April 14, 2026 – The American Bankers Association challenges a White House study. It says policymakers dangerously underestimate the deposit-flight risk of yield-bearing stablecoins at scale.

In Summary

The ABA disputes a White House / CEA study on stablecoin yield restrictions.

The CEA found banning yield would lift lending by only 0.02%, the ABA calls this misleading.

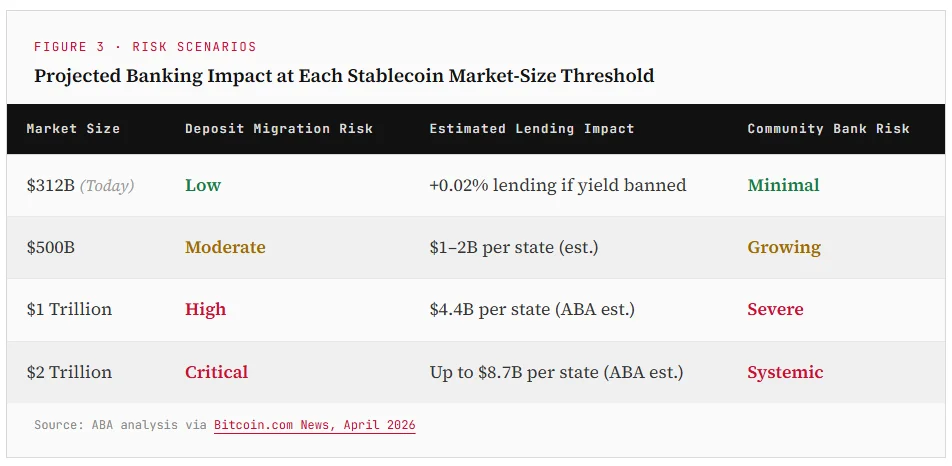

The contested risk is a stablecoin market scaling from $312B to $2 trillion, not today’s baseline.

ABA estimates lending could fall by $4.4B–$8.7B in a single state as stablecoins scale.

Community banks face the greatest exposure due to reliance on stable local deposit bases.

The ABA argues yield on payment stablecoins should be prohibited as a prudent safeguard.

The Policy Clash at the Center of U.S. Crypto Law

A sharp dispute emerged on April 13, 2026. The American Bankers Association (ABA) challenged a White House economic analysis. The Council of Economic Advisers (CEA) argued that banning stablecoin yields would have little effect on lending activity. The ABA says the CEA is asking the wrong question.

ABA chief economist Sayee Srinavasan and VP Yikai Wang authored the rebuttal. Their concern is not a yield ban in isolation. Their concern is what happens when yield-bearing stablecoins scale rapidly toward $1–$2 trillion.

Why It Matters: Yield-bearing stablecoins offer returns similar to bank savings accounts. If they scale quickly, deposits could migrate out of banks. This would shrink the funds available for consumer and business loans.

What the White House Study Found

The CEA paper found that prohibiting stablecoin yield would increase bank lending by only 0.02%. That is a negligible change. It falls within normal quarterly fluctuations in the banking system.

The study framed yield restrictions as having a limited short-term impact. Policymakers read this as reassurance. The ABA says that comfort is dangerously misplaced.

Policymakers should not take comfort from a study showing that prohibiting stablecoin yield might have a small, near-term effect on aggregate lending.

— ABA Chief Economist Sayee Srinavasan & VP Yikai Wang

The Real Risk: Scale, Not Today’s Market

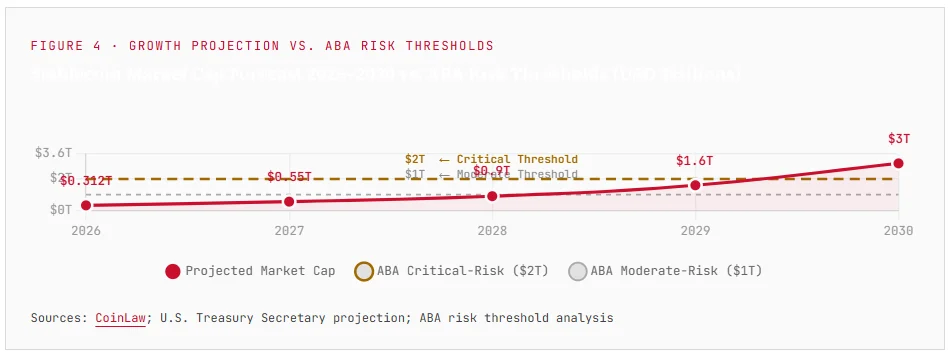

The ABA’s core argument centers on market size. The stablecoin market currently stands at roughly $312 billion, with transaction volumes expected to hit $33 trillion in 2025, a 72% year-on-year surge. That is large. But it is not yet the threat level the ABA fears.

The real danger arrives near $1–$2 trillion. At that scale, yield becomes a primary driver of deposit migration. Community bank customers would have compelling reasons to shift funds. Banks would lose the cheap deposit base they rely on to fund lending.

The ABA estimates that credit effects could include a $4.4B–$8.7B reduction in lending in a single state, using Iowa as an example. The nationwide impact would be far larger.

Community Banks Bear the Brunt

This risk is not evenly distributed. Large national banks have diverse funding sources. Community banks do not. They depend heavily on local deposits to fund mortgages and small-business loans.

Deposit outflows would hit them hardest. Rising funding costs follow. Then comes reduced lending capacity. The knock-on effects ripple through regional economies.

The European Central Bank echoed similar warnings. An ECB paper in early 2026 warned that stablecoin growth could weaken monetary policy transmission. It could also hamper lenders by shifting deposits away from banks. The concern is global in scope.

The ABA’s Proposed Safeguard

The ABA is not calling for a blanket ban on stablecoins. Its position is targeted. It argues that payment stablecoins should not pay yield. Yield is what transforms a payment tool into a deposit competitor.

The authors call a yield prohibition a “prudent safeguard.” It would allow stablecoins to develop as genuine payment innovations. Without it, they become risky substitutes for federally insured bank deposits.

Market Context: The stablecoin market now processes more than $33 trillion in annual transactions, up 72% year-over-year. U.S. Treasury Secretary Scott Bessent projects the market could reach $3 trillion by 2030. At that scale, the ABA’s concerns become much harder to dismiss.

What This Means for Crypto Regulation

The stablecoin debate sits at the heart of U.S. financial legislation in 2026. Congress is weighing the GENIUS Act and STABLE Act, two competing stablecoin bills. The yield question is a central fault line in both.

The ABA wants the final legislation to prohibit yield on payment stablecoins. Crypto industry groups want yield permitted. The White House study appeared to support a lighter-touch approach. The ABA rebuttal significantly complicates that political calculation.

For investors and market watchers, the stakes are clear. If yield-bearing stablecoins are permitted at scale, bank deposit models face structural disruption. If restricted, a major driver of DeFi growth disappears. Either outcome reshapes the $312 billion market.