July 04, 2026 – Tokenized finance promises cheaper settlement and better collateral mobility. However, faster markets can also transmit stress with less warning.

In Summary

Tokenization can consolidate execution, clearing, and settlement into a single programmable process.

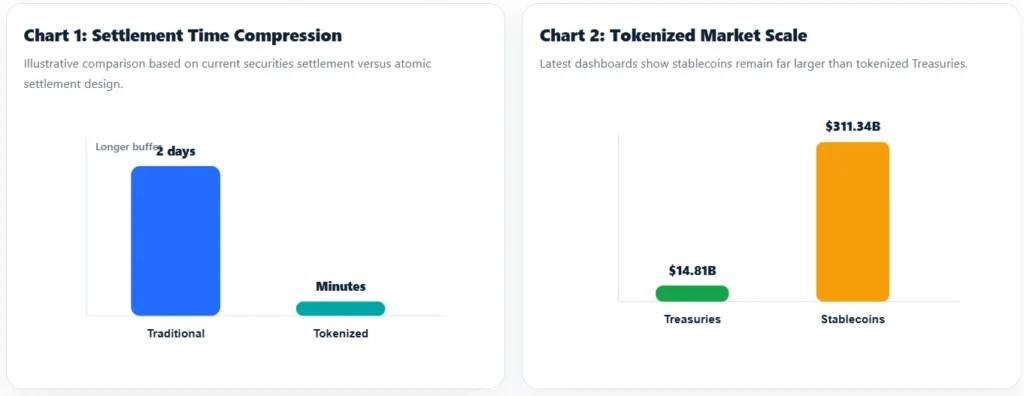

Faster settlement removes delays, yet those delays often act as safety buffers.

Market risk may shift from banks to platforms, smart contracts and shared ledgers.

Regulators now face urgent questions on legal finality, liquidity support and cyber resilience.

Tokenized Treasuries show adoption, but stablecoins still dominate tokenized money at scale.

Tokenization risks have moved from theory into policy debate. The latest IMF analysis says tokenization can make finance faster, cheaper and more programmable. Yet it also warns that speed can weaken shock absorbers.

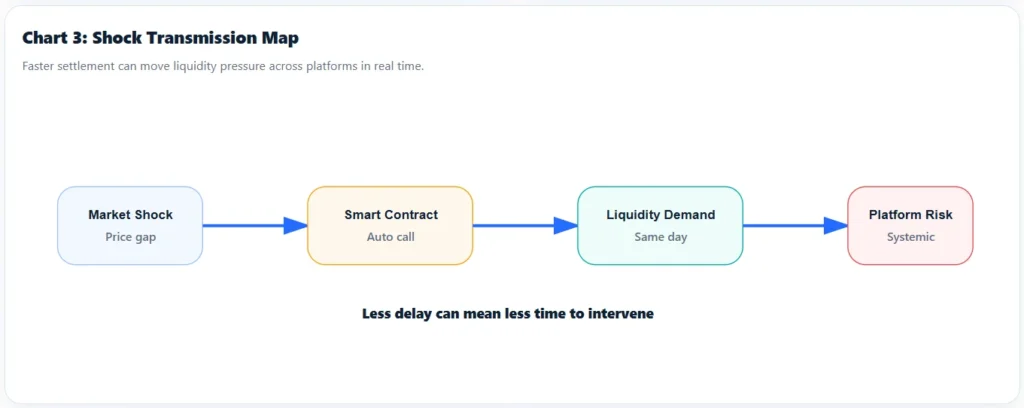

That creates a sharp market dilemma. Finance wants instant settlement, lower friction and cleaner records. However, the same upgrade can reduce reaction time during stress. In tokenized markets, trades, ownership transfers and payments can settle together. Smart contracts can also trigger margin calls without human delay.

This is why the story matters for banks, asset managers and regulators. Tokenization is not just a crypto trend. The IMF tokenized finance note calls it a structural shift in financial architecture. It changes settlement, liquidity, compliance and risk control.

Why faster settlement creates new pressure

Traditional finance looks slow because many steps happen in sequence. A trade gets executed first. Then clearing, settlement and reconciliation follow. These steps add cost. However, they also create time to detect errors, fund positions and contain stress.

Tokenized finance compresses those steps. A token can carry ownership data, transfer rules and settlement logic. Therefore, platforms can move assets and cash simultaneously. That can reduce operational drag across securities, payments, and collateral.

However, instant settlement changes liquidity management. A bank may need cash faster. An asset manager may face automated collateral calls. A platform outage may also block many users at once. As a result, operational risk can become market risk.

The bigger issue is concentration

The most important risk is not only speed. It is the concentration of activity on shared infrastructure. When many firms use the same ledger, that ledger becomes critical market plumbing. A coding flaw, cyber incident or governance failure can then travel widely.

The IMF warns that risk can move away from individual balance sheets. It can then concentrate in platforms, validators, or smart-contract operators. That shift matters because today’s rules focus heavily on banks, brokers and funds.

The market already shows scale. Tokenized U.S. Treasury products reached $14.81 billion in distributed value. Meanwhile, stablecoins stood near $311.34 billion in market value. These numbers show adoption, but they also show uneven maturity.

Stablecoins remain the first stress test

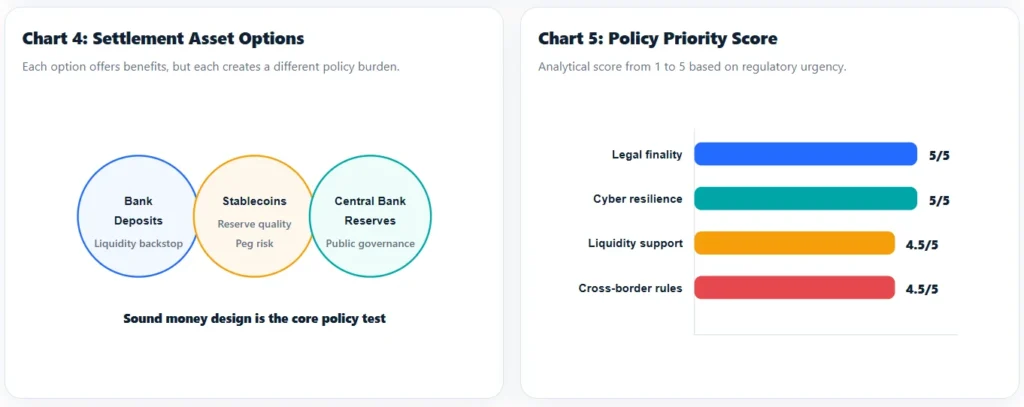

Stablecoins are the largest live test of tokenized money. They allow fast digital transfers and 24-hour settlement. Yet they depend on reserves, liquidity and redemption confidence.

The BIS policy update warns that broader adoption of stablecoins could affect banks’ funding and credit provision. It also says dollar-linked stablecoins may raise capital-flow risks in weaker economies.

This is vital for emerging markets. Dollar stablecoins can support payments. However, they can also speed currency substitution during stress. That creates a policy problem for central banks with fragile exchange rates.

What regulators need to fix

The first fix is legal certainty. Market users must know whether a token proves ownership. They also need clarity on settlement finality and applicable law.

The second fix is liquidity design. Real-time settlement requires real-time funding support. Without that support, faster systems can create faster gridlock.

The third fix is cyber resilience. Tokenized finance creates fewer manual breaks. Therefore, supervisors need stronger testing, recovery plans and governance standards.

The final fix is international coordination. Tokenized assets can cross borders quickly. Local rules alone may not protect investors or monetary stability.

Market outlook

Tokenization will likely expand first in regulated wholesale markets. Treasuries, money-market funds and collateral workflows offer clear use cases. Banks also have incentives to test tokenized deposits.

Still, mass adoption needs trusted settlement assets. It also needs credible legal wrappers and transparent operating rules. Without these safeguards, tokenization may remain a fast but fragile layer.

The bullish case is strong. Tokenization can improve settlement, unlock collateral and reduce reconciliation costs. Yet the warning is equally clear. Faster finance needs stronger guardrails, not weaker ones.

For investors, the message is simple. Watch growth, but also watch market plumbing. In tokenized finance, infrastructure quality may matter as much as asset quality.