April 12, 2026 – Henry Hub prices have tumbled 28% this year. Yet Morgan Stanley sees a powerful demand wave building behind the slump.

In Summary

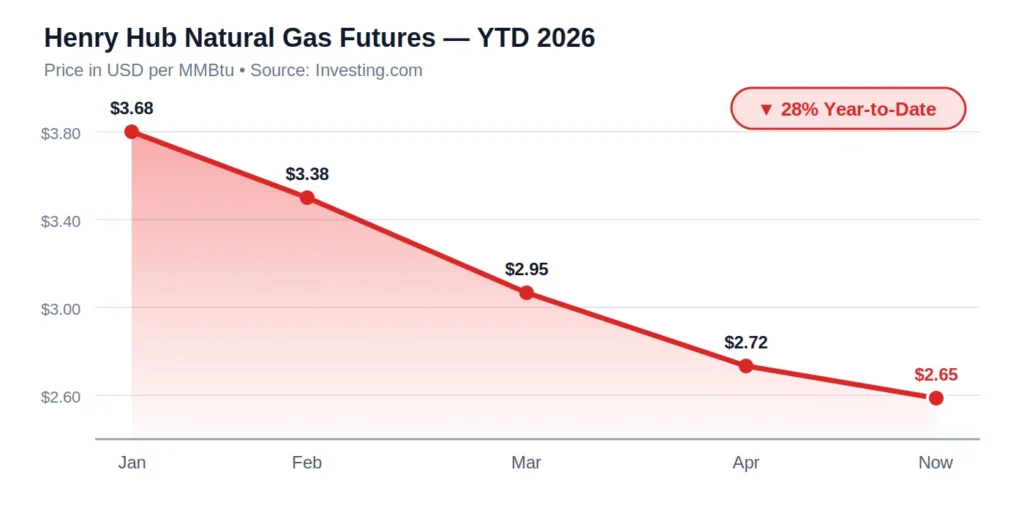

Henry Hub down 28% YTD, with futures near $2.65/MMBtu amid a mild winter exit.

Storage sits 5% above the five-year average, capping near-term price recovery

US gas demand to climb from 113 to 140 bcf/d by 2030, a 24% jump in five years.

LNG exports are the single biggest growth lever, with feedgas demand already rising.

Summer power demand to add ~1 bcf/d year-over-year as western snowpack runs 65% below normal.

Energy CPI jumped 10.9% M/M in April, the largest monthly gain since September 2005.

Morgan Stanley’s verdict: bearish on Q2 2026, structurally bullish through 2030.

US natural gas is caught between two stories. One is bearish and immediate. The other is bullish and structural. Morgan Stanley’s latest note captures both, leaving investors with a deliberately mixed call.

Prices Slide as Winter Disappoints

Henry Hub benchmark prices are down roughly 28% year-to-date. A mild end to winter is the main culprit. Storage inventories now sit about 5% above the five-year average.

That surplus has pinned the front of the curve. Natural gas futures last traded near $2.65/MMBtu, according to Investing.com market data. Morgan Stanley expects range-bound or slightly weaker prices through spring.

Seasonal demand is simply too soft to absorb the overhang. Producers face a tough second quarter as a result.

The Long-Term Picture Looks Very Different

Morgan Stanley’s bullish case rests on one number. US gas demand is projected to climb to roughly 140 billion cubic feet per day (bcf/d) by 2030. Today it sits near 113 bcf/d, in line with EIA Short-Term Energy Outlook consumption baselines.

That is a 24% jump in five years. Two engines drive the forecast.

LNG exports come first. Feedgas demand to liquefaction terminals is already rising. New Gulf Coast capacity is scheduled to come online through 2027. Morgan Stanley calls LNG the single biggest growth lever for US gas.

Power generation comes second. Electricity needs are climbing as data centers and electrification scale. Lower hydro output will compound the effect this summer.

Western US snowpack levels are running about 65% below normal. That forces grid operators to lean harder on gas-fired plants. Morgan Stanley expects roughly 1 bcf/d of additional summer power demand year-over-year.

Energy Markets Already Under Pressure

The note lands amid a volatile broader energy complex. The Iran conflict that erupted in late February has tightened fuel supply.

US CPI data released Friday underscored the strain. The energy index jumped 10.9% month-on-month. That is the largest monthly gain since September 2005, according to Bureau of Labour Statistics figures.

Gasoline alone surged 21.2% on the month. The national average retail price has crossed $4 a gallon for the first time in over three years.

Natural gas has decoupled from this trend so far. Mild weather and ample storage have shielded it. Morgan Stanley warns that decoupling may not last beyond 2026.

What Investors Should Watch

Three signals will decide whether the bearish or bullish case dominates next. The first is storage drawdown rates through summer. A hot June would erode the 5% surplus quickly. The second is LNG feedgas flows. Any acceleration above current levels would validate the 140 bcf/d trajectory.

The third is hydro recovery in the western US. A continued snowpack deficit locks in extra gas burn for power.

For producers, the message is patience. For traders, it is a barbell. Near-term weakness offers tactical shorts. Long-dated contracts offer structural length.

The Bottom Line

Morgan Stanley is not bearish on US natural gas. It is bearish on the next quarter and bullish on the next five years. That distinction matters for portfolio positioning.

Investors who can stomach a soft spring may find the 2027–2030 setup compelling. LNG buildout, power demand, and weather risk all point in one direction over the medium term.

The current $2.65 print may look cheap in hindsight.