July 13, 2026 – Inflation data and the new Fed chair collide on Capitol Hill within 90 minutes. Furthermore, the Bank of Canada sets the next day’s rate.

In Summary

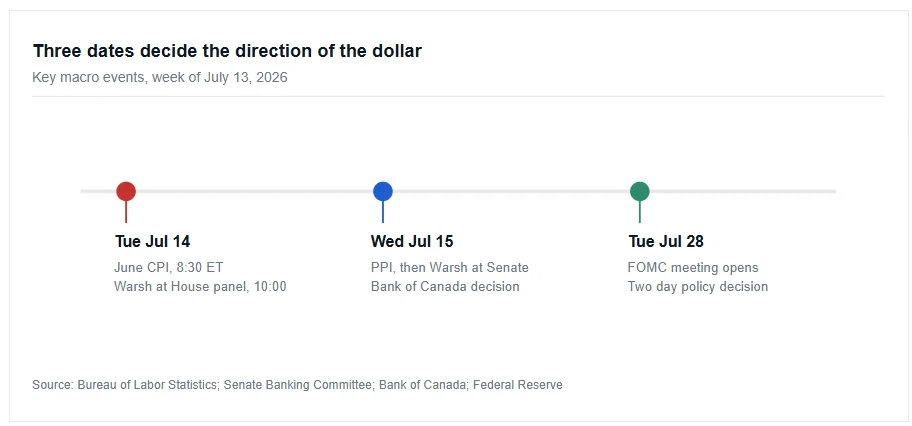

June US CPI lands Tuesday at 8:30 ET, only 90 minutes before Warsh faces the House.

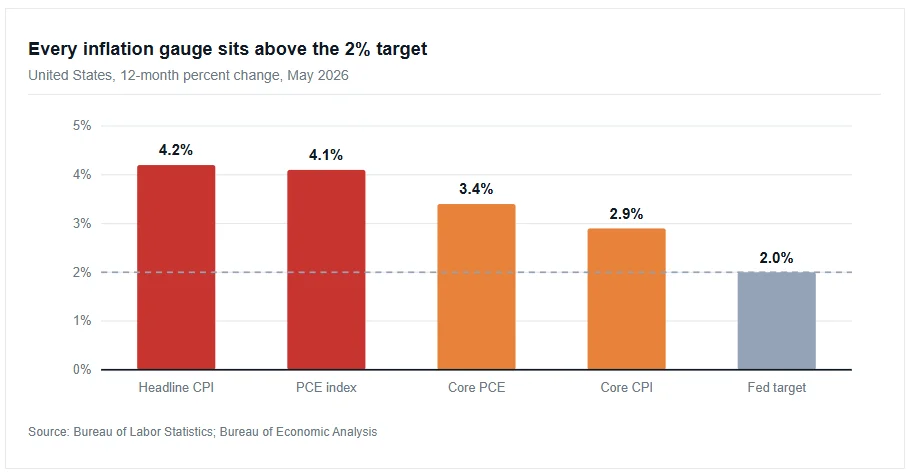

Headline CPI hit 4.2% in May, the fastest annual pace since April 2023.

Core CPI held at 2.9%, so the surge still looks energy-led rather than broad.

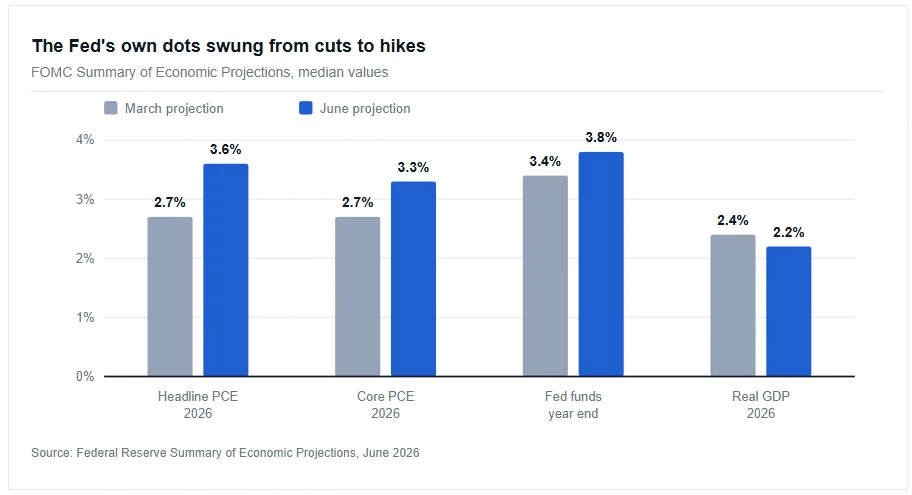

The June dot plot lifted the median 2026 policy rate to 3.8% from 3.4%.

The Bank of Canada rules on Wednesday and looks set to stay at 2.25%.

A hot print plus a hawkish Warsh would lift Treasury yields and the dollar.

Why the US CPI report sets the tone

The US CPI report for June arrives on Tuesday, July 14, at 8:30 a.m. Eastern time. Fed Chair Kevin Warsh then faces the House Financial Services Committee just 90 minutes later. Consequently, a single data print will frame a full day of political theatre.

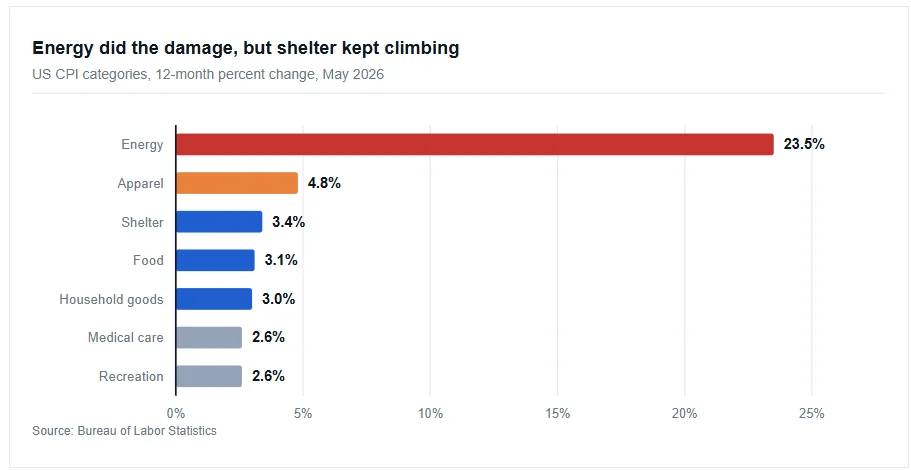

The starting point looks uncomfortable. In May, the all-items index rose 4.2% over 12 months. That marked the fastest annual pace since April 2023, when the gauge hit 4.9%. Moreover, energy prices jumped 23.5% over the same year.

Core inflation tells a calmer story. Excluding food and energy, prices climbed only 2.9% in the year to May. Therefore, the headline surge appears more like an energy shock than a broad price spiral.

Every major gauge still sits above 2%

The Fed watches personal consumption expenditures, not consumer prices. Yet that measure looks worse. In May, the PCE price index rose 4.1% year on year. Core PCE, the number policymakers quote most often, reached 3.4%.

Notably, core PCE has climbed steadily. April printed 3.3%. May added another tenth. Officials therefore cannot dismiss the drift as pure oil noise.

Shelter costs also rose 3.4% over the year. Apparel gained 4.8%, while food added 3.1%. In short, the pressure now spreads well beyond the pump.

The monthly path looks equally telling. April delivered a 0.6% seasonally adjusted gain. May followed with 0.5%. Energy alone drove more than 60% of that May increase.

Annual comparisons flatter the June number, though. Last summer brought soft prints, so the base effect helps. Even so, a downside surprise would not end the inflation debate.

Warsh testifies without a script

Warsh took the chair on May 22. Since then, he has said very little about rates. Indeed, he scrapped forward guidance entirely at his first meeting in June.

The Senate Banking Committee hosts him on Wednesday, July 15, at 10:00 a.m. His House appearance lands a day earlier. Because the June CPI drops first, lawmakers will press him hard on prices.

Still, traders should temper their hopes. Warsh has built a reputation on saying less, not more. Any concrete hint about the July 28 meeting would surprise the market.

Lawmakers will probe far beyond rates. Fed independence tops the list, given persistent White House pressure for cheaper money. In addition, Warsh has launched five internal task forces on Fed reform.

Those groups cover communications, the balance sheet, data quality, inflation analysis and productivity. Congress will want details on each one. Therefore, the hearings may reveal more about the institution than about September.

The Fed’s own forecasts turned hawkish

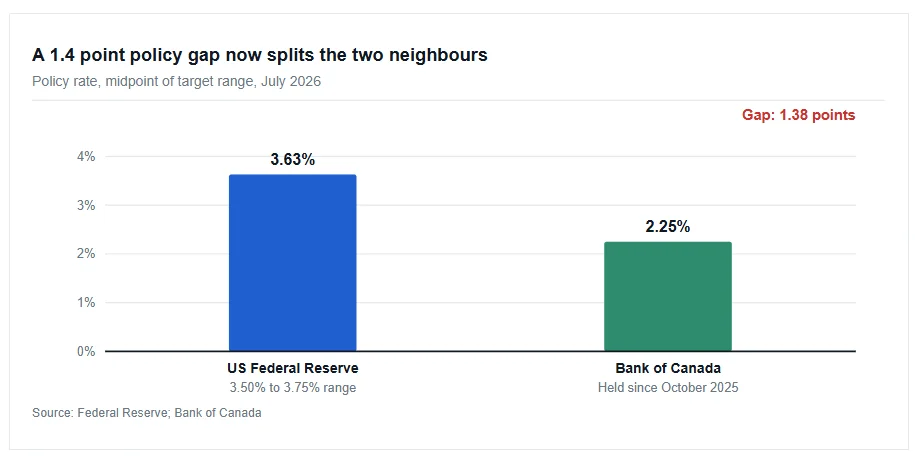

The June meeting delivered a message through numbers instead of words. Policymakers held the target range at 3.50% to 3.75% by a 12-to-0 vote. That marked a fourth straight hold.

However, the projections shifted sharply. The committee lifted its 2026 headline PCE forecast to 3.6% from 2.7%. Core PCE moved to 3.3% from 2.7%. Meanwhile, the median year-end policy rate rose to 3.8% from 3.4%.

In plain terms, the dots now imply a hike rather than a cut. Nine officials pencilled in at least one increase this year. Growth forecasts slipped only slightly, to 2.2%.

As a result, a hot June print could revive bets on September tightening. A soft print would simply buy the committee time.

The Bank of Canada holds a different line

Canada offers a striking contrast. The Bank of Canada has kept its policy rate at 2.25% since October 2025. Its next decision also lands on Wednesday, July 15.

Governor Tiff Macklem faces a genuine dilemma. Energy costs pushed headline inflation up, yet growth stayed sluggish. Therefore, he has held the line through five straight meetings.

The April Monetary Policy Report projected 1.2% growth for 2026. It also pencilled in average CPI inflation of 2.3%. By comparison, the Fed expects far hotter prices.

That gap matters for currency traders. A wide and widening rate differential favours the dollar over the loonie. Furthermore, a fresh Canadian forecast lands alongside the July decision.

China adds a growth test

Beijing offers the other half of the story. China grew 5.0% year on year in the first quarter. On a quarterly basis, output expanded 1.3%.

That result beat most forecasts. Exports carried the load, while consumer demand stayed weak. Meanwhile, the property slump kept dragging on household confidence.

Officials target growth between 4.5% and 5.0% for the full year. Because energy costs rose sharply, second-quarter momentum probably faded. Any sharp slowdown would hurt commodity currencies and risk assets alike.

How markets may trade the print

The dollar sits at the centre of every scenario. A hot CPI reading plus a hawkish Warsh would lift yields and the greenback together. Conversely, a soft print and a cautious chair would deflate both.

Bond traders face the sharpest repricing risk. Short-dated yields track policy expectations most closely. Therefore, the two-year note will react first and hardest.

Risk assets carry more nuance. Equities and digital assets both dislike higher real rates. However, they also rally when fears of inflation fade and growth holds up.

Producer prices follow on Wednesday morning. That release arrives shortly before Warsh reaches the Senate. Consequently, the second hearing may prove livelier than the first.

What the week really tests

Three questions dominate. First, does the energy shock leak into core prices? Second, will Warsh defend Fed independence under political fire? Third, can other central banks resist the tightening pull?

Markets have already positioned for drama. Rate futures lean toward one Fed hike before year-end. However, positioning can flip quickly on a single surprise.

The June CPI print will not settle the debate on its own. Instead, it will tilt the odds. Traders should therefore watch the core reading far more closely than the headline.

Warsh has promised price stability in writing. Now Congress will ask him how and when. That answer, or the lack of one, will move the dollar this week.