June 23, 2026 – Billion-dollar startups cannot exit. Their backers want money back. Yet the zombie unicorn herd keeps on growing.

In Summary

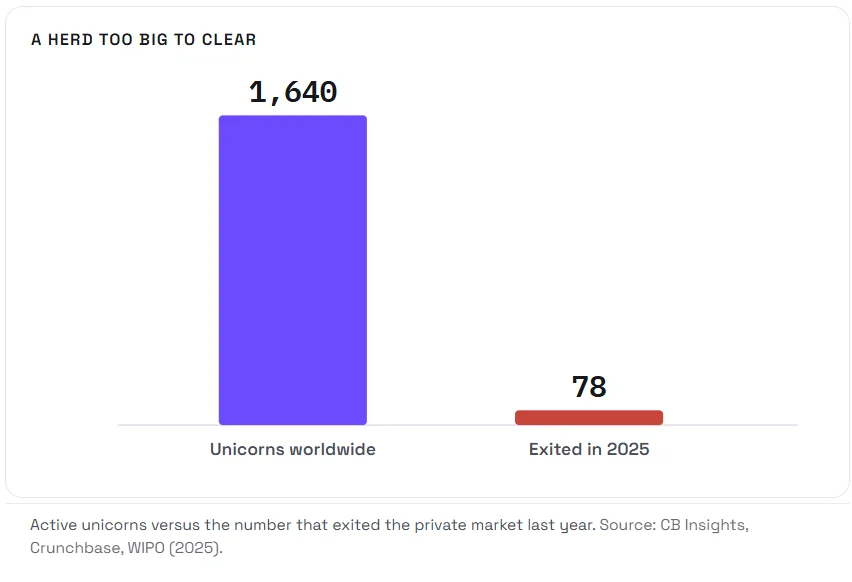

More than 1,600 unicorns now sit on private cap tables worth nearly $5 trillion.

Only 78 of them reached an exit during all of 2025.

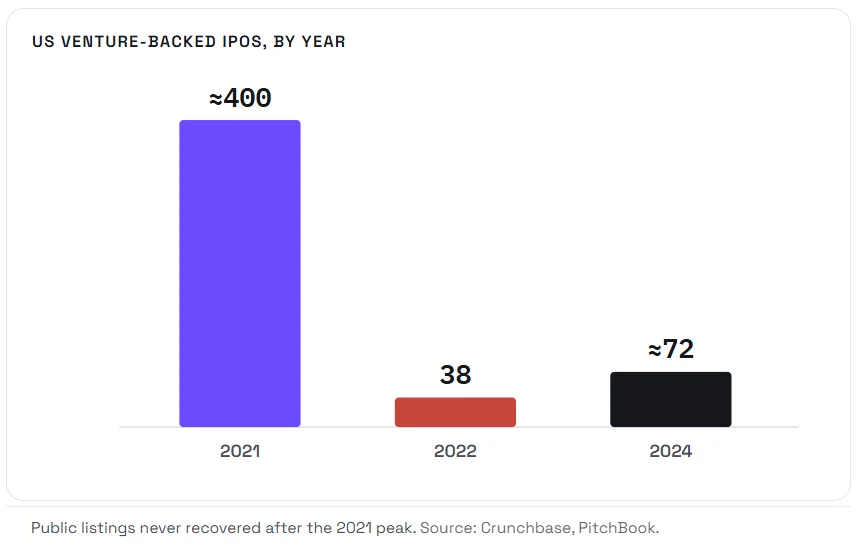

US venture-backed IPOs crashed from roughly 400 in 2021 to about 72 in 2024.

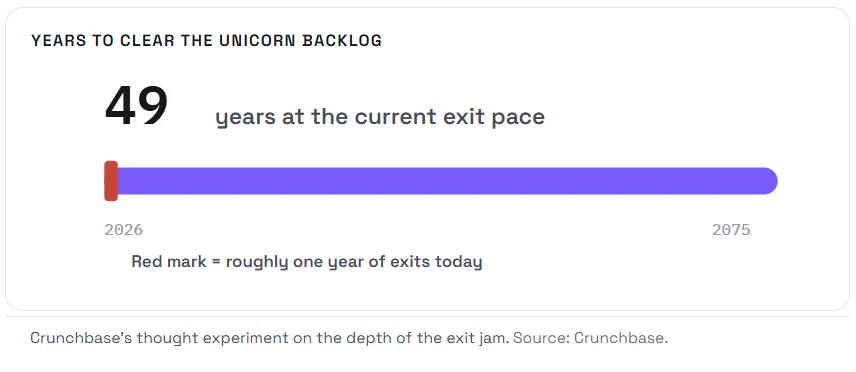

At today’s pace, clearing the backlog could take 49 years.

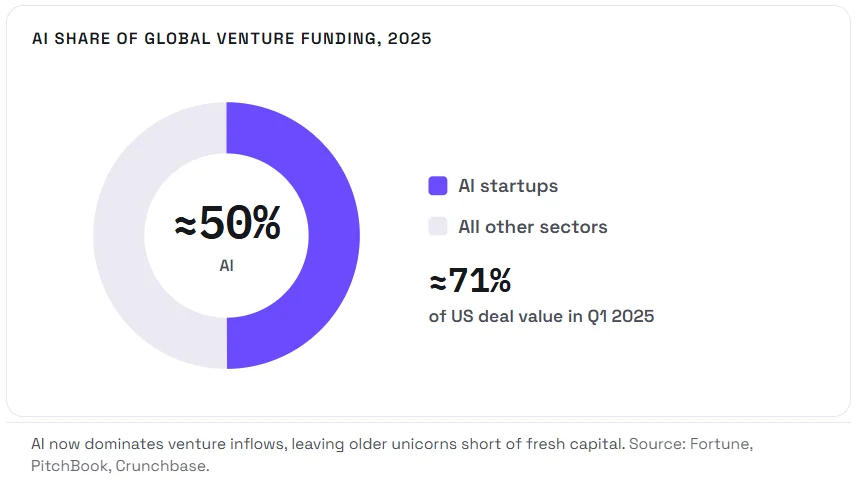

AI startups now grab nearly half of global venture funding, starving the rest.

A herd that cannot move

Silicon Valley faces a strange new monster. Investors call them zombie unicorns. These startups still carry billion-dollar valuations. Yet they cannot go public. They cannot find buyers either. Still, they refuse to die quietly.

The label sounds dramatic for a reason. A zombie unicorn looks alive on paper. In truth, it cannot grow or exit. Many simply burn cash while they wait.

This monster did not appear overnight. Cheap money built the herd for a decade. Then interest rates climbed sharply. Suddenly, the easy exits vanished.

The term is not brand new either. Venture investor Mike Maples Jr coined “zombiecorn” back in 2016. He spotted early cracks in the first unicorn wave. Today those cracks have turned into canyons.

Meanwhile, the herd keeps growing fast. The global unicorn club now holds more than 1,600 private firms. Their combined value neared $5 trillion in 2025, according to WIPO data. However, only a tiny share ever reaches a real exit.

Moreover, most of these firms raised money years ago. Roughly 40% of US unicorns have sat in portfolios for nine years or more. Therefore, their backers now demand returns. Yet the road to cash stays blocked.

The exit door stays shut

The IPO market tells the clearest story. In 2021, nearly 400 US venture-backed companies went public. The next year, that number collapsed to just 38. By 2024, only about 72 firms listed, Crunchbase data shows.

Consequently, the backlog now looks badly clogged. Crunchbase ran one striking calculation. At the recent exit pace, clearing the queue would take 49 years. The figure sounds absurd. Still, the math holds.

Public buyers have also grown picky. They now want profit, not just promises. As a result, few unicorns qualify for a clean listing. Many priced their last round in 2021. Today’s market no longer accepts those numbers.

M&A once offered a reliable backup. That route has narrowed as well. Antitrust reviews now stretch for months. Fewer big acquirers stay active in the market.

Secondaries have filled part of the gap. Investors traded roughly $293 billion of private stakes in 2025. Yet such deals only ease pressure. They do not clear the deeper backlog.

Why zombie unicorns get stuck

High prices now trap many founders. A fresh round often means a painful markdown. Therefore, leaders delay and hope for better days.

Researchers have long flagged the gap. Stanford’s Ilya Strebulaev estimates unicorns are overvalued by about 51%. In plain terms, paper value rarely meets real value. Consequently, a listing risks exposing that gap.

The danger runs deeper than vanity. Harvard’s Shikhar Ghosh found that roughly 75% of venture-backed firms never return investor capital. Many lose everything. The power law rules these portfolios.

Down rounds carry real damage too. They can wipe out staff equity overnight. Such resets can also trigger harsh investor clauses. So founders fight hard to avoid them.

Investors also resist marking down their books. A lower mark hurts fund performance. Therefore, some simply block a sale.

Employees feel the freeze most sharply. Stock options once promised life-changing payouts. Now many of those grants sit underwater. Without a listing, that wealth stays locked.

AI eats the funding

One corner of tech still booms loudly. Artificial intelligence now soaks up most of the venture capital. In 2025, AI captured nearly half of global venture funding, Fortune reports. Furthermore, a few giant rounds swallowed most of that total.

Investors call this split a barbell market. Capital piles into a handful of hot names. The long tail receives almost nothing. As a result, ordinary startups fight for scraps.

This surge also widens the divide. AI startups raise fresh billions with ease. Meanwhile, older unicorns in software, fintech, and consumer apps starve. Therefore, the gap between winners and zombies widens each month.

New AI unicorns even look leaner. They earn far more revenue per worker than older peers, CB Insights found. Yet that strength masks a wider weakness. Most of the herd still lacks a clear exit.

What comes next

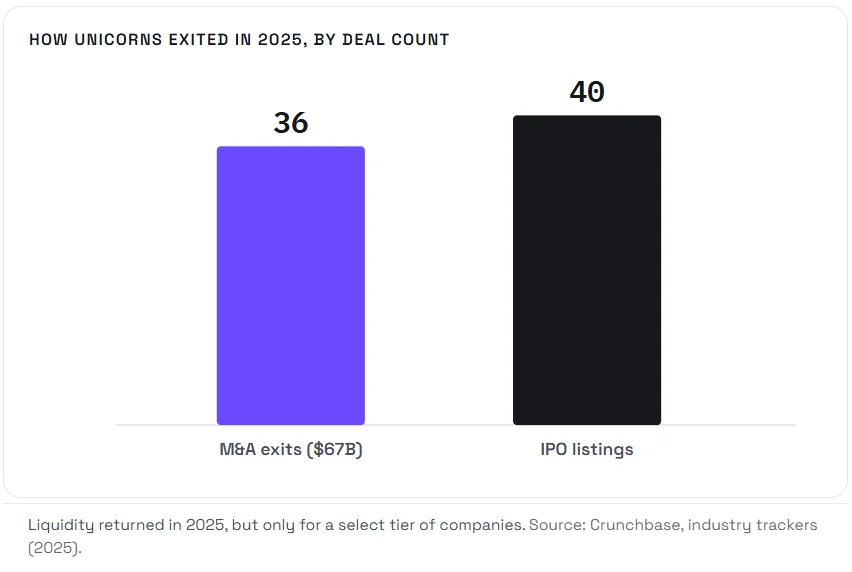

The outlook is not all dark. M&A activity rebounded sharply in 2025. Acquirers paid premium prices for prized AI and security assets. In addition, a handful of large IPOs tested the public mood.

Yet the relief stays narrow. PitchBook warns the market sits four years deep in a liquidity drought, PitchBook notes. Moreover, the pipeline of ready firms still looks thin.

Tangled cap tables add another problem. Years of mega-rounds left stacked preferences and rival agendas. As a result, simple choices now spark complex fights.

History also offers a blunt warning. WeWork once carried a $47 billion valuation. It later collapsed into bankruptcy. Other once-prized names have sold for scraps.

The pain also spreads beyond the founders. Suppliers, landlords, and recruiters all lose work. Whole local economies feel the slowdown. So the stakes reach far past venture funds.

Founders therefore hunt for creative exits. Many turn to structured equity to buy time. Others accept down rounds or quiet sales. Still, thousands remain trapped in zombie limbo.

A wider reopening needs steadier markets. It also needs lower rates and calmer politics. Until then, caution will rule boardrooms. Patience has become the only strategy left.

The bottom line

The unicorn era promised endless growth. Reality has proven far messier instead. Some founders will adapt and survive. A few will pivot toward steady profit. Others will wind down with dignity. Liquidity is returning, but only to a chosen few. Until exits reopen widely, the zombies will keep shuffling on.