May 31, 2026 – Agentic AI from TD’s Layer 6 lab slashed pre-adjudication time by 99.7%. The bank now leads ahead of its CAD 200 million AI value target for fiscal 2026.

In Summary

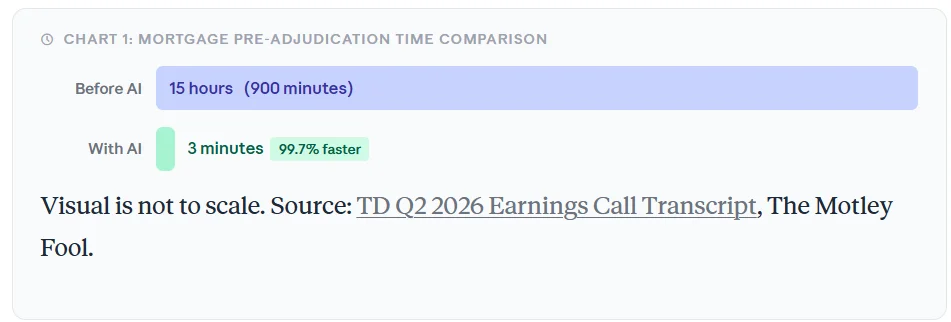

Agentic AI cut mortgage pre-adjudication from 15 hours to just 3 minutes, a 99.7% reduction in processing time.

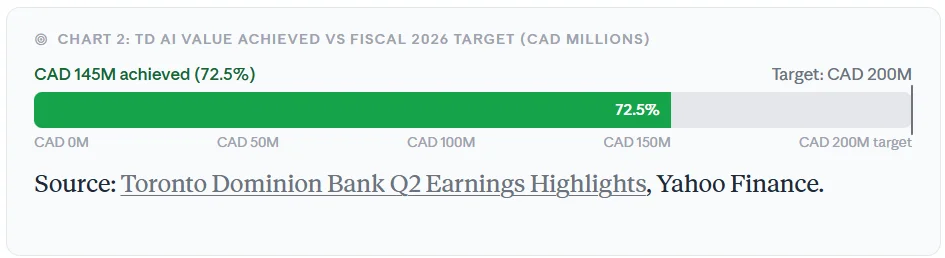

TD generated CAD 145 million in AI-driven value in fiscal 2026, ahead of its full-year CAD 200M target.

AI is projected to deliver more than $500 million in annualized savings for TD Bank.

Over 40,000 employees use Microsoft Copilot tools daily; top engineers achieved a 29% increase in throughput.

Canada’s largest banks are moving AI from the boardroom into core operations. TD Bank’s Q2 2026 earnings release provided the clearest proof yet. Agentic AI slashed mortgage pre-adjudication time from 15 hours to three minutes. TD confirmed this milestone on May 28, during its quarterly earnings call.

CEO Raymond Chun described the result as a genuine transformation. “AI will transform our operations, make our colleagues more efficient, and our products better,” he said. Furthermore, Chun confirmed TD is “tracking well ahead of pace” on all AI goals set at Investor Day.

What is agentic AI?

Agentic AI goes far beyond basic automation tools. It makes independent decisions and executes multi-step workflows without requiring human input at each stage. TD built its mortgage tool through Layer 6, its dedicated in-house AI research center. Moreover, the bank used the same technology to become Canada’s first home and auto insurer to launch a client-facing generative AI virtual assistant.

The system reads borrower documents and validates data in real time. It then delivers a pre-adjudication decision in under three minutes. Previously, this same process required approximately 15 hours of manual review. Additionally, the tool autonomously adapts to complex borrower profiles without additional human oversight.

AI value targets and progress

According to TD’s Q2 earnings highlights, the bank generated CAD 145 million in AI-driven value in fiscal 2026. That figure is already ahead of its CAD 200 million full-year target. Additionally, TD targets between $2 billion and $2.5 billion in annualized structural cost savings over the medium term.

AI is expected to contribute more than $500 million of those savings. A similar amount is also projected in revenue uplift. Therefore, AI is not just cutting costs for TD. It is actively generating new income streams at scale.

Across the bank, over 40,000 employees use Microsoft Copilot tools every day. Meanwhile, more than 7,000 engineers use AI throughout their software development workflows. Among the most active engineers, productivity climbed by 29%.

Record Q2 financials support the AI case

The AI milestones arrived alongside strong financial results. Adjusted EPS rose 21% year over year to CAD 2.38, beating average analyst estimates of CAD 2.26. Return on equity climbed to 14.4%. Canadian personal and commercial banking delivered record Q2 revenue, profit, and net earnings.

Net income for that segment reached CAD 1.93 billion, up 15% from a year earlier. Adjusted revenue rose 6% to $16.6 billion. Furthermore, TD raised its quarterly dividend by CAD 0.04 to CAD 1.12 per share, signalling management’s confidence in future earnings.

The bank targets 6% to 8% EPS growth for fiscal 2026. Management said TD is “ahead of the vast majority” of all Investor Day metrics. Shares fell about 0.5% in early trading on earnings day, reflecting broader market caution.

Cards emerge as a growth engine

In the United States, proprietary credit card balances rose 18% year over year. Strong customer acquisition drove that growth. New card account acquisition climbed 32% year over year, reflecting TD’s aggressive push into U.S. retail banking.

Additionally, TD completed the integration of Nordstrom card clients onto its servicing platform. CFO Kelvin Tran called this “an important strategic milestone.” He also noted it could help TD pursue new card partnerships while lowering long-term servicing costs across the franchise.

Middle-market lending balances increased 13% in U.S. banking. Average deposits rose 3% year over year across the bank. Together, these results confirm that TD’s U.S. franchise is gathering real momentum.

The broader banking shift

TD is not the only institution racing toward AI-driven lending. The ABA Banking Journal reports that 38% of mortgage lenders used AI in 2024, up from just 15% in 2023. Industry data also confirms AI can reduce per-loan operational costs by 30% to 50%. These numbers underscore how quickly the industry is shifting.

However, not all institutions are at the same stage. Large banks with dedicated AI labs, such as TD’s Layer 6, have clear structural advantages over smaller lenders. Therefore, the gap between AI-ready banks and legacy institutions is widening rapidly. Laggards risk permanent competitive disadvantage.

Challenges remain

Not all risks have disappeared for TD. The bank continues to invest in anti-money laundering (AML) remediation and governance systems. These AML-related costs are expected to decline later in fiscal 2026. In addition, analysts pressed management on whether AI could push long-term profitability above historical peaks.

Chun acknowledged the uncertainty but remained confident. He pointed to ongoing AI opportunities across credit, contact centers, fraud, and frontline productivity. Moreover, the bank’s CET1 capital ratio held firm at a healthy 14.3%, reflecting a strong balance sheet.

What this means for borrowers and banks

For borrowers, faster approvals mean less waiting, more certainty, and a smoother experience. For banks, the financial logic is now compelling. TD’s results confirm AI can deliver measurable returns at enterprise scale, not just in isolated pilots.

AI is no longer a banking experiment. Banks like TD are embedding it into every core process. Furthermore, the competitive pressure on slower-moving lenders will only intensify as agentic tools become standard infrastructure across the industry.