June 01, 2026 – Elon Musk publicly rejected claims that SpaceX cut its IPO target. The company’s financials make a compelling case for a $2 trillion valuation.

In Summary

Musk posted “False” on X to reject a Bloomberg-sourced valuation report.

Bloomberg sources alleged the IPO target dropped from $2T to $1.8 trillion.

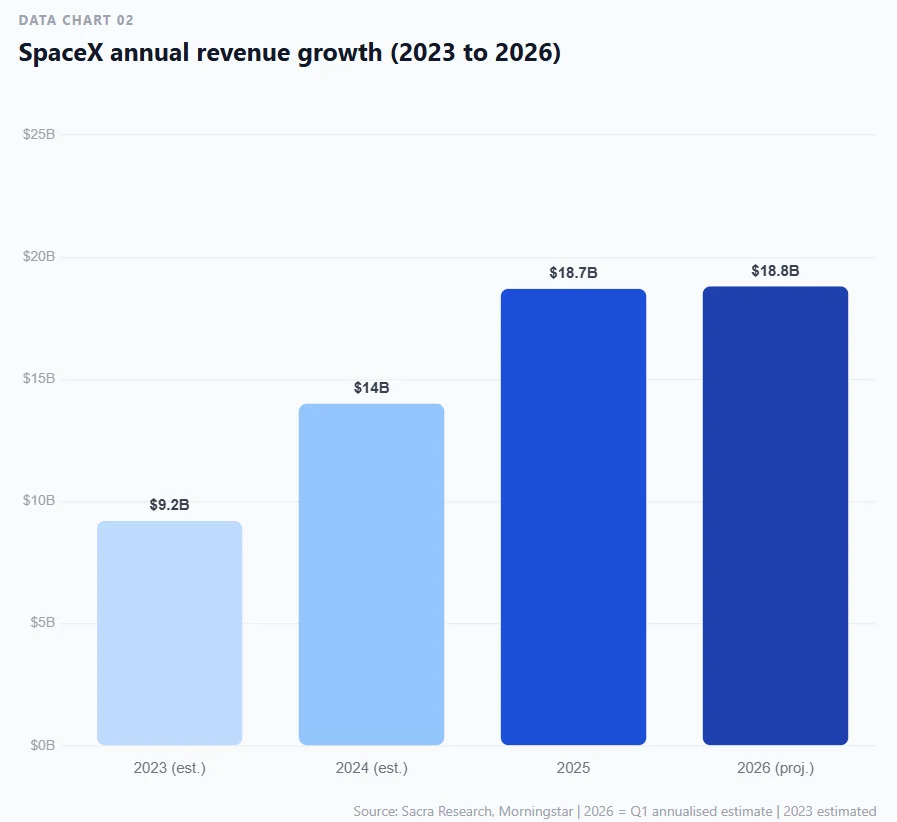

SpaceX earned $18.674 billion in revenue during 2025, up 33% year over year.

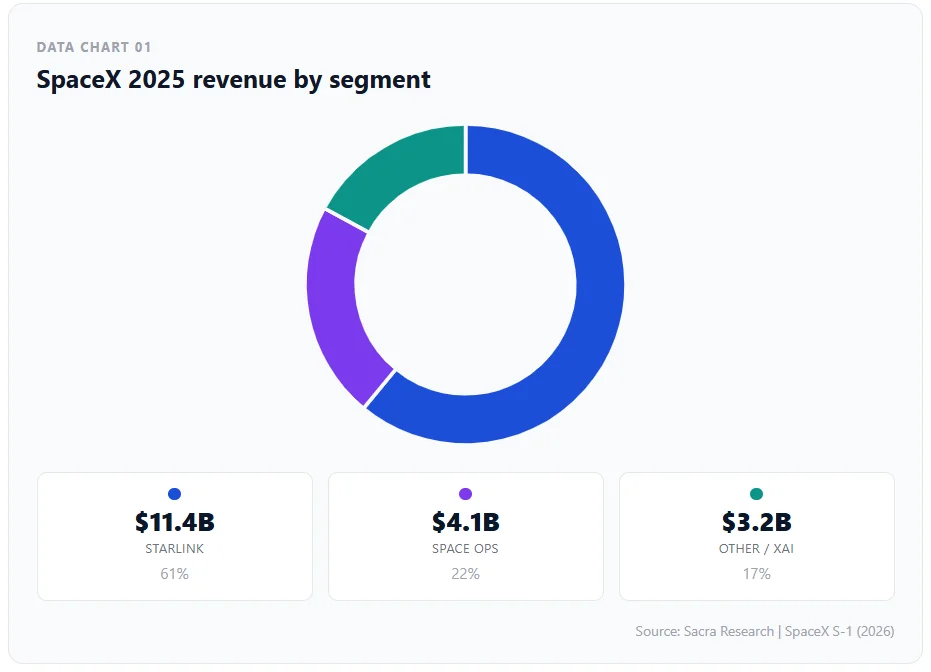

Starlink contributed $11.4 billion, or 61%, of total revenue with $4.4B in operating profit.

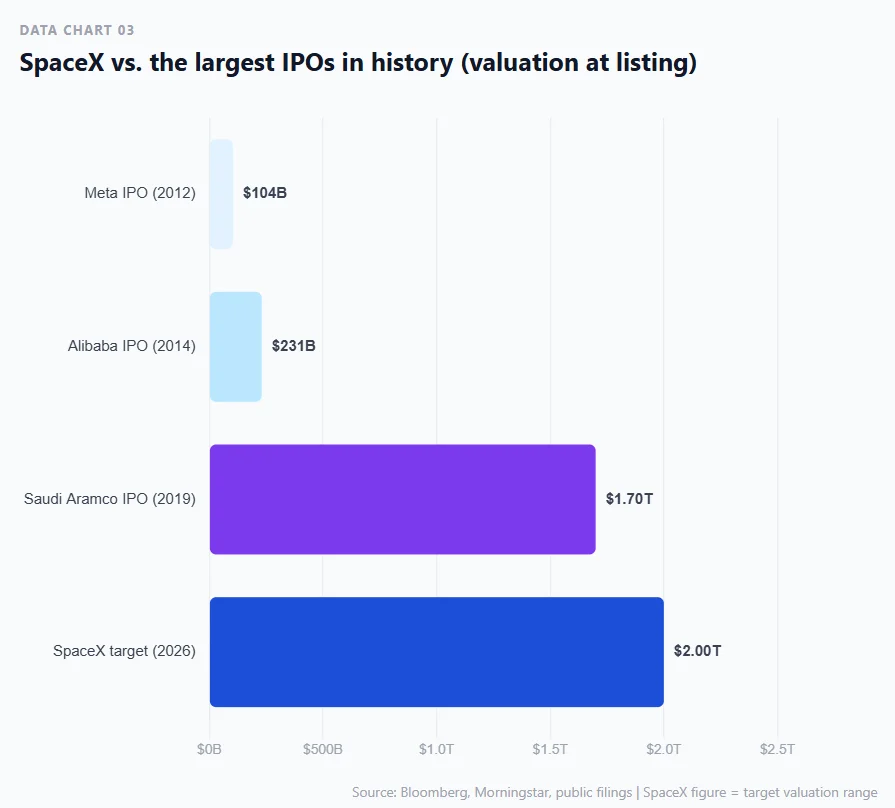

SpaceX plans to raise $75 billion in what could be the largest IPO in history.

Elon Musk does not ignore media reports that mischaracterize his companies. On May 29, 2026, he posted a single word on X: “False.” The post he rejected came from ZeroHedge. That post cited Bloomberg sources claiming SpaceX had cut its IPO valuation target. Specifically, those sources alleged the target dropped from above $2 trillion to at least $1.8 trillion. The rebuttal was swift, direct, and unambiguous.

What the reports claimed

Bloomberg’s anonymous sources alleged a meaningful shift in SpaceX’s IPO ambitions. They suggested the company scale back its valuation target before a potential June listing. Furthermore, these claims surfaced as anticipation of SpaceX’s S-1 regulatory filing intensified. SpaceX filed that document confidentially on April 1, 2026. However, neither SpaceX nor Bloomberg has since offered official clarification on the disputed figures.

SpaceX’s financial reality

The underlying numbers tell a compelling growth story. SpaceX reported $18.674 billion in consolidated revenue for full-year 2025. That figure represents a 33% increase over the prior year. Furthermore, Starlink carried the heavy load. The satellite internet unit contributed $11.4 billion, or 61% of total sales. Additionally, Starlink generated $4.4 billion in operating profit that year.

In Q1 2026, SpaceX posted $4.694 billion in quarterly revenue. That marks a 15% year-over-year gain. Moreover, Starlink generated more than $3.2 billion in Q1 2026 alone. However, SpaceX also recorded a net loss of $4.28 billion in that same quarter. Starship development costs and xAI integration drove those elevated losses.

The IPO timeline

SpaceX confidentially filed its S-1 with the SEC on April 1, 2026. The public offering could launch as early as June 2026. Additionally, reports indicate the company plans to raise approximately $75 billion. Twenty-one investment banks are reportedly lined up to support the deal. Therefore, this listing could surpass Saudi Aramco’s 2019 record as the largest IPO in market history.

SpaceX completed an all-stock merger with xAI in February 2026. This move created a third operating segment alongside Space and Starlink. Furthermore, SpaceX signed a compute deal with Anthropic worth $1.25 billion per month. These additions significantly expand SpaceX’s revenue potential beyond rocket launches.

Military contracts strengthen the case

SpaceX is not only a commercial rocket company. The U.S. Space Force awarded SpaceX a $2.29 billion contract in May 2026. This deal covers the construction of the Space Data Network Backbone. Furthermore, the Space Force awarded SpaceX $178.5 million in April for missile tracking satellites. These government contracts add meaningful revenue predictability. Additionally, deep military ties reinforce the national security narrative around SpaceX’s valuation.

Why the denial matters

Musk rarely engages directly with financial media. Therefore, his public rebuttal carries real weight with institutional investors. By calling the Bloomberg story false, he signals strong confidence in SpaceX’s valuation standing. Analysts at Morningstar note that Starlink’s adjusted EBITDA grew 86% between 2024 and 2025. Additionally, Starlink’s EBITDA margin reached 63%, far above the 20% average for traditional satellite operators.

Risks beneath the surface

Nevertheless, risks remain significant. SpaceX’s Q1 2026 net loss reached $4.28 billion. That is nearly eight times the year-ago quarterly figure. Consequently, capital consumption remains a valid concern for investors. Starship development continues to demand billions annually. Additionally, xAI integration adds new short-term operating costs that weigh on near-term profitability.

Investors should weigh these costs against Starlink’s strong cash generation. The satellite unit effectively subsidises SpaceX’s broader ambitions in space and artificial intelligence.

The road ahead

Regulatory filings and road show disclosures will provide clarity in the coming weeks. The S-1’s detailed financials will directly address the valuation debate. Moreover, speculation about a Tesla-SpaceX merger adds another layer of complexity. Wedbush analyst Dan Ives puts the probability of a merger at 80% to 90%, with a 2027 target. However, prediction markets assign only 33% odds to a deal closing before May 2027.

Musk’s one-word denial did not end the conversation. Instead, it focused attention on forthcoming S-1 disclosures. Those filings will provide the definitive answer on SpaceX’s market value. Meanwhile, the company continues to grow revenue, expand its satellite network, and secure major government contracts.