May 09, 2026 – The OMB projects a $2.06 trillion deficit for FY2026. That is more than $166 billion in new borrowing every month. Budget experts warn that the risk of a fiscal crisis is rising fast.

In Summary

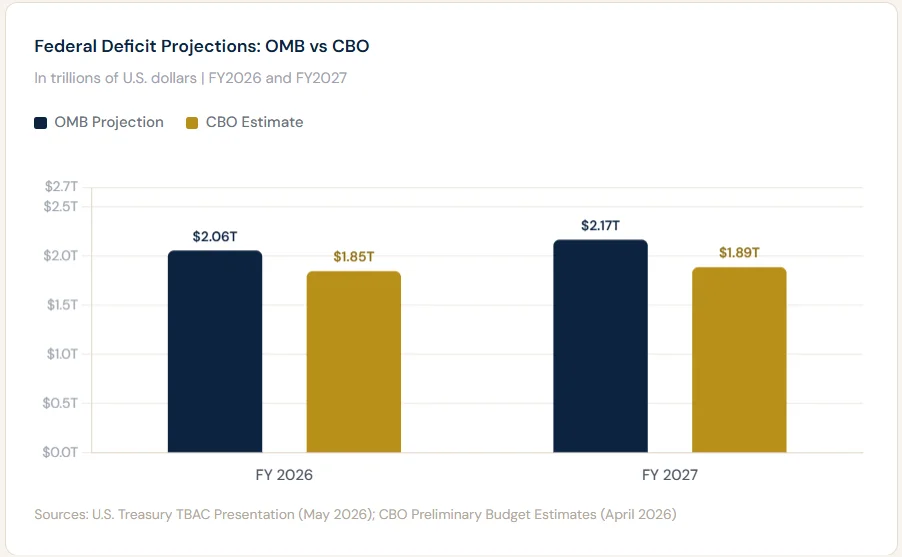

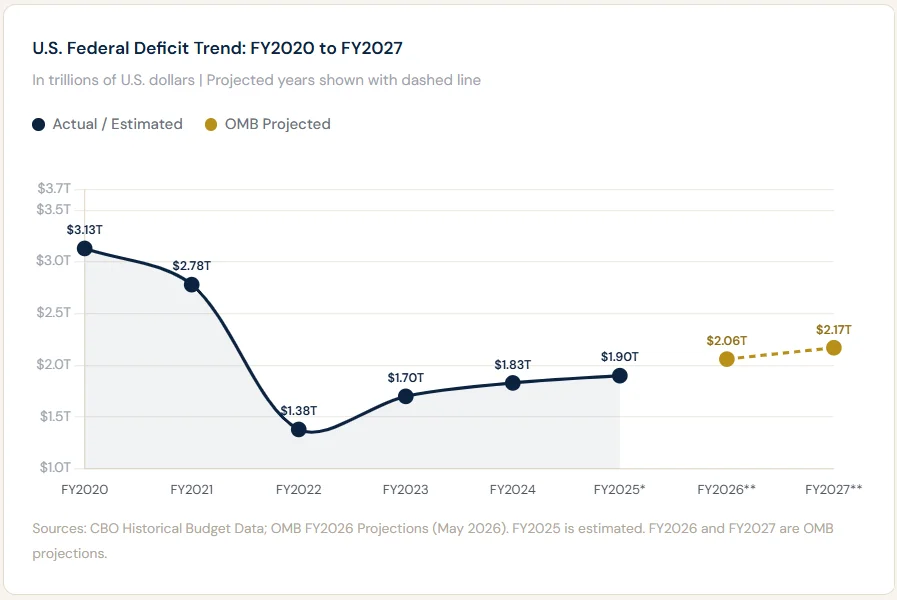

The OMB projects a FY2026 federal deficit of $2.06 trillion, above all pre-2020 peacetime records

The CBO offers a lower estimate of $1.85 trillion for the same period

Monthly debt issuance in FY2026 exceeds $166 billion; FY2027 rises to $181 billion per month

Treasury paid nearly $530 billion in interest payments in just six months (Oct 2025 to Mar 2026)

The current deficit equals more than 6% of GDP, double the proposed 3% target

U.S. national debt stands at $38.91 trillion as of May 2026, per Treasury fiscal data

The U.S. Treasury is on track to borrow more than $2 trillion in fiscal year 2026. That is a historic and deeply troubling milestone. The Office of Management and Budget (OMB) projects a deficit of $2.06 trillion for the current fiscal year. This figure equals more than $166 billion in new debt every single month. Budget analysts and independent economists are sounding urgent alarms. The trajectory suggests that US fiscal policy is on an unsustainable path. The risk of a genuine fiscal crisis is growing with each passing month.

A Record Pace of Borrowing

Not all forecasts agree on the exact scale of the deficit. The Congressional Budget Office (CBO) places the FY2026 deficit at $1.85 trillion. That figure is lower than the OMB’s projection. However, both estimates are staggeringly high by any historical standard, except during major crises or wartime spending.

These projections were published in the Treasury’s Quarterly Refunding Documents on May 7, 2026. The documents detail the U.S. debt management strategy and bond issuance plans. Treasury Secretary Scott Bessent oversees this process on behalf of the administration.

Furthermore, the outlook worsens heading into FY2027. The OMB projects the deficit will climb to $2.17 trillion next year. Monthly borrowing would then reach approximately $181 billion. That equals nearly $6 billion per day, or roughly $250 million per hour. In short, the pace of U.S. borrowing is accelerating, not slowing.

How Treasury Finances the Deficit

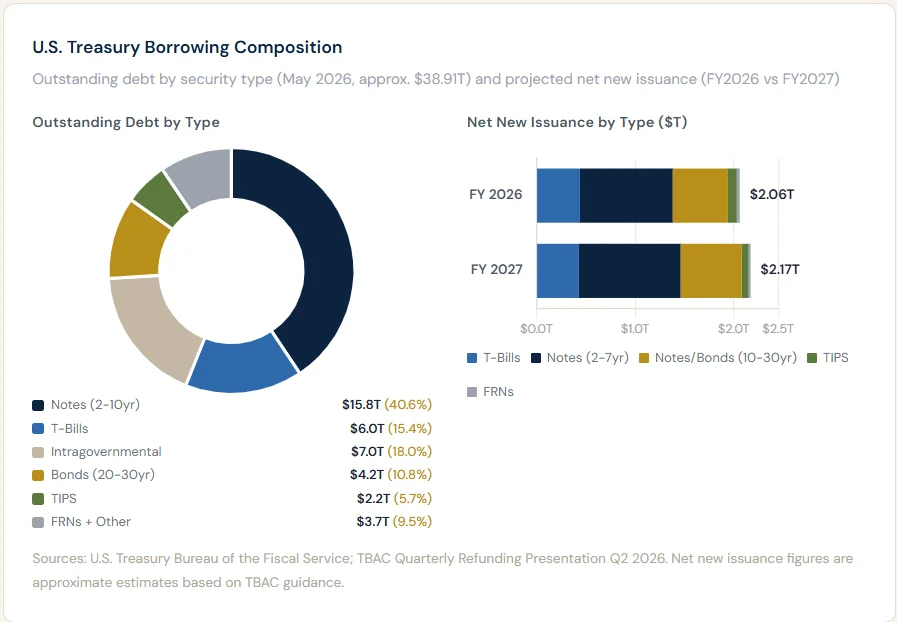

Understanding the record deficit also means examining HOW the Treasury borrows. The Treasury issues multiple types of debt securities. These range from short-term bills maturing in 4 to 52 weeks to long-term 30-year bonds. The composition of this borrowing matters greatly. Short-term bills cost less now but require frequent refinancing. Long-term bonds lock in today’s rates for decades. As the deficit widens, the Treasury must issue more of both.

Treasury bills currently account for roughly 15% of all outstanding debt. Treasury notes (2 to 10 years) dominate the stack, accounting for over 40%. Meanwhile, intragovernmental holdings, primarily Social Security trust fund bonds, represent about 18% of total debt. As new deficit spending accelerates, coupon-bearing notes and bonds are expected to absorb a growing share of fresh issuance in FY2027.

Interest Payments Are Breaking Records

The cost of servicing existing debt is now enormous and growing rapidly. Preliminary CBO data show that the Treasury paid nearly $530 billion in interest in just six months. That period spans October 2025 through March 2026. In monthly terms, interest expense exceeds $88 billion. In weekly terms, it surpasses $22 billion.

These figures are striking in context. Interest costs now rival combined federal spending on education and national defense. This is not a projected future scenario. It is the current reality in the U.S. federal budget today. As a result, discretionary investment in infrastructure and public services faces mounting pressure.

Moreover, the numbers are compounding in a difficult way. Each new dollar of deficit spending adds to the debt stock. Each dollar of debt generates additional interest expense. This cycle is extremely hard to break without substantial changes in fiscal policy. Elevated interest rates set by the Federal Reserve have significantly increased this burden over the past two years.

What Budget Experts Are Warning

Maya MacGuineas, president of the Committee for a Responsible Federal Budget, did not hold back. She described $2 trillion annual deficits as “beyond scary.” She noted that markets will only tolerate unsustainable borrowing for a limited time. Therefore, she argued, deficit reduction must be an urgent national priority.

“The risk of a fiscal crisis gets higher as the days pass. We need deficit reduction urgently.”

-Maya MacGuineas, Committee for a Responsible Federal Budget

Frederick Kempe, CEO of the Atlantic Council, reinforced those concerns in a May 7 blog post. He warned that trust in U.S. fiscal management erodes incrementally, not overnight. Higher mismanaged debt leads to higher interest rates on mortgages and business loans. It also shifts resources away from future investment and toward paying for past obligations. He emphasized that accelerating competition with China makes this fiscal challenge even more urgent.

The 3% GDP Target Remains a Distant Goal

A growing bipartisan coalition now supports anchoring the federal deficit to 3% of GDP. Some policymakers want this benchmark written into the US Constitution. However, the current deficit stands at more than double that level. The gap between aspiration and reality has rarely been wider.

MacGuineas put the math plainly. A $2 trillion deficit equals over 6% of GDP. That is roughly twice the proposed 3% target. Reaching that benchmark by 2036 would require approximately $10 trillion in deficit reduction over the next decade. The FRED historical data confirms that current deficit-to-GDP ratios are at elevated levels seen only in wartime or pandemic periods. Neither condition applies to the current environment.

In short, meaningful fiscal reform is essential. Experts broadly agree that further delay only compounds the eventual cost of adjustment.

What This Means for Everyday Americans

These numbers may seem abstract. However, their consequences are deeply practical for households and businesses alike. Higher government borrowing increases competition for available capital in financial markets. This tends to push interest rates upward across the entire economy. Mortgages, car loans, and business credit all become more expensive as a direct result.

Kempe framed this as a strategic national challenge, too. The U.S. needs fiscal flexibility to invest in infrastructure, technology, and national security. A heavily indebted balance sheet limits that flexibility. It consistently diverts resources from tomorrow’s priorities toward paying for yesterday’s decisions. That trade-off is becoming harder to ignore.

Budget analysts argue the window for corrective action is narrowing rapidly. Every month of delay compounds the problem. The $2 trillion deficit threshold is not a ceiling. At the current trajectory, it may soon become the new floor. Policymakers face an increasingly narrow path between fiscal discipline and economic stability.