July 14, 2026 – Britain has named the 54 firms that will move its wholesale markets on chain. The widely quoted 33-billion-pound figure, though, is not a pile of debt. It is a forecast.

In Summary

Ripple sits on the new 54-firm UK taskforce, next to BlackRock, J.P. Morgan and Goldman Sachs.

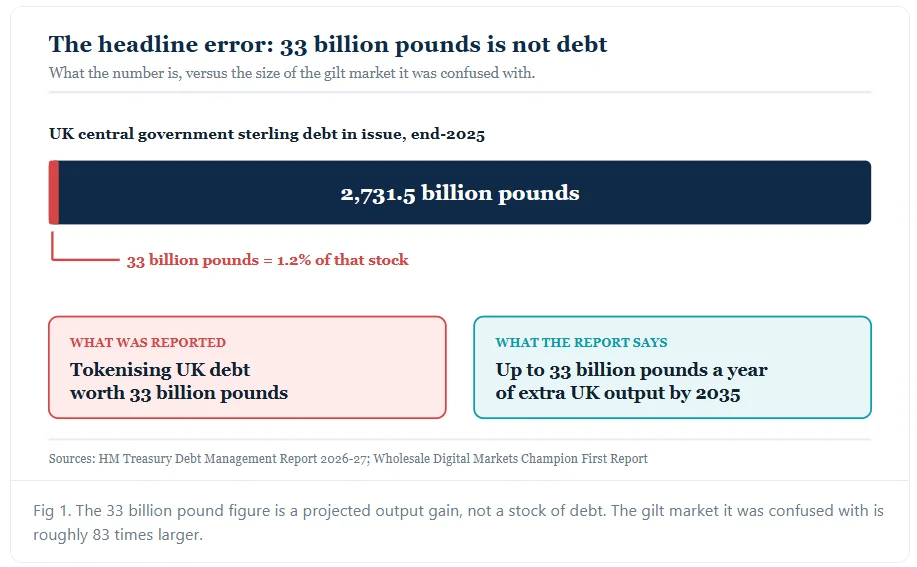

The 33 billion pound figure is a forecast of extra annual output by 2035, not a quantity of debt.

Real UK sterling debt in issue stood at 2,731.5 billion pounds at the end of 2025.

HM Treasury must deliver the DIGIT digital gilt pilot by the first quarter of 2027.

All 16 firms inside the Digital Securities Sandbox remain at the test stage, not live business.

The UK tokenisation taskforce now has Ripple on it. So do BlackRock, J.P. Morgan and Goldman Sachs. Chris Woolard CBE sent his first report to the Chancellor on 13 July. And the City of London Corporation named all 54 member firms on the same day. The list forms the core of Britain’s plan for digital wholesale markets.

What the 33 billion pound figure really means

But one number in the coverage needs a second look. Some outlets framed the story as a plan to tokenise UK debt worth 33 billion pounds. That reading gets the source wrong. The figure shows yearly economic output, not a pile of debt.

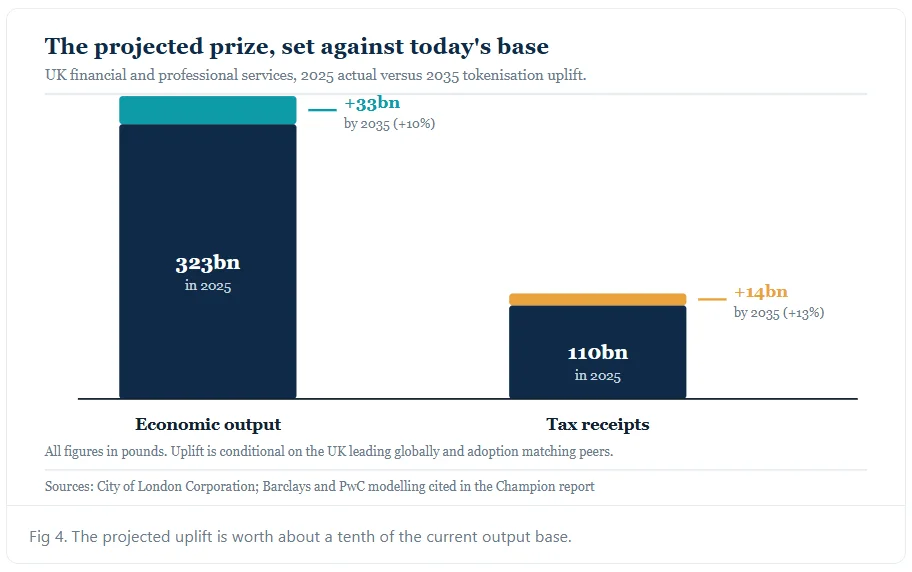

Barclays and PwC did the modelling behind it. Their work says the shift could add up to 33 billion pounds a year to UK output by 2035. And it puts the tax gain at 14 billion pounds a year. Yet both numbers come with strings. Britain must lead the field, the market must grow, and local uptake must match its peers.

UK finance and professional services made 323 billion pounds of output in 2025. They paid 110 billion pounds in tax. So the projected gain is worth about a tenth of that base.

And the real gilt market dwarfs the headline number. HM Treasury logs 2,731.5 billion pounds of central government sterling debt in issue at the end of 2025. That makes 33 billion pounds, worth just 1.2% of the stock. The two figures measure very different things.

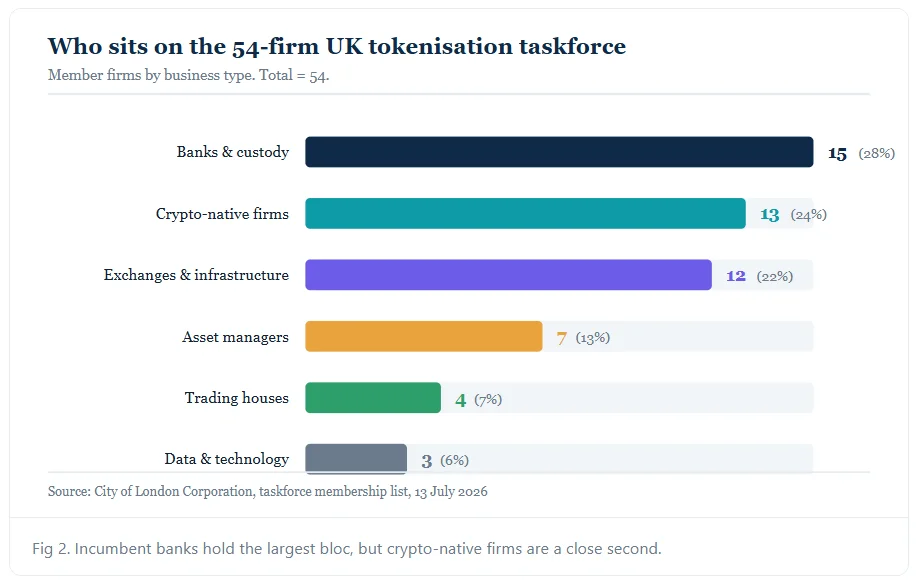

Who sits on the UK tokenisation task force

Banks and custody firms hold the most seats, with 15. Crypto native firms come next, with 13. Exchanges and market plumbing take 12 places. Asset managers hold seven, and trading houses hold four. Data and tech vendors fill the last three.

That mix shows the trade at the heart of the plan. Big banks bring cash, balance sheets and licences. Crypto firms bring the rails, the tools and the speed. Neither side can build this market alone.

Why Ripple earned a seat

Ripple’s place looks less odd on a closer read. The firm bought the prime broker Hidden Road for $ 1.25 billion in 2025. As a result, Ripple Prime now holds an FCA investment firm licence. It also holds an FCA crypto registration.

The report also notes that Santander UK runs cross-border payments on Ripple’s chain. So Ripple arrives with live UK licences, not just a pitch deck. BlackRock brings much the same profile. It signed on as a UK crypto firm in April 2025.

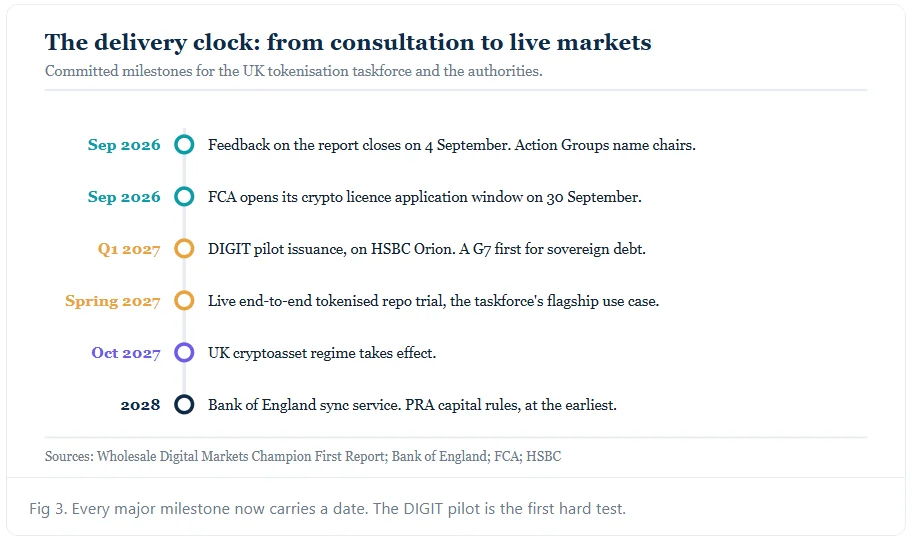

DIGIT and the 2027 deadlines

Feedback on the report closes on 4 September 2026. The nine Action Groups then name their chairs and members that month. HM Treasury must deliver the DIGIT pilot by the first quarter of 2027.

HSBC won the platform mandate for that sale in February 2026. Its Orion system has already processed more than $ 3.5 billion in digital bonds. If DIGIT lands, Britain becomes the first G7 state to sell sovereign debt on a chain.

The taskforce also wants a live tokenised repo trial by spring 2027. Repo sits at the heart of the plan for good reason. It funds the market, moves collateral and touches every big player. Prove the repo, and the rest tends to follow.

The UK has a once-in-a-generation opportunity to lead “a digital Big Bang in financial services”

-Chris Hayward, Policy Chairman, City of London Corporation

The payment leg problem

Tokenised bonds still need a cash leg. The Bank of England opened omnibus accounts back in 2022. It now plans to launch a sync service in 2028. Eighteen firms are testing that link in the Bank’s Sync Lab. Meanwhile, high street banks continue to build the Great British Tokenised Deposit. Without a working cash leg, the whole plan stalls.

The evidence base for efficiency gains

Backers point to hard numbers. A 2025 ISSA survey found an 11.6% drop in collateral buffers. It also logged a 13.4% fall in failed trades. And 94% of the firms polled expect better collateral flow.

Boston Consulting Group projects a 15%-30% revenue lift for asset managers. A 1%-2% increase in collateral use could lift banks’ return on equity by up to 4%. Still, these are forecasts, not results.

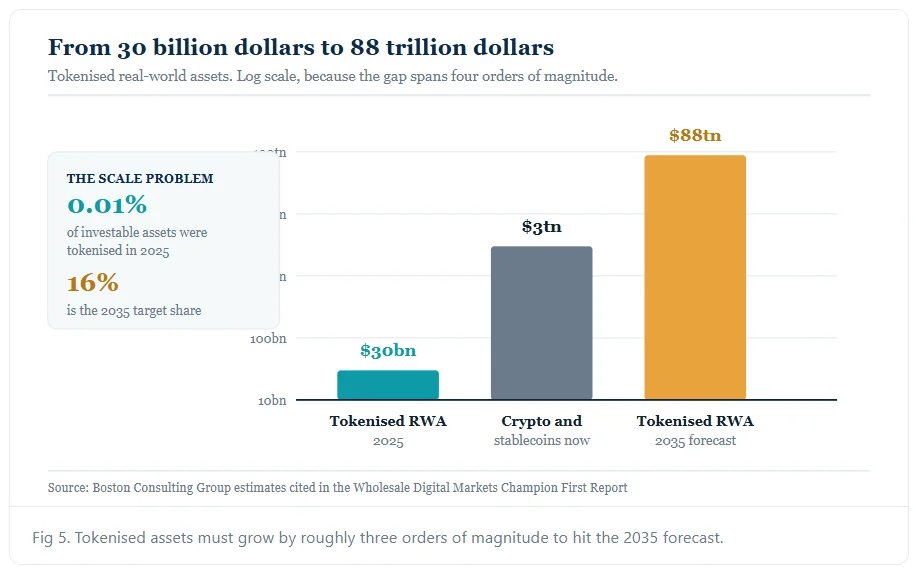

The gap between pilots and scale

Scale is the open question. Tokenised assets made up just 0.01% of the world’s investable assets in 2025. That is about $ 30 billion, and it grew by 300% over the year. Boston Consulting Group sees 88 trillion dollars by 2035, or 16% of investable assets.

Britain’s own progress shows the distance left to run. Sixteen firms are operating within the Digital Securities Sandbox today. But all of them are still at Gate 1, the test stage. None yet does live business at Gate 2.

Risks the report admits

Timing creates friction. The PRA has pushed back its work on lasting capital rules to 2028 at the earliest. Meanwhile, the FCA opens its crypto licence window on 30 September 2026. That regime bites in October 2027.

Split liquidity is the second risk. Trading could break up across rival chains, forming what the report calls “walled gardens”. Shared standards therefore sit at the heart of the work plan.

Rivals add to the pressure. Hong Kong has already sold digital government bonds. Singapore tests cross-border links through Project Guardian. Yet no country has reached full market scale so far. That gap is Britain’s opening.

What to watch next

City policy chief Chris Hayward went further, calling the shift “a digital Big Bang in financial services”. Chancellor Rachel Reeves tied it to Britain’s rank in world finance. All three now own a clock with dates on it.

Britain has the players and the deadlines. Delivery alone determines whether 33 billion pounds remains a forecast or becomes revenue.