July 03, 2026 – A softer 2026 outlook, data centre grid strain, and cheaper aluminium now threaten copper’s record run.

In Summary

Goldman Sachs sees LME copper easing to a $10,000–$11,000 range across 2026.

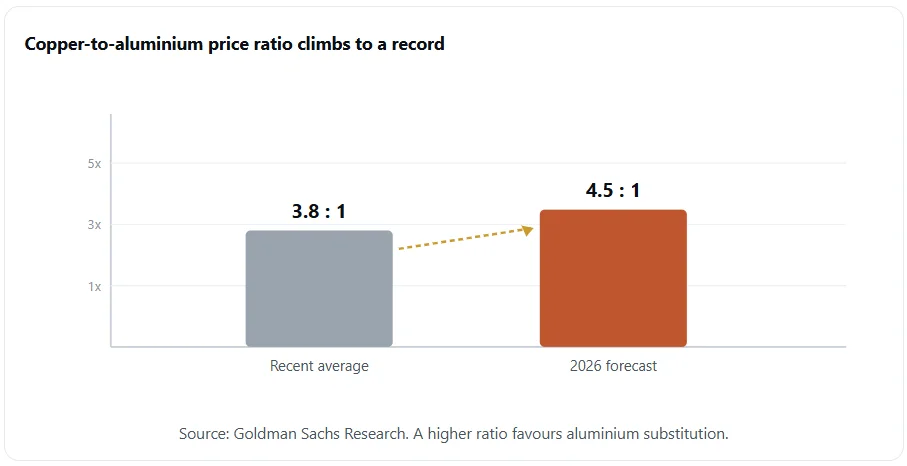

The copper-aluminium price ratio should push to a record 4.5:1.

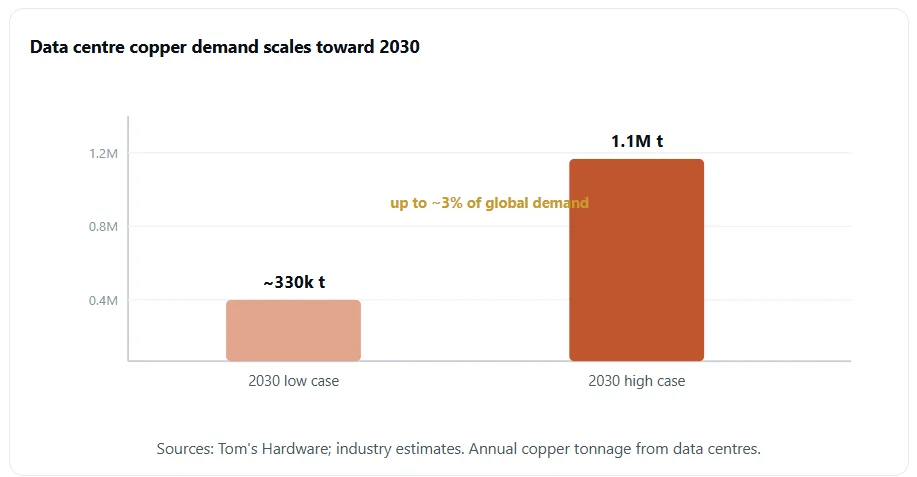

Data centres may absorb up to 1.1 million tonnes of copper a year by 2030.

Grid strain and permitting friction are slowing some large builds.

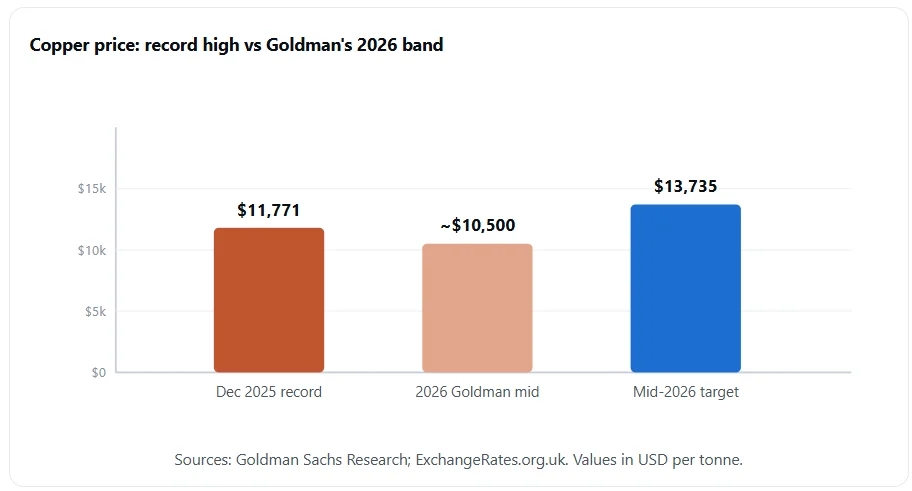

By mid-2026, Goldman had firmed its end-2026 target toward $13,735 a tonne.

Copper’s record run could slow through 2026. A copper-aluminium pivot is now reshaping how buyers source power metals. Meanwhile, cheaper aluminium and data centre grid strain pile on fresh pressure. So the metal’s rally now faces a real speed bump. This piece breaks down the drivers, the data, and the risks.

Why the copper rally is cooling

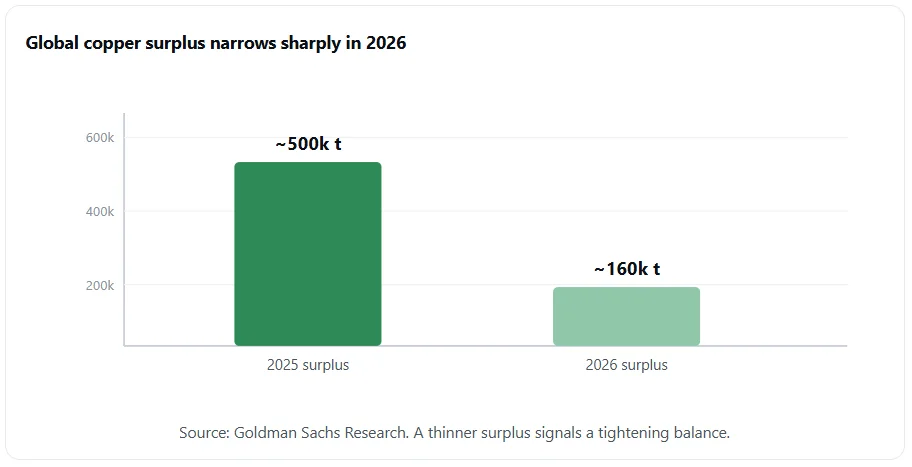

Goldman Sachs expects copper prices to ease from record highs in 2026. The bank sees LME copper trading between $10,000 and $11,000 this year. It also forecasts a smaller global surplus near 160,000 tonnes. Furthermore, Chinese refined copper demand fell about 8% in late 2025. China buys close to half of the world’s refined copper. Therefore, softer Chinese demand weighs on the whole market. A thinner surplus still points to a slow tightening ahead.

The copper-aluminium pivot explained

High prices make the switch to aluminium far more appealing. Goldman expects steady switching from copper to aluminium in many goods. Consequently, the copper-to-aluminium price ratio should reach 4.5:1 in 2026. That level tops the recent average of 3.8:1. Aluminium prices, by contrast, may slip toward $2,350 a tonne by year-end. So the cost gap between the two metals keeps widening. Makers of white goods and cars feel this gap first. Even a small price cut can flip a design choice.

Where aluminium wins ground

Data centre engineers now trim metal use per megawatt. Aluminium wires and busbars can replace copper in some power lines. However, aluminium cables must grow thicker to carry the same load. Thus, tight server halls still limit a full switch. Rio Tinto and Prysmian are even trialling low-carbon aluminium cables for the sector. Their work aims to reduce carbon emissions from data centre power gear. On the data side, fibre optics already displaces copper for signals. Yet copper still rules power delivery, where aluminium struggles to match it.

Tariffs reshape copper flows

US trade policy reshaped copper flows through 2025. Washington set a steep tariff on some copper imports in August 2025. Importers then rushed to stock up before the tax landed. As a result, US warehouses swelled while other regions drained. This split pushed regional prices apart. The stockpiling drive pulled in roughly 600,000 tonnes of metal. In turn, copper spiked to about $13,387 a tonne in early January 2026. Buyers outside America paid up for scarce spot metal. Traders are now closely watching the next US tariff move.

Data centre demand still looms large

The AI build-out stays a powerful driver for copper. Data centres could use up to 1.1 million tonnes of copper a year by 2030. That figure equals close to 3% of total global demand. Rio Tinto cites data indicating that data centres account for about 7% of North American cable demand in 2025. Moreover, that cable segment may grow by nearly 17% a year through 2030. Aluminium should grab a rising share of that growth. S&P Global sees total copper demand nearing 42 million tonnes by 2040.

The data centre speed bump

Grid strain is already slowing several large builds. Operators now build private gas plants to skip strained networks. In addition, permit delays and power access push timelines out. These frictions cool the near-term copper pull from AI. Still, the long-term shortfall case stays firmly intact. Chile’s mine output fell by roughly 210,000 tonnes in 2025. New mines can take up to 25 years to reach output. UBS even sees a copper deficit above 400,000 tonnes in 2026.

The long game still favours copper

Beyond 2026, most analysts stay bullish on copper. Clean energy needs vast amounts of the metal. Electric cars use three to four times as much copper as petrol models. Grids, wind farms and solar plants all lean on copper. Therefore, demand should overtake supply later this decade. Goldman even flags $15,000 a tonne as possible by 2035. That target would reward fresh investment in mines. The IEA sees grid copper demand rising toward 7.5 million tonnes by 2040. Meanwhile, falling ore grades force miners to dig deeper for less metal. Still, high prices invite yet more aluminium substitution.

What it means for investors

The 2026 outlook has since firmed. By mid-2026, Goldman lifted its end-2026 target toward $13,735 a tonne. Yet bank forecasts still vary widely. Deutsche Bank sees prices near $10,600 for the year. The World Bank pencils in a softer $9,800 average. So the spread of views stays unusually wide. Meanwhile, the pivot risk clearly persists beneath the bullish surface. If copper stays costly, aluminium keeps winning share. Investors should track the copper-to-aluminium ratio closely. This analysis is informational only and not investment advice.