May 25, 2026 – The US dollar ended the week near flat, balanced between rising rate hike bets and cautious optimism over US-Iran ceasefire diplomacy.

In Summary

The US Dollar Index (DXY) ended the week near 99.24, essentially flat after touching a six-week high.

US-Iran peace talks made tentative progress via Pakistani mediation, but Tehran flagged that big differences remain.

Fed minutes showed a majority of policymakers now consider rate hikes appropriate if energy-driven inflation persists.

University of Michigan consumer sentiment fell to a record low of 44.8 in May, down from 49.8 in April.

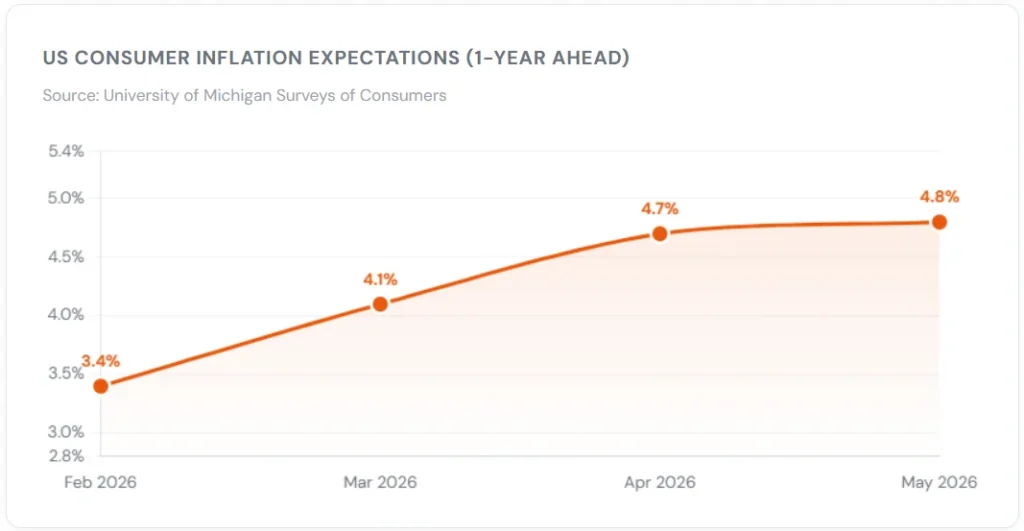

Year-ahead inflation expectations climbed to 4.8%, far above the 3.4% reading seen before the Middle East conflict began.

The US dollar closed a turbulent week nearly unchanged. Investors weighed surging inflation expectations against signs of diplomatic progress in the US-Iran conflict. The currency followed a seesaw pattern throughout the week. It slipped on some days and recovered on others. However, the net result was near zero change.

The Dollar’s Weekly Journey

The US Dollar Index (DXY) started the week on a firm footing. It climbed to a six-week high above 100.00 on Monday. Furthermore, the dollar held above pre-conflict levels for most of the week. However, by Friday, it drifted back to 99.24.

Two forces pulled the dollar in opposite directions. On the one hand, rate-hike bets pushed the greenback higher. On the other side, improving risk appetite weighed on safe-haven demand. Therefore, the net weekly move was negligible.

Rate Hike Expectations Drive Markets

The Federal Reserve’s April meeting minutes revealed a clear shift. A majority of policymakers now view rate hikes as appropriate. This view holds if energy-driven inflation persists. Notably, traders have fully priced in a quarter-point rate hike by year’s end.

Additionally, Kevin Warsh was sworn in as the new Fed chair on Friday. He takes office during a complex moment. President Trump has pushed for rate cuts. However, with inflation running well above target, cuts appear unlikely in the near term. Consequently, the dollar’s appeal as a rate-hiker remains intact.

“The foreign exchange market is relatively calm and being gently bounced around by headlines out of Iran.”

-ING Analysts, Forex Strategy Note, May 2026

Iran Diplomacy: Progress, But Deep Gaps Remain

Diplomatic activity between the US and Iran intensified this week. Pakistan’s Interior Minister Syed Mohsin Naqvi met with Iran’s foreign ministry. His goal was to bridge key divides in the ongoing peace negotiations, according to Reuters.

US Secretary of State Marco Rubio described the discussions as showing “good signs.” However, he cautioned against excessive optimism. Meanwhile, Iran’s foreign ministry spokesperson Esmaeil Baqaei struck a more guarded tone. He stated the two sides had not reached a point where “a deal is close.” Furthermore, he described differences between Washington and Tehran as “deep and significant.”

Consequently, the forex market responded with modest and measured moves. Risk appetite improved cautiously. Nonetheless, traders stayed alert to shifting headline risks from the region.

Consumer Confidence Crashes to Record Low

A striking data point arrived on Friday. The University of Michigan reported its final consumer sentiment reading for May. The headline index fell to 44.8 from 49.8 in April. This marks the lowest level ever recorded in the survey’s history.

Moreover, consumers flagged persistent cost pressures as the main concern. According to survey director Joanne Hsu, 57% of respondents cited high prices as eroding their personal finances. This figure rose from 50% in the prior month. Furthermore, the reading fell just below the previous all-time trough set in June 2022.

Inflation Expectations Keep Climbing

Inflation expectations continued their upward march in May. Consumers’ one-year inflation outlook rose to 4.8%, up from 4.7% in April. This is sharply above the 3.4% reading recorded in February, before the Middle East conflict began.

Long-run expectations also deteriorated. The five-year outlook climbed to 3.9% in May. This compares with the 2.8%-3.2% range observed throughout 2024. Accordingly, Federal Reserve policymakers face increasing pressure to act decisively.

Other Major Currencies at a Glance

Sterling Rebounds Despite Weak Retail Sales

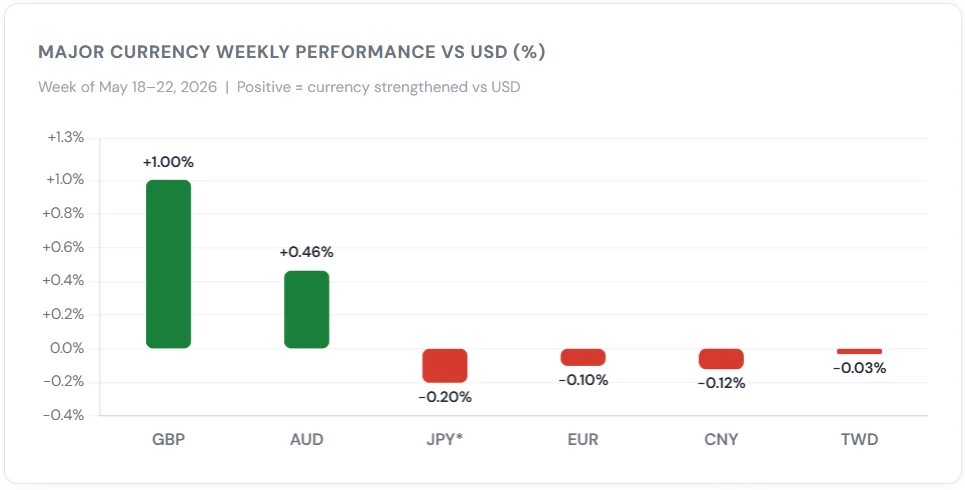

The British pound gained nearly 1% for the week, rising to $1.3440. This bounce came despite a negative surprise from UK retail sales. Retail sales fell 1.3% month-on-month in April, nearly double the expected 0.6% decline. However, the weekly gain reflected a recovery from steep losses the prior week. Those losses followed poor local election results for Prime Minister Keir Starmer’s Labour Party.

Euro Slips; Yen Approaches Key Level

The euro edged down 0.1% to $1.1607, posting a slight weekly loss. Meanwhile, the Japanese yen strengthened for a second consecutive week. The USD/JPY pair posted a 0.2% weekly gain as the yen found support near the critical 160 level. Currency traders believe Japanese authorities intervened in late April to defend the yen around that key mark.

What Traders Are Watching Next

The coming week brings several important catalysts. First, any development in US-Iran ceasefire talks will move currency markets quickly. Second, the Federal Reserve’s next public communications will shape rate expectations. Third, further energy price movements will influence inflation outlooks globally.

Analysts at ING advise closely monitoring the situation in the Strait of Hormuz. Disruptions to oil shipping routes continue to fuel gasoline prices globally. Therefore, any resolution or escalation there will ripple directly into currency markets.

In summary, the dollar’s near-term direction hinges on two factors. Progress in Iran peace talks could reduce safe-haven demand and weaken the USD. Conversely, a hawkish Fed tone could push the DXY back above 100.