Options are the most versatile instruments in finance. They let investors protect portfolios, generate income, and bet on price moves with a strictly capped downside. This guide demystifies calls, puts, premiums, payoffs, and the Greeks in plain language.

In Summary

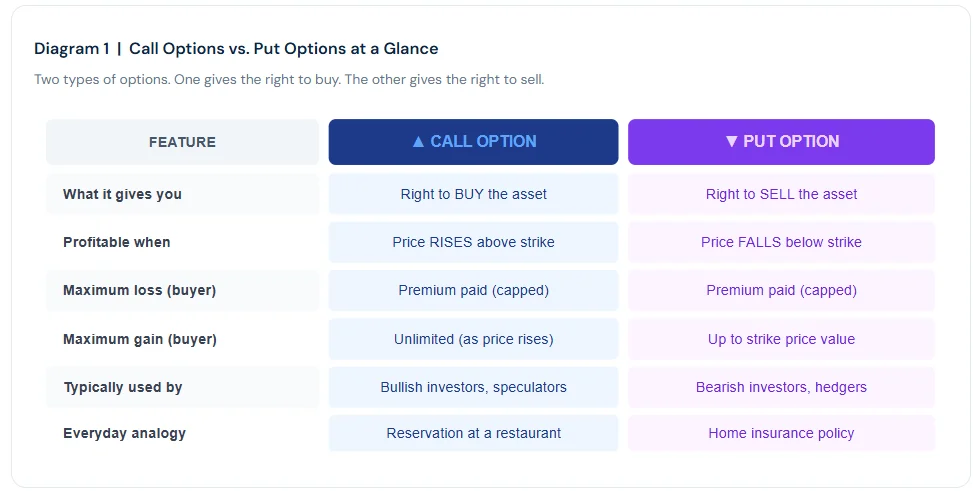

First and foremost, an option gives the buyer the right, but not the obligation, to buy or sell an asset at a fixed price on or before a specific date. This distinguishes options from all other derivatives.

Moreover, a call option gives the right to buy. A put option gives the right to sell. Both require the buyer to pay a premium to the seller up front.

Notably, the maximum loss for any option buyer is always capped at the premium paid, regardless of how far the underlying price moves against them.

By contrast, option sellers face very different risk profiles. Call sellers face theoretically unlimited losses. Put sellers face very large losses if the underlying falls sharply toward zero.

Additionally, option premiums consist of intrinsic value (how far in the money the option already is) and time value (the probability of further favourable movement before expiry).

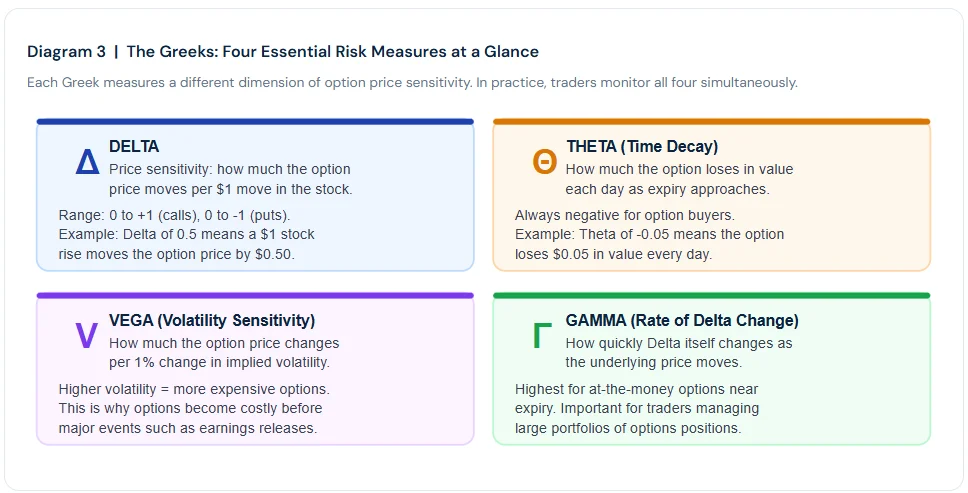

Furthermore, the Greeks measure four dimensions of option risk: Delta (price sensitivity), Theta (time decay), Vega (volatility sensitivity), and Gamma (rate of change in Delta).

In particular, Theta works against option buyers every day. Holding an option passively without a price move results in a steady erosion of premium value over time.

Finally, options serve three key purposes for investors: portfolio protection (protective puts), income generation (covered calls), and leveraged directional exposure with defined downside risk.

The House Insurance Analogy

Picture a homeowner in Sydney whose property is worth $800,000. Property prices, in fact, have risen sharply over recent years. However, she worries they might fall significantly before she can sell. Consequently, she buys home insurance. For an annual premium, the policy gives her the right to claim a payout if her home’s value declines. Notably, she is not obligated to make a claim if prices stay high. She simply has the option to act if conditions turn against her.

In financial markets, options work by exactly the same logic. Instead of insuring a house, investors use options to protect stocks, currencies, and commodities. Furthermore, options are not only defensive tools. They also allow investors to profit from price movements while limiting downside risk. This combination of flexibility and controlled risk makes them the most versatile instruments in the entire derivatives universe.

According to the Options Clearing Corporation (OCC), US options markets cleared a record 10.3 billion contracts in 2022. Indeed, this figure reflects just how central options have become to modern investing, hedging, and risk management worldwide.

What Exactly Is an Option?

An option is a contract that gives the buyer the right, but not the obligation, to buy or sell an underlying asset at a fixed price before or on a specific date. Specifically, the buyer pays a fee called a premium to obtain this right. In other words, the buyer is purchasing the possibility of a future transaction, not a commitment to complete one.

By contrast, a futures contract obligates both sides to transact at expiry. An option, moreover, gives the buyer a choice. If market conditions are unfavourable, the buyer simply lets the option expire worthless. As a result, the most an option buyer can ever lose is the premium already paid. This asymmetric risk profile sets options apart from every other derivative instrument.

Options trade both on regulated exchanges, such as the Chicago Board Options Exchange (CBOE), and in OTC markets between banks and institutional clients. Furthermore, they exist on virtually every asset class, including stocks, indices, currencies, interest rates, and commodities.

Call Options: The Right to Buy

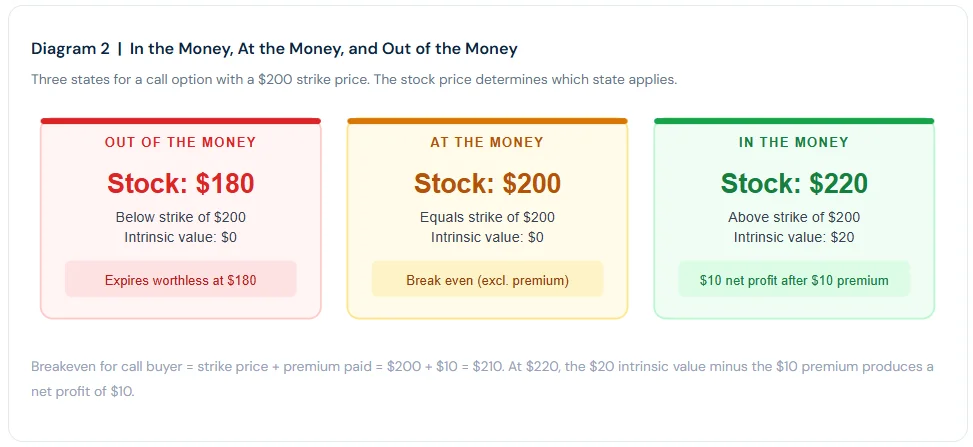

A call option gives the buyer the right to purchase an asset at a fixed price, the strike price, before or on the expiry date. For example, a call option on Apple shares with a $200 strike price and a $10 premium gives the buyer the right to buy Apple at $200, regardless of where the market price actually goes. Furthermore, the maximum loss is simply the $10 premium, regardless of how high or low the stock moves.

Consequently, if Apple rises to $240, the call buyer exercises the option, buys at $200, and earns a $30 profit after accounting for the premium. However, if Apple falls to $160, the buyer simply lets the option expire. As a result, the total loss is capped at the $10 premium paid, not the entire stock decline.

Put Options: The Right to Sell

A put option gives the buyer the right to sell an asset at the strike price before or on the expiry date. In other words, it is the financial equivalent of insurance. Just as the Sydney homeowner paid a premium for protection against falling property prices, a put buyer pays a premium for protection against a falling stock price.

For instance, a put option on Apple with a $200 strike protects the holder if Apple falls to $150. Specifically, the put buyer can sell Apple at $200 even though the market price is only $150, generating a $40 gross profit minus the premium paid. Nevertheless, if Apple rises or stays above $200, the put expires worthless, and the buyer loses only the premium.

The Key Terms Every Option Investor Must Know

Strike Price

The strike price, also known as the exercise price, is the fixed price at which the option can be exercised. Specifically, it is agreed at the time the contract is purchased and does not change. For a call option, the strike is the price at which the buyer can buy the asset. By contrast, for a put option, the price is the level at which the buyer can exercise the option to sell.

Premium

The premium is the price paid by the option buyer to obtain the contract. In practice, it has two components. First, intrinsic value represents how far the option is already in the money. Second, time value reflects the remaining time until expiry and the probability of further price movement. Notably, even an out-of-the-money option has time value, since the market might still move favourably before expiry.

Expiry Date

Every option contract has an expiry date. After this date, the option ceases to exist. Moreover, as expiry approaches, the time value portion of the premium declines steadily. This process is called time decay, and it works against option buyers while favouring option sellers.

How Option Payoffs Work

Every option position has a specific risk and reward profile. Notably, the buyer and the seller of the same option have exactly opposite payoff profiles. Understanding both sides, moreover, is essential for a complete picture of how options markets function.

The Call Option Payoff: Buyer and Seller

For the call option buyer, the payoff curve is asymmetric. Losses are strictly capped at the premium paid, regardless of how far the underlying falls. Gains, furthermore, are theoretically unlimited as the underlying price rises. By contrast, the call seller receives the premium upfront but faces unlimited potential losses if the price rises sharply above the strike.

The Put Option Payoff: Buyer and Seller

For the put option buyer, the payoff is the mirror image of the call option’s payoff. Specifically, the buyer profits as the underlying price falls below the strike. Maximum gain equals the strike price minus the premium (achieved if the asset falls to zero). Moreover, maximum loss remains capped at the premium paid, no matter how high the underlying price rises.

The put seller, by contrast, receives the premium upfront. However, significant losses arise if the underlying price falls well below the strike price. Consequently, put sellers must be confident in the stability or growth of the underlying asset before entering this position.

The Greeks: Measuring Option Risk

Options traders use a set of risk measures known as the Greeks. Each Greek measure, specifically, quantifies how sensitive an option’s price is to a particular factor. Understanding these measures, furthermore, is essential for managing an options portfolio effectively.

In practice, most individual investors focus mainly on Delta and Theta. Delta, specifically, indicates how much their option position will gain or lose from a given move in the stock price. Theta, furthermore, reminds them that time is always working against option buyers. As a result, buying options and holding them passively is a costly strategy over time, since Theta erodes the premium every day regardless of price action.

Vega, by contrast, becomes especially important around major corporate events such as earnings announcements. Implied volatility typically rises sharply before such events, making options more expensive. After the announcement, volatility often collapses rapidly, even if the stock moves in the expected direction. Consequently, this phenomenon can cause option buyers to lose money even when they correctly predict the direction of the move.

Why Options Matter for Investors

Options serve three broad purposes for investors. First, they provide portfolio protection. A put option on a stock or index allows an investor to limit downside losses while maintaining full upside exposure. In fact, this is the financial equivalent of the home insurance policy described at the start of this article.

Generating Income With Options

Second, options allow investors to generate additional income from stocks they already own. A strategy called the covered call involves selling a call option on shares the investor already holds. Consequently, the investor receives the premium upfront. However, if the stock price rises above the strike price, the shares are called away at that price. Moreover, many income-oriented investors use this strategy systematically to generate monthly returns.

Gaining Leveraged Exposure

Third, options offer leveraged exposure to price movements with a strictly defined maximum loss. Specifically, buying a call option on a $200 stock for a $10 premium gives full upside participation for only a $10 outlay per share. By contrast, buying the stock directly costs $200 per share. As a result, options can amplify returns considerably from a given capital investment. Nevertheless, the time decay factor means that timing must be much more precise than with a direct stock purchase.

Key insight for beginners

Options give buyers asymmetric risk profiles. The most an option buyer can ever lose is the premium paid. However, the seller of an option faces potentially unlimited risk on calls and very large risk on puts. Always understand which side of the trade you are on before entering any options position.

Up Next

Swaps: The Hidden Giants of the Derivatives World