July 10, 2026 – A group of 17 global banks will pilot live transactions on Swift’s new shared ledger, pushing round-the-clock cross-border payments closer to reality.

In Summary

Swift’s blockchain ledger is ready for its first live use with 17 major banks.

The pilot spans six continents and targets 24/7 cross-border payments.

Banks will move tokenised deposits, while existing rails still handle final settlement.

Speed is the goal: the G20 wants 75% of payments cleared within one hour by 2027.

The Swift blockchain ledger is now ready for its first live use. So 17 major banks will soon pilot real payments on it. These banks span six continents, and their reach shows strong global demand. Together, they want to move money around the clock across borders.

Swift shared the news on Thursday. It called the step a big moment for regulated digital money. The banks will use tokenised deposits to send funds. In short, tokenised deposits are digital forms of normal bank money.

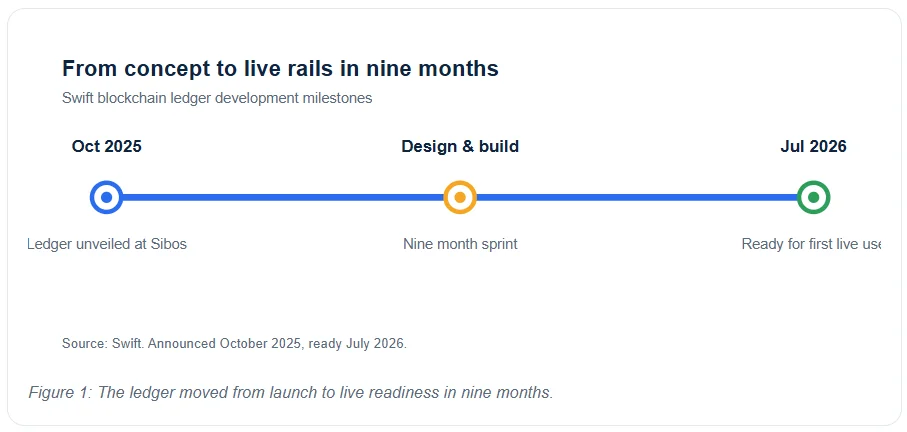

Swift built the ledger in just nine months. It first showed the plan last October at its yearly Sibos event. Now the work has moved from an idea to live rails. So the pace here is fast by banking standards.

Why the Swift blockchain ledger matters

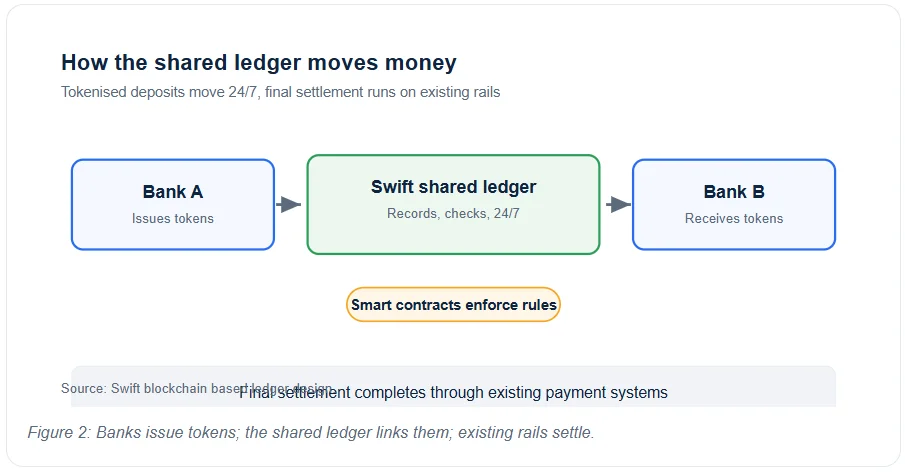

The new platform provides banks with a single shared layer for these digital tokens. Each bank still issues its own tokens on its own books. But the ledger lets them all link up in one place. So funds can move even at night and on weekends.

Final settlement still runs through today’s payment systems. In other words, the ledger adds speed without ripping out old rails. It records, sorts, and checks each payment in real time. Smart contracts then enforce the rules on every transfer.

Thierry Chilosi is Swift’s chief business officer. He said the tool brings the trust of old finance into digital money. Meanwhile, banks gain smoother cash flow and keep their risk checks intact. That balance is the whole point of the design.

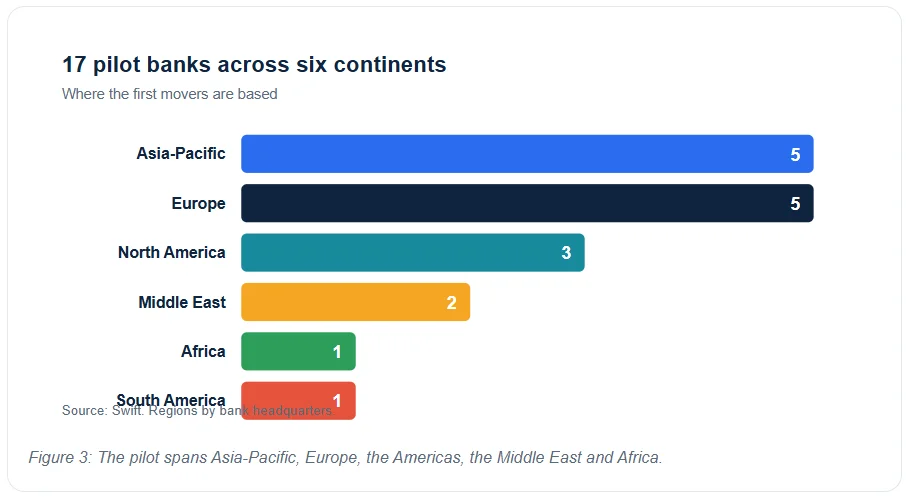

A roster spanning six continents

The pilot group reads like a map of world finance. For example, it includes UBS, BNP Paribas, Citi, and Wells Fargo. HSBC joined too, alongside Asian names such as DBS and MUFG. Middle Eastern banks like Mashreq and First Abu Dhabi Bank signed on as well.

Many of these banks already run their own token rails. HSBC, for instance, lets clients send funds abroad 24/7 on-chain. But each bank’s system has sat on its own island. So the shared ledger aims to connect those islands into a single network.

This matters for big firms with cash in many places. Right now, they wait for local cut-off times to clear. With always-on rails, they can shift money the moment they need it. Thus, treasury teams gain real control over their global cash.

Better liquidity is the quiet win here. Idle cash trapped in one branch costs firms money. So faster moves free up funds for real work. In turn, that saving flows straight to the bottom line.

Tokenised deposits versus stablecoins

Stablecoin firms already offer transfers that clear outside bank hours. So banks feel real pressure to match that speed. Yet they point to rules, checks, and risk controls as key concerns. Tokenised deposits let them answer both needs at once.

These tokens sit inside the regulated banking system. Each one still counts as a claim on a real bank deposit. As a result, banks keep their guardrails while gaining fresh speed. That mix is why the model appeals to cautious lenders.

Speed is still the real prize

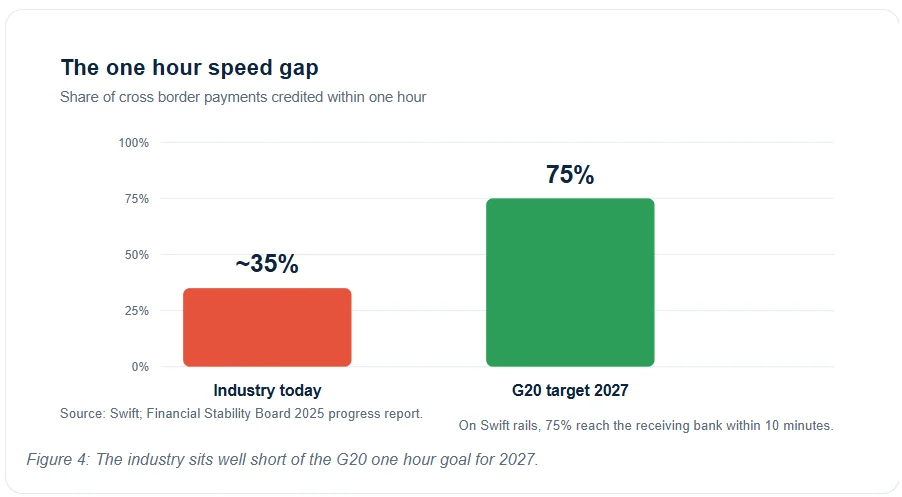

Cross-border payments have grown much faster in recent years. Indeed, 75% of SWIFT payments reach the receiving bank within 10 minutes. Many even land in seconds. Yet the last leg of the trip often drags.

Local checks at the receiving end can stretch delivery to days. Rules, time zones, and manual steps all slow things down. So the middle mile is quick, but the final mile lags. This is the gap where always-on rails could help the most.

Meanwhile, the stakes are tied directly to global policy. The G20 aims for 75% of these payments to be cleared within one hour by 2027. But only about a third clear that fast today. Clearly, the industry has a large gap left to close.

Because banking hours and time zones cause delays, non-stop settlement offers a fix. Tokenised deposits on shared rails could shrink much of that gap. So this pilot is more than a tech test. It is a direct answer to a stubborn global problem.

What comes next

Swift plans to widen the ledger’s features after this first phase. First, the pilot must prove that the live value moves safely. Then broader access and richer tools should follow. The rollout stays careful and staged on purpose.

Behind it sits a network that already carries huge weight. In fact, Swift moves the equivalent of world GDP every two to three days. It links more than 11,500 firms across over 200 markets. So even a small upgrade here ripples across the whole system.

For now, this pilot marks a turning point for digital assets. Old banking hours are fading, and money is edging toward true round-the-clock movement. Firms that manage cash across time zones stand to gain the most. Ultimately, the goal is simple: money that never has to wait.