May 21, 2026 – NVIDIA posts record $81.6B in Q1 FY2027 revenue. Data Centre jumps 92%. EPS beats by 6%. The board raises its quarterly dividend 25-fold and approves $80B in new buybacks.

In Summary

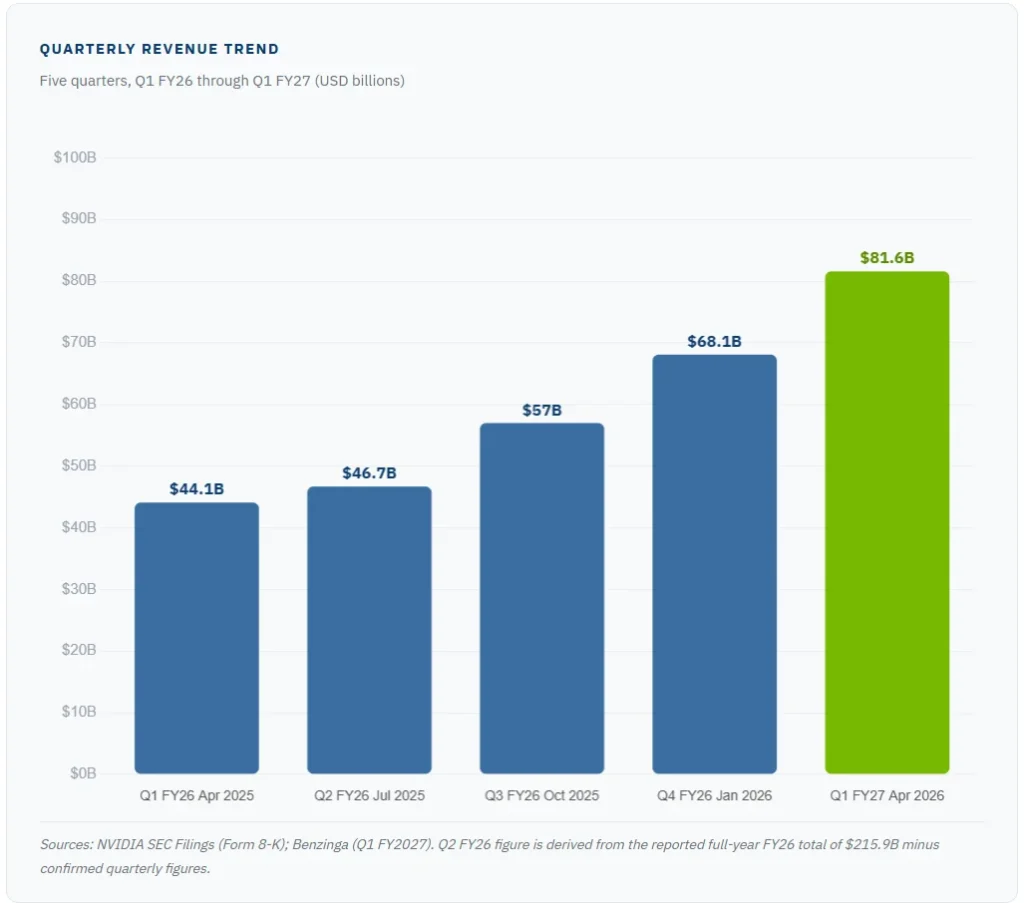

Q1 Revenue: $81.6B, up 85% year-over-year

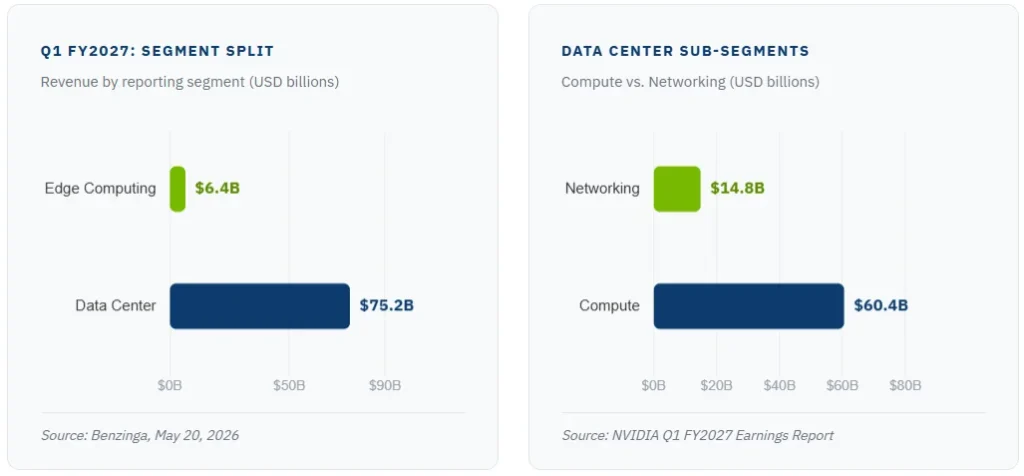

Data Centre: $75.2B, up 92% year-over-year

Quarterly dividend raised from $0.01 to $0.25 per share

EPS: $1.87, beating the $1.76 Street estimate

Edge Computing: $6.4B, up 29% year-over-year

Q2 FY2027 guidance: $89.2B to $92.8B, topping estimates

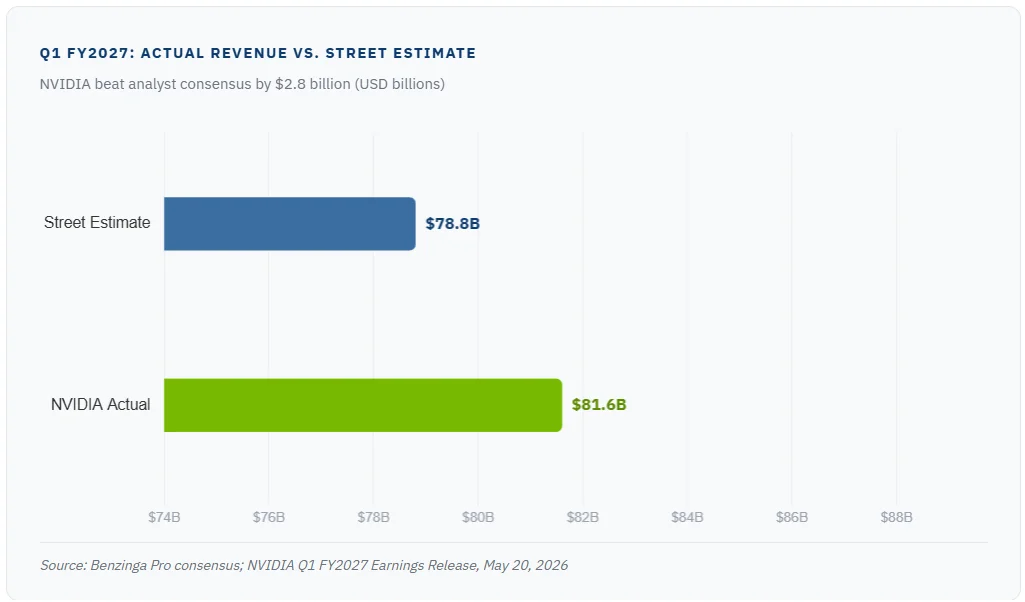

NVIDIA set another earnings record on May 20, 2026. The chipmaker reported Q1 FY2027 revenue of $81.6 billion. This beat the Wall Street consensus of $78.8 billion by $2.8 billion, per Benzinga Pro data. Furthermore, earnings per share of $1.87 topped the $1.76 estimate. Consequently, NVIDIA delivered a clear “double beat” on both key metrics.

The results came after a streak of thirteen consecutive blowout quarters. Analysts had debated whether growth could continue. However, Q1 FY2027 answered that question decisively. Revenue acceleration year-over-year actually increased compared to prior quarters.

Revenue Growth Accelerates Again

NVIDIA’s revenue grew 85% year-over-year in Q1 FY2027. This is notably faster than the prior quarter’s 73% growth rate. Therefore, the AI infrastructure demand cycle shows no signs of slowing. Additionally, the result came despite NVIDIA excluding all China data centre compute revenue from its Q2 outlook.

The company now uses two reporting segments. First, the Data Centre generated $75.2 billion, up 92% year over year. Second, the new Edge Computing segment added $6.4 billion, growing 29% from a year ago. Together, these segments signal NVIDIA’s expanding reach across the AI stack.

Data Centre: The Engine of Growth

Within the Data Centre, the granular data is equally striking. Compute revenue reached $60.4 billion, up 77% year-over-year. Furthermore, networking revenue soared to $14.8 billion, a 199% year-over-year increase, according to NVIDIA Newsroom filings. This spike reflects the rapid adoption of NVLink AI compute fabric and Ethernet AI platforms.

Hyperscale cloud customers remain NVIDIA’s largest Data Centre customer segment. However, enterprise and sovereign AI are growing faster. Analyst Daniel Newman of Futurum Group estimates hyperscaler capital expenditure at roughly $725 billion for 2026. Therefore, NVIDIA has an enormous structural runway ahead.

Jensen Huang: A Historic Buildout

The buildout of AI factories is accelerating at an extraordinary speed. Agentic AI has arrived, doing productive work, generating real value and scaling rapidly across companies and industries.

-Jensen Huang, CEO and Founder, NVIDIA Corporation

Huang described NVIDIA as the only platform running in every cloud. Moreover, it scales from hyperscale data centres to the edge. This positioning underpins NVIDIA’s pricing power. Consequently, the company maintained a gross margin of 75% in the quarter.

Gross margin met analyst expectations and held flat from Q4 FY26, according to CNBC and StreetAccount data. Additionally, NVIDIA invested $18.6 billion in private companies and infrastructure funds during Q1. Some of these companies may indirectly use NVIDIA products through cloud infrastructure.

Capital Returns: A 25-Fold Dividend Raise

NVIDIA announced two major shareholder return initiatives. First, the board approved $80 billion in additional share buybacks. Second, the quarterly dividend jumped from $0.01 to $0.25 per share, effective June 26, 2026. This 25-fold dividend increase signals strong management confidence in future cash generation.

The buyback program is larger in absolute terms and may have a greater near-term impact on share count. However, the dividend raise carries strong symbolic value. It signals that NVIDIA views its cash generation as both durable and predictable.

Q2 Guidance Tops the Street by $4 Billion

For Q2 FY2027, NVIDIA guided revenue of $89.2 billion to $92.8 billion. The midpoint of roughly $91 billion exceeds the Street estimate of $86.6 billion. Therefore, analysts expect the positive earnings trend to extend into the summer quarter.

However, NVIDIA included a notable caveat. The company is not counting any China data centre compute revenue in Q2 guidance. This reflects ongoing US export restrictions on advanced AI chips. Consequently, actual revenue could outperform guidance if policy conditions change.

What Analysts Are Saying

Gene Munster of Deepwater Asset Management called the revenue acceleration “remarkable.” He noted that NVIDIA is still working through noise related to China restrictions. Nevertheless, the underlying growth momentum is strong.

Tony Wang of T. Rowe Price added that agentic AI is rapidly expanding compute needs. Therefore, new AI application layers could drive incremental demand for years. Additionally, Kiplinger reported that sovereign AI spending tripled to over $30 billion in fiscal 2026. This geographic diversification reduces NVIDIA’s dependence on US hyperscalers.

However, China’s export restrictions remain a material risk. NVIDIA estimated it lost approximately $8 billion in Q2 H20 chip revenue due to export controls. Furthermore, the geopolitical landscape around semiconductor exports remains fluid and unpredictable.

New Segments Signal a Strategic Shift

NVIDIA introduced a new reporting framework this quarter. The company now separates the Data Centre from Edge Computing as distinct segments. Additionally, within the Data Centre, it plans to break out Hyperscale and ACIE (AI Clouds, Industrial and Enterprise) going forward. Management said this new structure better reflects current and future growth drivers.

Edge Computing generated $6.4 billion, growing 29% year-over-year. Although much smaller than the Data Centre, it still matters. However, the next few quarters will reveal whether this segment can sustain high-growth rates. Investors should monitor Edge Computing as a potential second growth pillar for NVIDIA.

NVIDIA’s Q1 FY2027 report confirms the AI infrastructure supercycle is still in full force. Revenue acceleration, stable margins, and aggressive capital returns all point in the same direction. Furthermore, guidance well above Street expectations leaves little room for bearish arguments. Consequently, NVIDIA remains the most pivotal company in the global AI infrastructure buildout.