July 11, 2026 – Sony Bank has moved closer to a regulated U.S. stablecoin business. The bigger story is about trust, reserves, and digital dollar rails.

In Summary

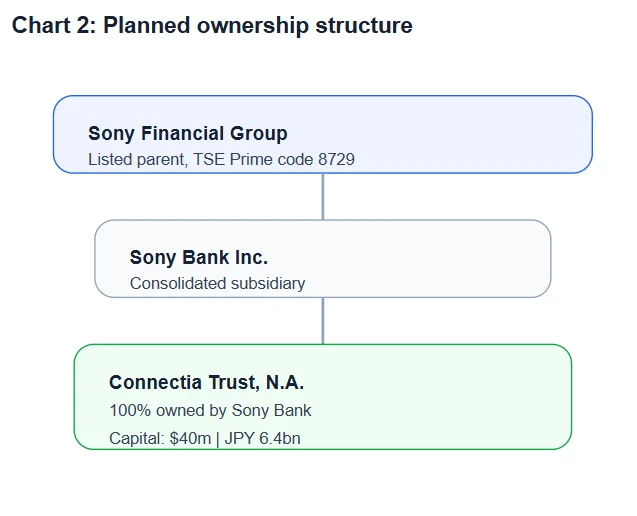

Sony Bank plans a US national trust bank called Connectia Trust.

The entity will support US dollar stablecoin issuance and management.

Initial capital is set at $40 million, or about JPY 6.4 billion.

No stablecoin activity can begin before final regulatory approvals.

The move adds a major consumer brand to regulated digital dollar infrastructure.

Sony Bank’s stablecoin plans gained fresh momentum after its parent approved a U.S. trust subsidiary. The planned unit, Connectia Trust, National Association, will sit inside Sony Bank’s financial group structure. It will prepare businesses tied to U.S. dollar stablecoin issuance and management. However, investors should read the signal carefully. This is not a live coin launch. The company filing states that no business activity may begin until all authorizations are received.

Why this approval matters

The approval matters because it links a global consumer finance group to regulated digital-dollar infrastructure. Stablecoins have already become the settlement layer for much of crypto trading. Now, major financial brands want a safer route into that market. A national trust bank can give Sony Bank a clearer federal supervisory channel. That matters in a sector where reserve quality and redemption speed drive trust. The move also follows a broader trend in digital asset charters. A federal charter statement said conditional approvals remain subject to strict OCC conditions. It also said approved entrants would join about 60 national trust banks. Therefore, Sony Bank is entering a crowded but increasingly formal path.

What Connectia Trust will do

Sony Bank plans to capitalize Connectia Trust with $40 million. The filing converts that amount to about JPY 6.4 billion. Sony Bank will own 100% of the trust subsidiary. The planned business description covers trust company activities and related operations. In plain terms, the unit will build the legal and operational base for stablecoin activity. Still, the filing does not confirm token design, launch timing, or customer distribution. That missing detail is important for investors and users. A closed-loop payment token would have different economics from an open-market stablecoin.

The market is large, but concentrated

The stablecoin market is big enough to attract banks, networks, and consumer platforms. A current stablecoin market dashboard shows a total market value of $311.804 billion. It also shows USDT dominance at 59.04% and USDC at $73.272 billion. That concentration creates both opportunity and difficulty for new issuers. New entrants can target trust, compliance, and better user experience. However, they must overcome liquidity advantages held by existing market leaders. That is why Sony Bank’s brand may help, but it will not be enough on its own.

Why banks are moving now

Stablecoins are shifting from trading tools to payment infrastructure. That shift changes who wants to issue and manage them. Earlier issuers won through liquidity, exchange access, and fast distribution. Banks compete through supervision, custody, treasury operations, and compliance discipline. Sony Bank’s proposal fits that second model. It does not need to copy every crypto-native feature. Instead, it can compete on redemption quality and user confidence. That approach may suit corporate users and platform businesses. These users often care more about control than novelty. They also need predictable accounting, reporting, and operational support. For that reason, the trust bank model could become a bridge. It can connect digital asset rails with conventional finance controls. The downside is speed. A regulated issuer may move more slowly than offshore rivals. It must build policies, systems, audits, and vendor controls before scaling. However, that slower path can help in institutional payments. Counterparties usually prefer clear legal rights and transparent settlement rules. Stablecoin adoption will depend on these practical details.

The regulation angle

U.S. rules now put reserves and disclosures at the center of stablecoin policy. The stablecoin law fact sheet states that issuers must maintain 100% liquid reserves. It also points to monthly public disclosure of reserve composition. That framework favors issuers that can operate like regulated financial institutions. For Sony Bank, this may turn compliance into a competitive feature. Yet compliance can also raise costs before revenue scales. That trade-off is central to the investment case.

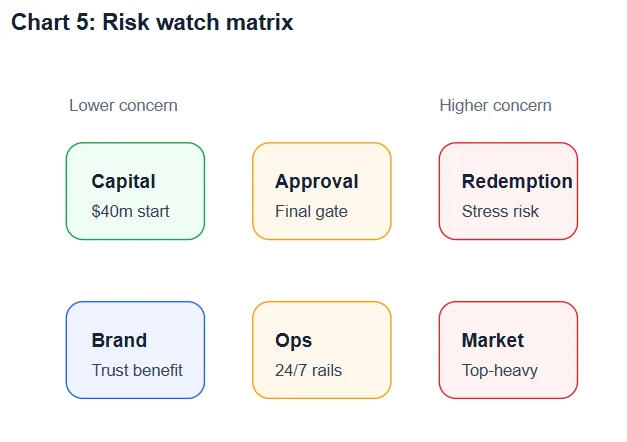

Risks to watch

The first risk is approval risk. Conditional approval does not equal final approval. The second risk is reserve liquidity. A stablecoin must meet redemptions under pressure. The third risk is adoption. Users need a reason to move from incumbent coins. There is also operational risk from always-on blockchain settlement. An analysis by an international central bank forum says money-like stablecoins need to be redeemable for cash at all times. It also says low-risk reserves and credible backstops become vital at scale.

What comes next

The next milestone is final authorization for Connectia Trust. After that, investors should watch token design, reserve disclosures, and redemption mechanics. They should also watch whether Sony links the token to payments, content, or wider digital services. The strategic value sits in payment utility, not in the license alone. For now, Sony Bank’s stablecoin plans mark a regulated step into digital dollars. The step is meaningful. Yet the real test starts when users can redeem at par. For readers, the lesson is simple. Stablecoin credibility now depends on governance, not only on blockchain speed.