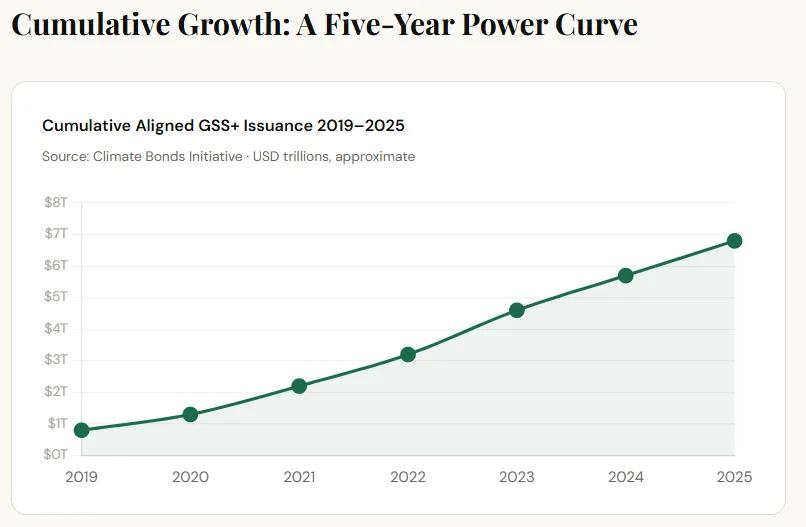

May 27, 2026 – Cumulative aligned issuance hit USD 6.8 trillion by the end of 2025. Green bonds lead the charge. New issuers are joining from 109 countries.

In Summary

Cumulative aligned sustainable debt reached USD 6.8 trillion by the end of 2025.

Annual issuance exceeded USD 1 trillion for the third consecutive year.

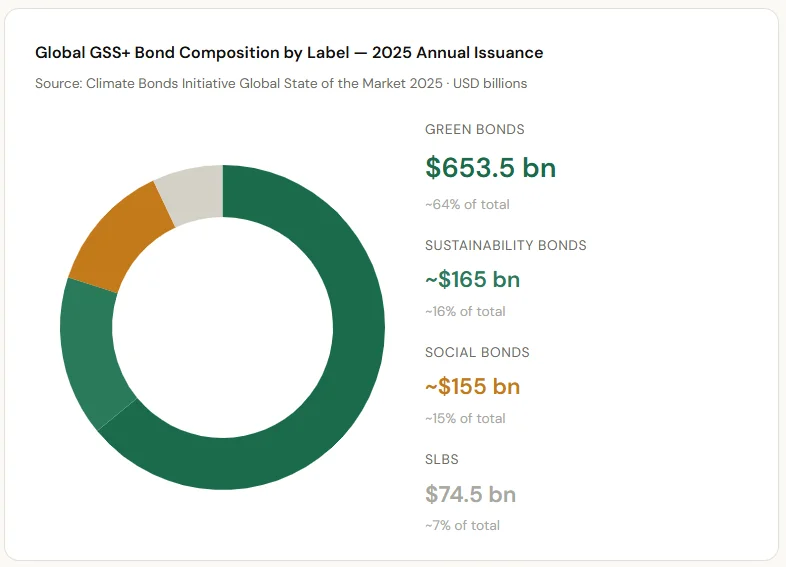

Green bonds account for 64% of all aligned GSS+ issuance in 2025.

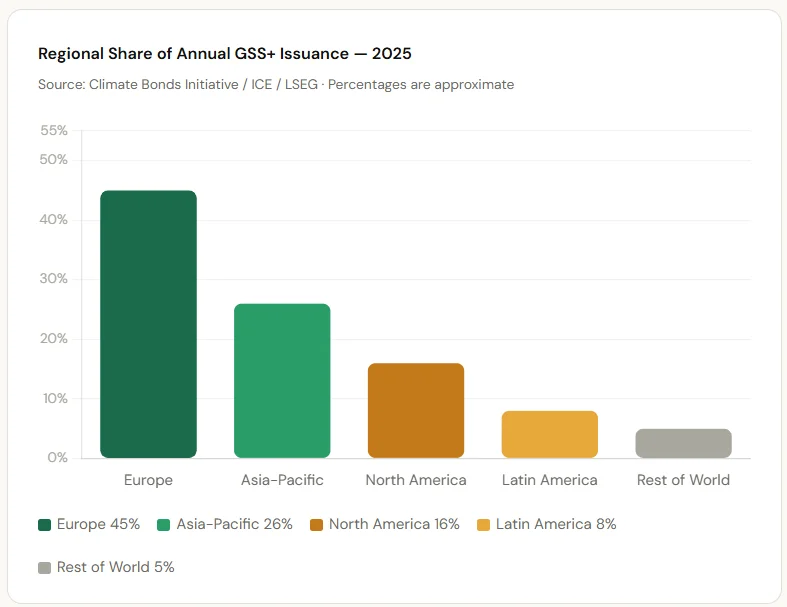

Europe leads globally, with 45% of annual volume and USD 3 trillion in cumulative value.

Over 400 new issuers joined the market in 2025, from 109 countries worldwide.

The global sustainable debt market is growing rapidly. According to the Climate Bonds Initiative (CBI), cumulative aligned issuance reached USD 6.8 trillion by December 2025. This is the headline finding from CBI’s 15th annual Global State of the Market report. The report was published in March 2026. Furthermore, annual issuance crossed USD 1 trillion for the third consecutive year. More than 400 new issuers entered the market in 2025. Together, these figures confirm sustainable debt as a mainstream asset class. The market now spans 109 countries and continues to attract participants from every region.

What Is Sustainable Debt?

Sustainable debt covers several types of financial instruments. These include green bonds, social bonds, sustainability bonds, and sustainability-linked bonds (SLBs). Collectively, they are called GSS+ bonds. Each instrument targets a specific environmental or social objective. Investors use them to fund clean energy, sustainable transport, water infrastructure, and more. The OECD notes that the International Capital Market Association published its Green Bond Principles in 2014. Additionally, the Climate Bonds Standard, first published in 2012, certifies bonds linked to climate projects. These standards increase investor confidence. Furthermore, they provide a framework for transparency and post-issuance reporting.

Green Bonds Lead the Pack

Green bonds remain the dominant force in sustainable finance. They account for 64% of all aligned GSS+ issuance in 2025. In 2025 alone, green bond issuance totalled USD 653.5 billion. This is the second-highest annual volume ever recorded. However, other segments also showed strength. Sustainability bonds added USD 217.3 billion in annual issuance. Social bonds reached USD 141.2 billion for the year. Moreover, sustainability-linked bonds (SLBs) showed renewed momentum. Their aligned issuance rose 46% year-on-year, reaching USD 14 billion. Therefore, market growth is broad-based across all GSS+ categories. Green bonds also surpassed USD 4 trillion in cumulative issuance during 2025.

Europe Maintains Global Leadership

Europe remains the world’s leading source of sustainable debt. According to LSEG, Europe retained the top position for green bond issuance in 2025. The region accounts for 45% of the total aligned annual GSS+ volume. Furthermore, Europe’s cumulative sustainable debt has crossed USD 3 trillion. Asia-Pacific ranked second globally, with USD 305.6 billion issued in 2025. China’s issuance rose more than 30% year-on-year, driven by domestic green finance policies. Meanwhile, North America is approaching USD 1 trillion in cumulative issuance. However, the United States saw a 17% decline in annual issuance for 2025. Consequently, the global sustainable finance landscape is shifting eastward.

New Issuers Expand the Market

The sustainable debt market continues to attract new participants. More than 400 new issuers entered the market in 2025. Today, sustainable debt instruments originate from 109 countries worldwide. This wide participation signals growing global recognition of the asset class. Furthermore, it reflects stronger regulatory frameworks and rising investor demand. The OECD reports that the outstanding amount of corporate sustainable bonds reached USD 2.4 trillion in 2024. Official sector issuers added another USD 2.2 trillion over the same period. Together, public and private actors are scaling up their sustainable debt programmes. Additionally, corporate non-financial sector bonds reached USD 1.3 trillion outstanding by the end of 2024.

Adaptation Finance Gains Ground

Climate adaptation finance is becoming a new market priority. The CBI identifies resilience finance as a rapidly emerging sector. Climate-related disasters are rising in frequency and economic cost. As a result, the demand for adaptation-focused investment is growing. The Tokyo Metropolitan Government issued the world’s first certified Climate Bonds resilience bond in 2025. This landmark deal demonstrates strong investor appetite for adaptation instruments. Additionally, it signals that capital markets are beginning to price climate risk more seriously. Therefore, resilience finance could be the next major growth driver for the sustainable debt market.

“The continued trillion-dollar scale of sustainable debt issuance demonstrates that capital markets are increasingly aligned with climate and sustainability goals.”

-Clodagh Muldoon, Head of Research, Climate Bonds Initiative

What Comes Next?

The global bond market exceeds USD 100 trillion in total outstanding value. Sustainable debt still represents a small share of this total. However, the trajectory points toward faster expansion in the coming years. Environmental Finance forecasts global new sustainable bond issuance near USD 950 billion in 2026. Moreover, the Asia-Pacific is expected to hit a new regional issuance record. Regulatory drivers support this outlook. Japan’s GX transition policy and China’s updated green taxonomy are two key examples. LSEG also reports that total outstanding green bonds crossed USD 3 trillion for the first time in Q3 2025. Furthermore, clear taxonomies and standards will be critical for scaling climate finance. Sustainable debt is maturing from a niche segment into a core pillar of global capital markets.