June 30, 2026 – Wall Street futures climbed after Washington and Tehran agreed to halt strikes near the Strait of Hormuz and return to the table in Doha.

In Summary

The US and Iran agreed on Sunday to pause strikes near the Strait of Hormuz.

Both sides plan fresh technical talks in Doha on Tuesday, June 30.

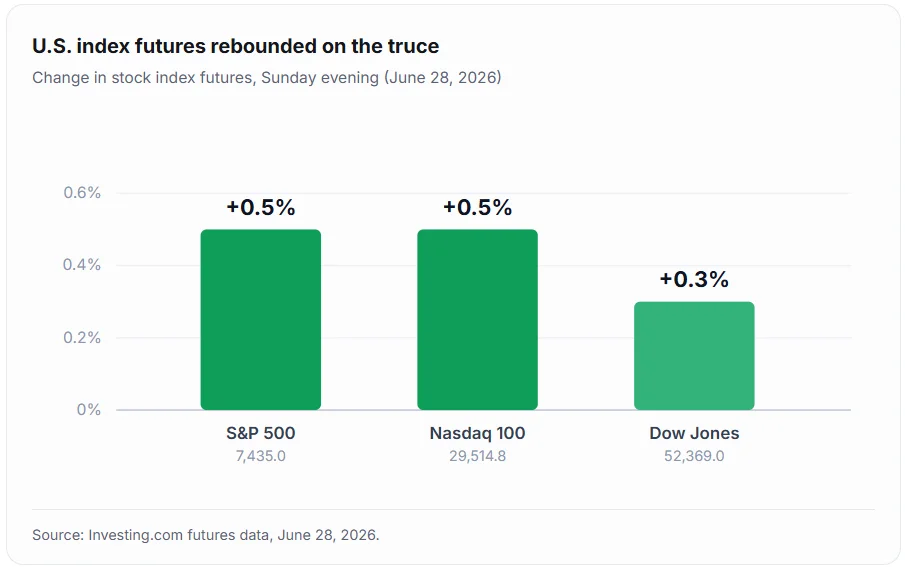

S&P 500 futures rose 0.5%, while Dow and Nasdaq futures also advanced.

Oil gained modestly, with Brent near $72.55 and WTI at $70.17 a barrel.

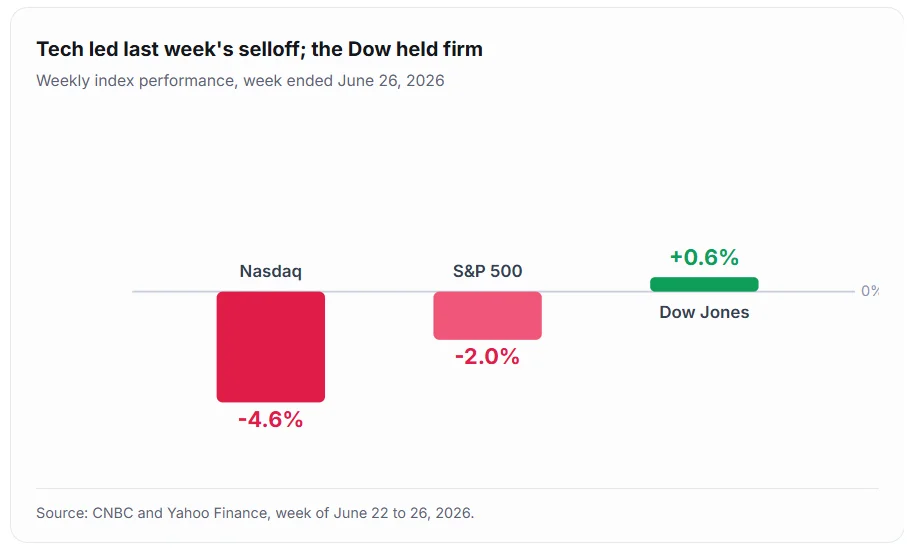

Last week’s tech rout had dragged the Nasdaq down 4.6%.

Wall Street began the week on firmer footing. U.S. stock index futures climbed Sunday evening after Washington and Tehran agreed to pause their attacks. The truce eased fears of a wider disruption near the Strait of Hormuz. As a result, risk appetite returned across global markets. The shift marked a sharp turn from last week’s gloom. Investors had braced for a deeper regional escalation.

Futures climb as tensions cool

S&P 500 futures rose 0.5% to 7,435 points, according to Investing.com. Meanwhile, Nasdaq 100 futures also gained 0.5%, reaching 29,514.75. Dow Jones futures added 0.3% to 52,369 points. Together, these moves signaled renewed confidence after a turbulent weekend. Notably, the gains arrived during thin Sunday trading. Even so, the direction provided an early gauge of sentiment.

The rebound followed an Axios report on the diplomatic breakthrough. According to that report, both sides “decided to stop all the kinetic activity.” Furthermore, the two governments plan to resume technical talks in Doha on Tuesday. Envoy Steve Witkoff and adviser Jared Kushner will reportedly attend. Qatar has hosted several rounds of these sensitive negotiations. Mediators from Pakistan have also supported the wider process. Markets, in turn, treat each session as a catalyst.

Why the Strait of Hormuz matters

The strait carries roughly a fifth of the world’s seaborne oil. Therefore, any blockage threatens the global energy supply and prices. Over the weekend, U.S. forces struck Iranian military and radar sites. In response, Iran fired missiles and drones at bases in Kuwait and Bahrain, Times of Israel reported.

Kuwaiti authorities said they intercepted two incoming ballistic missiles. However, officials reported no American casualties or major damage. President Donald Trump still warned that Washington could “militarily complete the job”. Despite that threat, Sunday’s standdown pulled the fragile peace back from the brink of collapse.

This latest agreement builds on a June 17 memorandum of understanding. That accord reopened the strait and extended a shaky ceasefire. Yet disputes over shipping lanes quickly reignited the violence. Consequently, Tuesday’s session in Qatar now carries heavy weight for traders.

The human stakes also remain considerable. Roughly 1,000 cargo vessels still wait across the wider region. In addition, thousands of mariners remain stranded aboard them. Therefore, a durable truce matters well beyond financial markets. Bahrain and Kuwait both condemned the weekend strikes afterward.

Oil edges higher but stays calm

Oil prices rose, yet the move stayed surprisingly modest. Brent crude climbed 0.78% to $72.55 a barrel. Similarly, West Texas Intermediate gained 1.3% to $70.17, CNN reported. Notably, WTI had settled below $70 on Friday.

That close marked WTI’s weakest level since late February. Indeed, crude now trades far below its wartime peak near $119. Traders clearly expect the ceasefire to hold for now. As a result, energy markets have stayed comparatively composed.

Lower crude has also eased pressure at the pump. Average U.S. gasoline recently held near $3.87 a gallon. That level sits above pre-war norms, but below crisis peaks. Still, another flare-up could quickly reverse the relief.

Tech stocks rebound after a brutal week

Last week punished high-growth technology shares severely. The Nasdaq Composite tumbled 4.6%, its worst week in over a year, CNBC reported. Meanwhile, the S&P 500 fell nearly 2%. By contrast, the Dow gained 0.6%, shielded by lighter tech exposure.

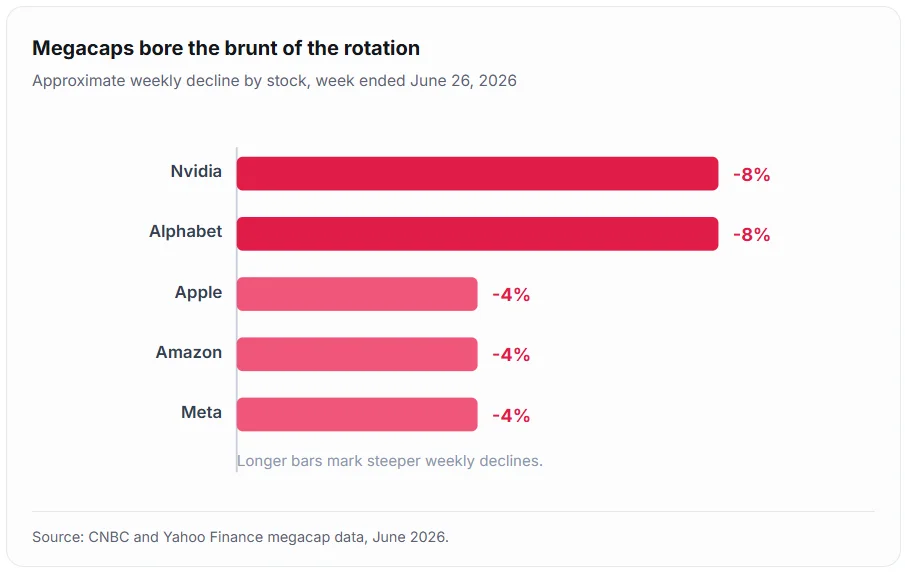

Megacap names drove most of that damage. Nvidia and Alphabet each shed more than 8%. In addition, Apple, Amazon, and Meta each lost over 4%. Investors clearly rotated away from stretched artificial-intelligence valuations. That rotation reflected deep unease over lofty technology multiples. Many of those names had led 2026’s powerful rally. Therefore, even small disappointments triggered outsized selling.

Apple also dampened sentiment with a notable price hike. The company raised prices on several MacBook and iPad models. It blamed surging memory-chip costs tied to booming AI demand. Therefore, hardware affordability has become a fresh market worry.

On Monday, however, the mood brightened considerably. The S&P 500 advanced 1.1% in a choppy session. The Nasdaq Composite jumped roughly 1.8%. Alphabet rose about 4% on its debut as a Dow member. Semiconductors also recovered, as the VanEck Semiconductor ETF climbed 2.5% intraday.

Memory-chip makers added to the sector’s wild swings. Reports suggested Samsung and SK Hynix planned huge new investments. Meanwhile, several U.S. chip names whipsawed through volatile sessions. European markets closed mixed on Monday as well. The Stoxx 600 technology index recovered about 1.2%. By contrast, broad regional indexes ended marginally lower.

What investors should watch next

The trading week ahead offers several fresh catalysts. First, key U.S. labor market data arrives midweek. Second, major firms begin reporting second-quarter results. Additionally, the Independence Day holiday will thin trading volumes on Friday. Each data release could shift Federal Reserve policy expectations. Cooler hiring would strengthen the case for rate cuts.

The conflict itself began in late February 2026. Since then, oil and equities have swung on every headline. This week simply extends that volatile, news-driven pattern. Patience, therefore, may reward disciplined long-term investors.

Geopolitics, though, still dominates overall sentiment. The Doha talks on Tuesday remain the decisive test. Should negotiators clarify approved shipping corridors, equities could extend their gains. Otherwise, renewed strikes might swiftly revive market volatility across asset classes.

Bond markets also reflected the calmer overall tone. The 10-year Treasury yield recently held near 4.38%. Consequently, rate expectations stayed broadly stable into the holiday. The dollar index, meanwhile, hovered around the 101 mark.

Strategists remain split on the near-term path, however. Some argue the earnings recovery still supports equities. Others warn that AI valuations look stretched and vulnerable. Either way, headline risk from Doha keeps positioning defensive. Volatility gauges, meanwhile, eased from last week’s spikes. The Cboe VIX index slipped back toward the high teens.

Analysts urge caution despite the relief rally. Diplomatic progress has repeatedly unraveled within hours before. For now, cautious optimism prevails across Wall Street. Investors will watch Doha closely when markets reopen.