May 16, 2026 – A global risk-off wave struck on Friday, May 15, 2026. South Korean chip stocks led the selloff. Oil surged past $108 on Hormuz fears. Bond yields rose sharply worldwide.

In Summary

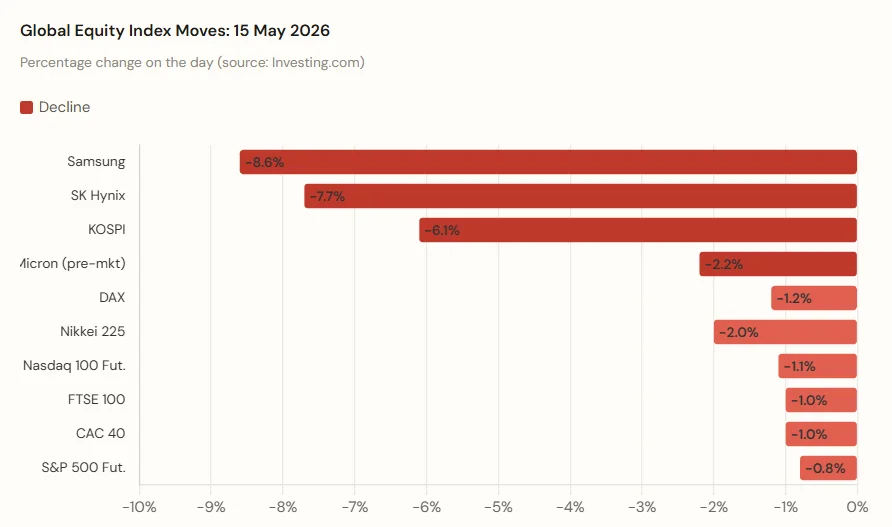

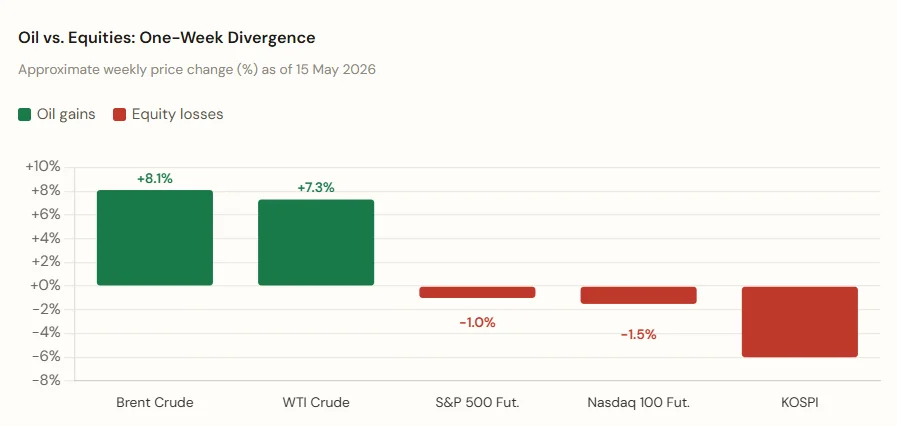

South Korea’s KOSPI fell 6.1%, its sharpest single-day drop in months, as chip stocks collapsed globally.

Brent crude surged to $108.75, and WTI reached $104.42, driven by fears of disruption in the Strait of Hormuz.

US equity futures declined: S&P 500 futures fell 0.8%, and Nasdaq 100 futures dropped 1.1%.

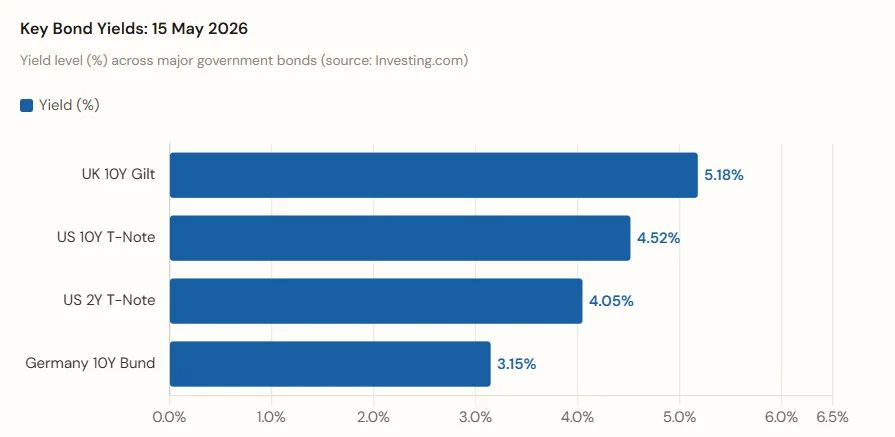

Bond yields spiked globally: the US 10-year yield approached 4.52%, while Japan’s 20-year yield hit its highest level since 1996.

The Trump-Xi summit in Beijing ended with warm words but no concrete trade or geopolitical breakthroughs.

Global financial markets entered full risk-off mode on Friday. The trigger was a sharp selloff in South Korean equities. As a result, weakness spread rapidly to semiconductor stocks across Asia, Europe, and US futures markets. At the same time, rising tensions over the Strait of Hormuz sent oil prices to their highest levels in months.

Asian Chip Stocks Collapse

South Korea’s KOSPI index fell 6.1% on Friday. Earlier in the session, it had briefly broken above the 8,000-point threshold. Profit-taking accelerated rapidly after that peak. Consequently, declines were most severe among memory chip producers.

Samsung Electronics dropped 8.6%, erasing recent gains built during the global tech rally. SK Hynix shed 7.7%. In premarket US trading, memory chip maker Micron Technology fell 2.2%. Meanwhile, mainland Chinese stocks held up better than regional peers.

Oil Surges on Strait of Hormuz Fears

In contrast, oil prices were a standout performer amid the broader selloff. Brent crude futures rose 2.9% to $108.75 per barrel. WTI crude gained 3.2%, reaching $104.42. Both benchmarks were therefore on track for strong weekly gains.

Specifically, the catalyst was President Donald Trump’s comment that the United States did not need the Strait of Hormuz open “at all.” This raised fears of a prolonged disruption to the energy supply. The Strait of Hormuz handles a significant share of global seaborne crude exports. Furthermore, Trump said he was “losing patience” with Iran, stoking supply risk fears even further among traders.

“Markets have lost momentum after President Trump said the US doesn’t need the Strait of Hormuz open at all.”

-Deutsche Bank Strategists, Morning Note, 15 May 2026

PVM Oil Associates analyst Tamas Varga noted that the market focus was gradually shifting toward demand destruction. He added that a sudden escalation could still push prices to new highs. Additionally, Brent oil inventories were described as “horrifically low” in current conditions.

Wall Street Futures Follow Asia Lower

US equity futures tracked Asian markets lower. Specifically, contracts tied to the S&P 500 fell 0.8% in premarket trading. Nasdaq 100 futures dropped 1.1%. These moves came after a period of strong gains in recent weeks.

Similarly, European markets weakened as sentiment soured. Germany’s DAX fell 1.2%. The FTSE 100 and France’s CAC 40 each declined roughly 1%. In addition, UK political uncertainty added further weight to London-listed assets, as Prime Minister Keir Starmer faced renewed internal party pressure.

Vital Knowledge analyst Adam Crisafulli described the Trump-Xi meeting as a non-event for markets. He wrote that none of the summit headlines was “narrative-shifting at all.” Overall, investor sentiment appeared to fade despite the summit’s broadly positive tone.

Bond Yields Spike Worldwide

Government bonds sold off sharply across major markets. Rising yields reflected renewed inflation concerns. In addition, weak demand at recent US Treasury auctions compounded the pressure. Deutsche Bank strategists noted the “lukewarm demand” for recent T-bill auctions. Auction sizes had, moreover, been raised by the Treasury across the prior two weeks.

The US two-year Treasury yield climbed above 4.05%, while the 10-year yield moved toward 4.52%. In the UK, the 10-year gilt yield reached 5.18%. Japan’s 20-year government bond yield surged to its highest level since 1996. Strong producer price data in Japan reinforced expectations of further Bank of Japan rate tightening.

Trump Departs Beijing After Summit

President Trump departed Beijing aboard Air Force One after a two-hour-plus meeting with Chinese President Xi Jinping. The summit generated few concrete policy results. However, the warmer tone between the two leaders offered limited comfort to the market.

Trump said both countries wanted the Iran conflict to end. He also reiterated that Iran should not obtain nuclear weapons. According to Trump, the two sides had reached “fantastic trade deals.” Nevertheless, no details of any agreement were made public.

Chinese state media reported Xi told American business executives that China’s “doors to the outside world will open wider and wider”. Trump, meanwhile, said US-China relations would be “better than ever.” Overall, markets largely dismissed these statements as vague and non-binding.

Looking ahead, investors will focus on US industrial production data for April. The Empire State manufacturing survey for May is also due for release. Both reports could shift rate expectations further if they surprise to the upside.

Broadly speaking, the market narrative has shifted since late April. Geopolitical energy risk has consequently returned as the dominant driver. Until Hormuz tensions ease, oil will likely remain elevated. As a result, pressure on both equity and bond markets is expected to persist.