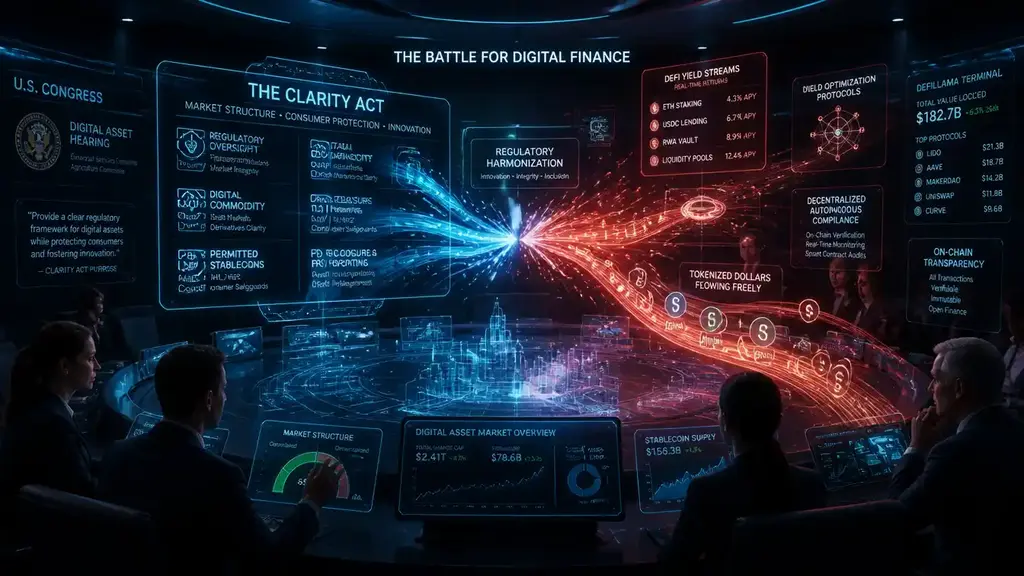

Catenaa, Monday, May 25, 2026- The US Senate’s proposed CLARITY Act is accelerating a new race across the crypto industry to redesign stablecoin yield products around artificial intelligence and decentralized finance as lawmakers move closer to banning passive interest payments on regulated dollar-backed tokens.

The latest Senate draft extends restrictions beyond stablecoin issuers to exchanges, brokers and custodial platforms, effectively blocking firms from offering traditional annual percentage yields on idle stablecoin balances. Industry executives and compliance specialists say the restrictions could reshape how crypto yield products function across the US financial system.

The legislation expands earlier provisions contained in the GENIUS Act and seeks to prevent stablecoins from operating like unregulated bank deposits. Under the proposal, regulators would treat any passive yield mechanism resembling savings account interest as equivalent to a banking product.

The restrictions emerged after months of negotiations involving crypto firms, banking groups and White House officials. Traditional financial institutions argued that stablecoin rewards create shadow banking systems capable of pulling deposits away from regulated lenders.

Policy analysts linked to the White House Council of Economic Advisers estimated that banning passive stablecoin yield could increase bank lending activity while reducing consumer benefits tied to crypto-based savings products.

The debate comes as stablecoins increasingly dominate crypto trading, decentralized finance liquidity and cross-border digital payments. Global stablecoin circulation has expanded rapidly since 2024, intensifying regulatory pressure in Washington and Europe.

Crypto firms are now developing alternative yield structures that depend on active transaction routing rather than direct interest payments. Industry executives describe the emerging model as “Yield-as-a-Service,” where AI systems automatically move stablecoin liquidity across decentralized finance protocols to capture trading fees, lending spreads and liquidity incentives.

Under the structure, AI agents monitor blockchain markets in real time, assess liquidity conditions and execute yield-generating trades through decentralized finance networks. The yield would technically originate from transactional activity rather than passive account balances, potentially fitting within carve-outs currently permitted under the CLARITY proposal.

Analysts say the shift could push crypto markets deeper into automated finance systems powered by artificial intelligence. It may also increase complexity and risk exposure for retail investors as yield generation becomes dependent on algorithmic trading systems and decentralized liquidity pools.

Some banking groups continue lobbying for tighter restrictions, arguing that even AI-routed stablecoin yield systems could threaten deposit stability inside traditional banks.

Compliance specialists say lawmakers are attempting to draw a legal boundary between banking products and blockchain-based transactional finance.

Crypto infrastructure firms argue the legislation may unintentionally accelerate financial automation by forcing yield generation into more complex decentralized systems rather than regulated centralized platforms.

Regulatory observers also warn that lawmakers could eventually tighten the transactional yield carve-out if decentralized finance products grow too rapidly or begin resembling synthetic banking systems.

Artificial intelligence developers working in decentralized finance say automated compliance systems may become necessary as crypto regulation becomes more fragmented across jurisdictions.

The CLARITY Act debate reflects a broader global struggle over how governments should regulate digital dollars and blockchain-based financial services. Stablecoins increasingly sit at the center of crypto trading, tokenized assets and international settlement systems, placing lawmakers under pressure to balance innovation with banking stability.

The emerging AI-driven yield model shows how quickly crypto markets adapt to regulatory pressure. Rather than eliminating yield products entirely, restrictions may instead shift financial activity toward decentralized protocols and automated execution systems operating beyond conventional banking infrastructure.

Whether regulators ultimately accept those structures may determine the next phase of competition between traditional banks, crypto firms and AI-powered financial networks.

Stablecoins emerged as one of the fastest-growing sectors in digital finance after 2020 because they allowed traders and institutions to move dollar-linked assets across blockchain networks instantly. Platforms later began offering passive yield products tied to those tokens, attracting billions of dollars from retail and institutional investors seeking returns higher than traditional savings accounts.

Regulators increasingly viewed those products as competing with commercial bank deposits without equivalent oversight or insurance protections. Banking groups warned that stablecoin-based yield systems could weaken traditional funding structures and increase financial instability during periods of market stress.

The US Congress responded by developing separate stablecoin frameworks including the GENIUS Act and the broader CLARITY Act. Both proposals seek to establish federal oversight for digital asset markets while limiting the ability of crypto firms to replicate core banking functions through blockchain infrastructure.