May 28, 2026 – Cramer flags three growth drivers and one structural concern ahead of the June 12 Nasdaq debut under ticker SPCX.

In Summary

SpaceX targets a $1.75T to $2T valuation, listing on Nasdaq under ticker SPCX on June 12, 2026.

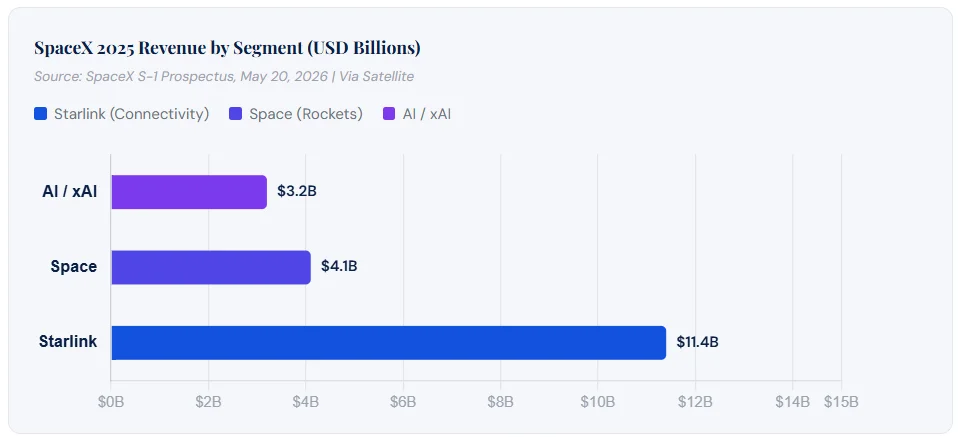

Starlink drives 61% of revenue and holds a 63% adjusted EBITDA margin. It is the only profitable division.

Cramer’s three catalysts: Starship commercial payloads, Starlink subscriber growth, and the Cursor deal.

A small public float could push opening-day valuation to $5 trillion or beyond, Cramer warns.

SpaceX posted a $4.9B net loss in 2025. The AI segment alone lost $6.36B in operating income.

SpaceX filed its S-1 prospectus on May 20, 2026, targeting a Nasdaq debut on June 12. The company plans to trade under the ticker SPCX. Its filing disclosed $18.7 billion in total revenue for 2025. However, SpaceX also posted a net loss of $4.9 billion that year. CNBC’s Jim Cramer reviewed the offering on Mad Money on May 26. He identified three near-term catalysts for investors to track. Yet he also raised one significant structural concern. The offering targets a raise of up to $75 billion. That would make it the largest IPO in capital markets history.

The $2 Trillion Question

SpaceX targets a valuation between $1.75 trillion and $2 trillion. At that price, shares would trade at roughly 100 times trailing revenue. Cramer described that multiple as “crazy expensive.” Therefore, investors must weigh near-term growth triggers carefully. The prospectus also shows steep losses in the AI segment. Specifically, xAI posted an operating loss of $6.36 billion in 2025. Nonetheless, Starlink remains the company’s primary financial engine.

For context, 200 S&P 500 companies reported more revenue than SpaceX last year. Tesla’s sales were five times higher. The valuation is therefore a bet on future growth curves, not current earnings. However, that bet depends on three specific catalysts Cramer outlined on air.

Three Near-Term Catalysts

Catalyst 1: Starship Commercial Payloads

SpaceX completed its 12th Starship test flight on May 23, 2026. The test carried no passengers or commercial cargo. However, the prospectus targets commercial payload delivery to begin in H2 2026. SpaceX has already invested over $15 billion in Starship development. Cramer believes a successful payload launch would sharply lift investor confidence. Additionally, Starship aims to significantly reduce launch costs per kilogram. A lower cost base would benefit both government and commercial customers.

Catalyst 2: Starlink Growth Engine

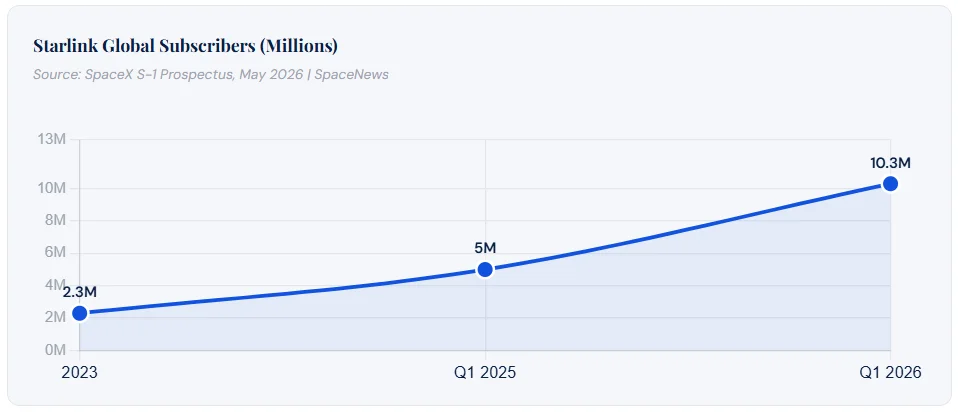

Starlink is the only profitable SpaceX division. In 2025, it generated $11.4 billion in revenue. That figure grew 49.8% year-over-year. Furthermore, Starlink’s adjusted EBITDA margin reached 63%. That is a remarkable level for a capital-intensive infrastructure business. Subscribers doubled from 5.0 million to 10.3 million in just one year. However, average revenue per user fell from $99 to $66 per month. This decline reflects expansion into lower-income international markets. SpaceX operates over 9,600 satellites across 164 countries. Q1 2026 Starlink revenue alone reached $3.26 billion, with operating income of $1.19 billion.

Catalyst 3: The Cursor Partnership

SpaceX signed a strategic deal with AI coding startup Cursor. The partnership combines Cursor’s tools with SpaceX’s computing infrastructure. Together, they aim to improve AI products such as Grok. Additionally, SpaceX holds an option to acquire Cursor for $60 billion later in 2026. Cramer argued this would strengthen xAI’s position among leading AI labs. Therefore, enterprise revenue growth could accelerate meaningfully. The deal also signals SpaceX’s broader ambitions in the AI infrastructure market.

Cramer’s Reservation: Float Risk

Despite the catalysts, Cramer urges caution. His core concern focuses on the IPO float structure. A small public float could push valuation far above fundamentals. Cramer warned the stock could briefly reach a $5 trillion valuation. For context, Nvidia currently trades at roughly $5.4 trillion. Such a spike would reflect speculation, not underlying earnings. Moreover, SpaceX’s IPO could drain capital from the broader market. Investors may sell existing holdings to fund new purchases. The Cerebras Systems IPO offered a recent warning: shares surged nearly 70% on debut day.

Additionally, lock-up expiry periods could trigger sharp selling. Standard agreements prevent insiders from selling for 90 to 180 days post-IPO. Once these expire, a significant supply could hit the market. Smart investors should plan for this scenario well in advance.

“At $2 trillion, SpaceX would trade at roughly 100 times trailing revenue. That is the central tension every investor must weigh before participating.”

Reading the Prospectus

SpaceX’s 2025 revenue breakdown reveals a clear structural story. Starlink drove 61% of total revenue. The Space segment contributed 22% but posted an operating loss. The AI segment added 17%, yet lost $6.36 billion in operating income. Total long-term debt stood at $29.1 billion as of March 2026. Elon Musk will retain approximately 42% of shares after the offering.

Morningstar analysts note that SpaceX’s capital intensity exceeds that of even manufacturers like Tesla and Rivian. Furthermore, SpaceX has $25.45 billion in contractual cloud-capacity commitments for 2026 and 2027. xAI’s research and development costs surged over 300% in 2025. GPU depreciation and cloud infrastructure drove that increase. These figures explain why Starlink’s profits are critical to funding the rest of the business.

The Bottom Line

SpaceX represents a rare, high-stakes market opportunity. However, its fundamentals do not yet justify a $2 trillion price tag. Cramer advises investors to track catalysts, not just market hype. Starship payloads, Starlink subscriber growth, and the Cursor deal are the key signals to monitor closely. Above all, watch how the share float affects opening-day pricing. Discipline should drive investment decisions here. The first 90 days after the IPO will be critical. Smart investors will track lock-up expirations and quarterly Starlink reports with care.