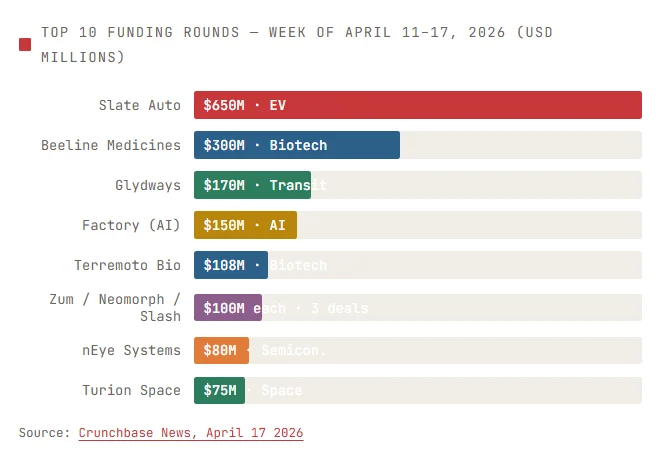

April 18, 2026 – Slate Auto’s $650M Series C tops the biggest deals week ending April 17, 2026. Transportation and life sciences command over 80% of capital deployed.

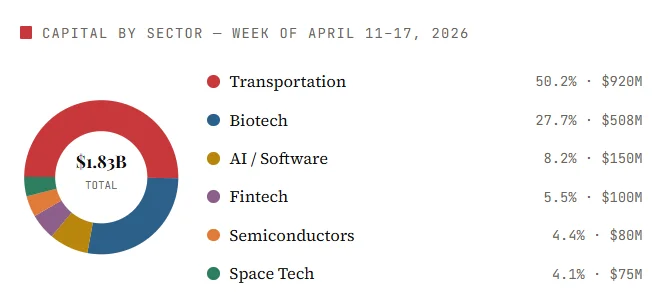

Venture capital had a striking week. U.S. startups raised $1.83 billion across ten major rounds between April 11–17, 2026. According to Crunchbase News, transportation and biotech dominated the leaderboard. Together, these two sectors claimed over $1.4 billion, roughly 78% of total capital.

The deals signal continued investor conviction in physical-world disruption. Electric vehicles, autonomous transit, and precision medicine all drew large checks. AI software engineering also made a notable appearance.

Slate Auto Leads With a $650M EV Bet

The week’s standout deal belongs to Slate Auto, a Troy, Michigan-based EV startup. It closed a $650 million Series C round led by TWG Global. That is the largest single EV funding round seen this quarter.

Slate Auto’s pitch is unconventional. It builds lower-cost electric pickup trucks that convert into SUVs. The Jeff Bezos-backed company plans to deliver its first vehicles to customers later in 2026. At $650M raised, the company now holds a substantial runway for manufacturing scale-up.

“Lower-cost EVs targeting mainstream buyers represent the next frontier of electric vehicle adoption.”

Biotech Claims the Second Spot Twice Over

Beeline Medicines emerged from stealth with a $300 million Series A. Led by Bain Capital, Beeline targets autoimmune and inflammatory diseases. It licensed five programs directly from Bristol Myers Squibb. This is a significant stealth-to-public debut for the Boston-based company.

Further down the list, Terremoto Biosciences raised $108 million in Series C funding. The South San Francisco firm develops small-molecule drugs for cancer and rare diseases. Investors include RA Capital Management and Deep Track Capital. Neomorph, another cancer therapeutics developer, secured $100 million in Series B funding. Deerfield led the round.

Three biotech deals totaling $508 million reflect continued investor appetite for precision medicine. This is a notable pattern: biotech has ranked in the top two sectors for weekly VC totals in six of the last ten weeks.

AI Software Engineering Hits $1.5B Valuation

Factory, a San Francisco startup, secured $150 million in Series C funding. Khosla Ventures led the round. The deal valued the 3-year-old company at $1.5 billion, crossing the unicorn threshold. Factory builds tools that automate software engineering workflows. Its growth signals investor confidence in autonomous coding tools as an enterprise category.

Autonomous Transit Gets Its Moment

Glydways raised $170 million in Series C funding. The San Francisco company makes personal autonomous pods for dedicated transit lanes. Suzuki Motor, ACS Group, and Khosla Ventures co-led the round. Glydways is launching pilots in three cities this year. The investment reflects growing municipal interest in affordable autonomous public transit solutions.

Fintech, Semicon & Space Round Out the Week

Slash, a business banking platform, raised $100 million in Series C funding. It reported over $250 million in annualized revenue in 2025. Its $1.4 billion valuation makes it another new unicorn. Semiconductor startup nEye raised $80 million for optical data center interconnects. Space firm Turion Space closed over $75 million in Series B funding for its orbital intelligence platform.

What the Data Tells Us

This week’s capital flow reinforces two macro trends. First, physical-world infrastructure EVs, transit, and space are attracting large Series C and B rounds. Second, biotech’s precision medicine wave continues to draw billion-dollar commitments at early stages.

Three new unicorns emerged this week alone: Factory ($1.5B), Slash ($1.4B), and Slate Auto (valuation undisclosed but implied). That density of $1B+ outcomes in a single week reflects a maturing, if selective, VC market in early 2026.

One throughline: Khosla Ventures co-led three of the week’s top deals Factory, Glydways, and Slash. That concentration signals high conviction in AI autonomy and physical infrastructure as converging themes.