You now understand the instruments. This final article examines who keeps derivatives markets safe, what history teaches us about risk, and where derivatives are heading next, from Bitcoin futures to ESG-linked contracts.

In Summary

First and foremost, derivatives serve genuinely productive economic purposes. They enable hedging, price discovery, and efficient risk transfer across the entire global economy.

Moreover, six major regulators, including the CFTC, ESMA, FCA, SEBI, MAS, and ASIC, oversee derivatives markets across their jurisdictions and coordinate globally through the FSB and G20.

Notably, the 2008 crisis triggered the most significant structural reform in derivatives history. Central clearing, trade reporting, and mandatory margin requirements have substantially reduced systemic interconnectedness since 2009.

However, significant risks remain in less standardised, bilaterally-cleared parts of the market. The 2021 Archegos collapse demonstrated that new vulnerabilities continue to emerge even after major reforms.

Furthermore, the future of derivatives is being shaped by three forces: the rise of crypto derivatives on regulated exchanges, the rapid growth of ESG-linked contracts, and the integration of artificial intelligence into pricing and risk management.

In particular, ESG-linked derivatives represent a genuinely new use case, directly linking financial instrument pricing to sustainability outcomes for the first time in financial market history.

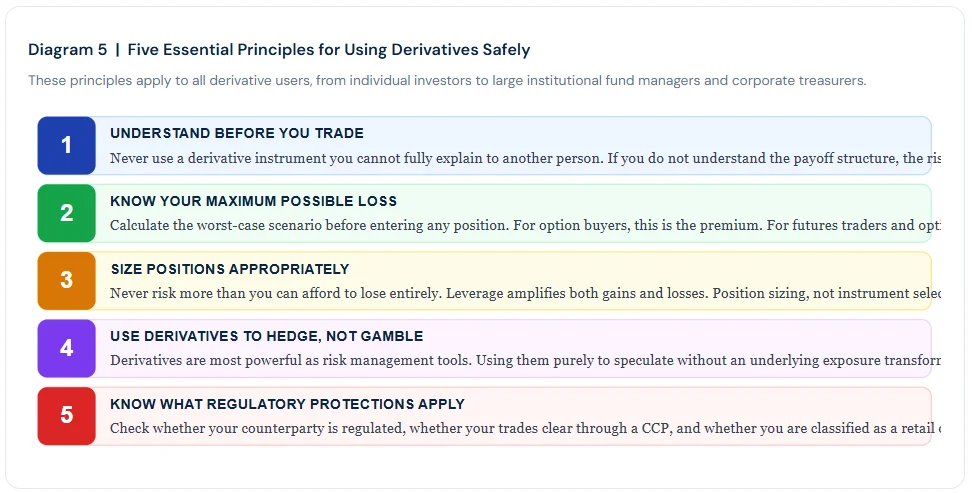

Additionally, the five principles of safe derivatives use apply universally: understand the instrument, know your maximum loss, size positions appropriately, hedge rather than gamble, and verify regulatory protections.

Finally, derivatives are not inherently dangerous. Their power lies in their flexibility. Used correctly, they remain indispensable tools for managing risk in a complex and uncertain global economy.

Table of Contents

- Table of contents will be generated automatically when the page loads.

Why Derivatives Matter to the Real Economy

Picture a world without derivatives. Farmers, in fact, would face devastating price swings at every harvest, unable to lock in revenues before planting. Airlines, moreover, would have no way to stabilise fuel costs months ahead. Banks, furthermore, could not efficiently manage the gap between fixed-rate loans and floating-rate deposits. Consequently, businesses worldwide would face far greater uncertainty and cost volatility than they do today.

Throughout this five-part series, we have explored each of the four main types of derivatives in depth. However, this final article takes a broader view. Specifically, it examines the regulatory frameworks that underpin market safety, the lessons history teaches about systemic risk, and the compelling innovations that are reshaping the derivatives landscape for a new generation of investors.

According to BIS research, non-financial corporations that use derivatives show significantly lower cash flow volatility than those that do not. Indeed, this confirms that derivatives serve a genuinely productive function in the real economy, well beyond the speculative uses that dominate headlines.

The Global Regulatory Landscape

Derivatives markets are regulated at the national level but coordinated internationally through the G20 and the Financial Stability Board (FSB). After the 2008 crisis, moreover, the FSB established a clear global reform agenda: all standardised OTC derivatives should be centrally cleared, all trades should be reported to trade repositories, and margin requirements should apply to non-cleared derivatives. Consequently, each major jurisdiction translated these principles into its own regulatory framework.

Notably, while each jurisdiction has its own rules, they share the same core principles: central clearing, trade reporting, margin requirements, and registration of major dealers. Furthermore, regulators cooperate actively through bilateral recognition arrangements, ensuring that a swap cleared in Chicago is also recognised under European rules. As a result, the global derivatives market functions with a degree of cross-border coherence that did not exist before 2008.

Lessons From Five Decades of Crises

Derivatives markets have experienced a series of high-profile failures since the 1990s. Each crisis, moreover, revealed a different vulnerability in how these instruments are used and managed. Consequently, understanding these events is as important as understanding the instruments themselves.

The Recurring Lessons

Each of these crises, in fact, taught the same core lesson in a different disguise. First, excessive leverage consistently transforms manageable losses into catastrophic ones. Second, opacity in OTC markets prevents regulators and counterparties from measuring true exposure until it is too late. Third, correlation risk means that strategies that appear hedged can fail simultaneously when extreme conditions emerge. Fourth, overconfidence in quantitative models leads institutions to underestimate the probability of tail events.

Notably, the 2021 Archegos collapse illustrates that new vulnerabilities continue to emerge even after major reforms. Specifically, Archegos used total return swaps (TRS) to build enormous concentrated positions in individual stocks without disclosing these to regulators or counterparties. When the positions collapsed, moreover, prime brokers rushed to sell simultaneously, triggering losses of over $10 billion across Credit Suisse, Nomura, and others. Consequently, regulators subsequently moved to require reporting of large TRS positions.

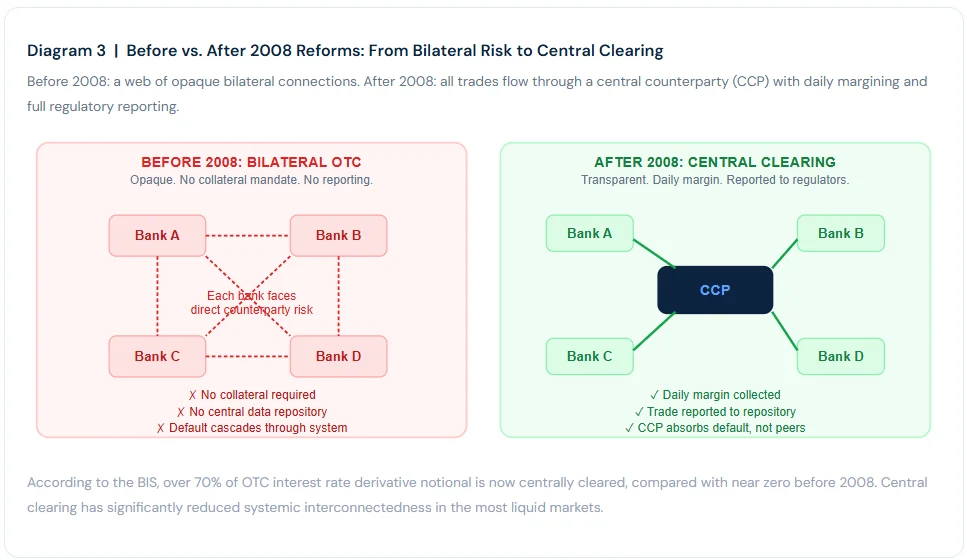

The Central Clearing Revolution

The most significant structural reform since 2008 is the shift from bilateral OTC trading to central clearing. Before 2008, the vast majority of interest rate swaps and CDS were traded bilaterally between banks, with no central entity guaranteeing performance. As a result, the failure of one major counterparty threatened to cascade through the entire system. Furthermore, no regulator had real-time visibility into the total network of exposures.

Nevertheless, significant risks remain in less standardised corners of the market. Specifically, bespoke credit derivatives, exotic structured products, and some commodity derivatives still trade bilaterally without central clearing. Furthermore, the concentration of clearing in a small number of CCPs creates its own systemic risk: if a major CCP itself were to fail, the consequences could be severe. As a result, CCPs are now subject to extremely stringent capital and stress-testing requirements from regulators worldwide.

The Road Ahead: The Future of Derivatives

Derivatives markets continue to evolve rapidly. Three forces, in particular, are reshaping the landscape for the next decade: the rise of crypto derivatives, the growth of ESG-linked contracts, and the integration of artificial intelligence into pricing and risk management.

Crypto Derivatives

Bitcoin futures launched on the CME in December 2017. Subsequently, Ether futures followed in 2021. These products brought institutional-grade risk management tools to the cryptocurrency asset class for the first time. Furthermore, the approval of Bitcoin ETF options in the US in 2024 marked another significant step toward mainstream integration. Nevertheless, crypto derivatives remain highly volatile, and regulatory frameworks across different countries are still evolving.

ESG-Linked Derivatives

Sustainability-linked interest rate swaps, in which the fixed rate adjusts based on a company’s ESG performance metrics, first appeared in 2019. According to ISDA’s ESG survey, interest in ESG derivatives has grown significantly among both corporate and investor communities. Carbon credit derivatives, moreover, enable companies to hedge and speculate on the price of CO2 emissions allowances. Consequently, these instruments play an increasingly important role in the transition to a lower-carbon economy.

A Framework for Using Derivatives Safely

Derivatives are not inherently dangerous. However, they do demand a higher level of knowledge, discipline, and risk awareness than most other financial instruments. The five principles below, moreover, apply equally to individual investors, corporate treasurers, and institutional fund managers.

In practice, the vast majority of derivative losses that make headlines involve violations of one or more of these five principles. Specifically, Nick Leeson at Barings broke rules 1, 3, and 4 simultaneously. AIG violated rules 2 and 5. Archegos violated rules 3 and 4 at extraordinary scale. Furthermore, retail investors who use leveraged crypto derivatives without understanding the mechanics regularly violate rules 1 and 2 simultaneously.

“Derivatives are like fire. When used properly, they can cook your food and keep you warm. Misused, they can burn your house down.”

-René Stulz, Journal of Applied Corporate Finance, widely cited in derivatives education