their long-term liabilities with assets. Finally, governments and sovereign wealth funds use currency swaps to manage foreign exchange reserves and cross-border financing needs.

Up Next

Derivatives and the Bigger Picture: Risk, Regulation, and the Road Ahead