April 14, 2026 – Goldman Sachs posts second-highest revenue in its history. JPMorgan, Netflix, Bank of America, and Johnson & Johnson are next. Here is what the numbers mean.

In Summary

Goldman Sachs posted Q1 net revenue of $17.23B, up 14% year over year.

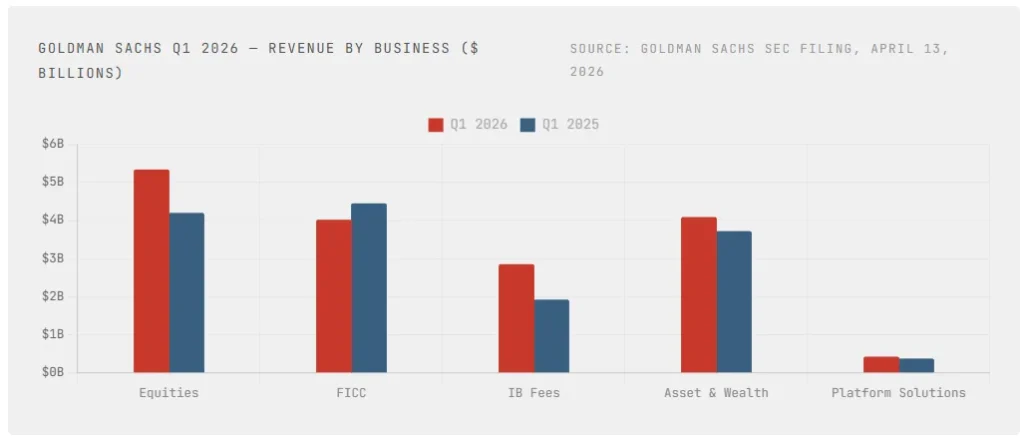

Equities trading set a record at $5.33B, up 27% year over year.

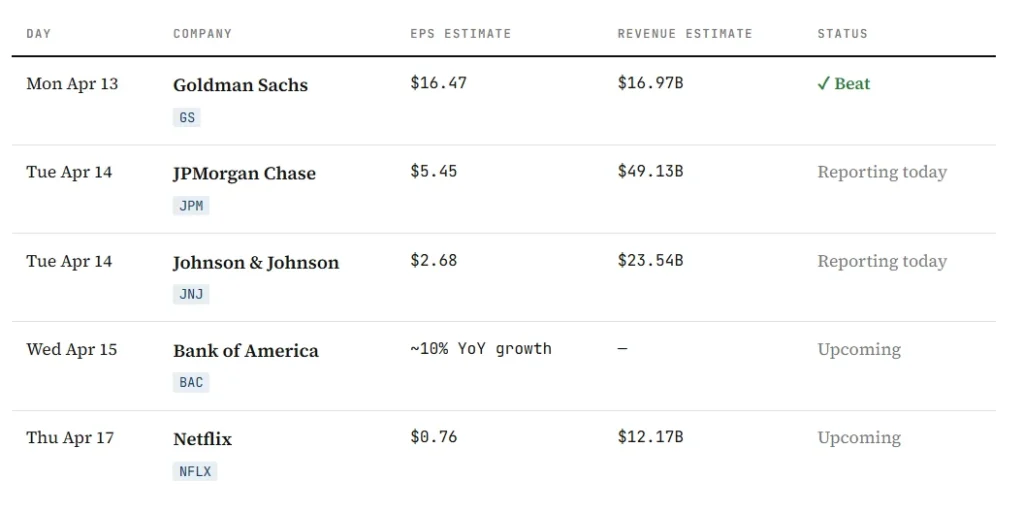

JPMorgan reports Tuesday. Analysts forecast $5.45 EPS, a 7% YoY gain.

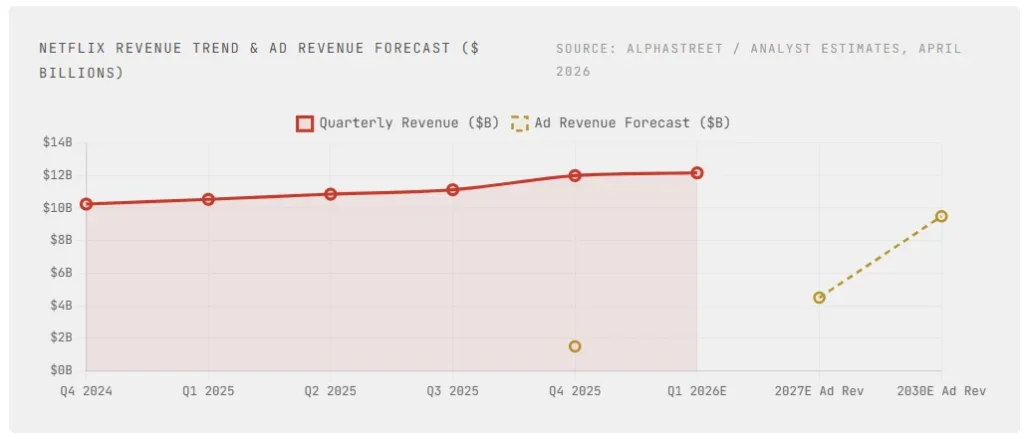

Netflix reports on Thursday. Revenue consensus is $12.17B, up 15% YoY.

PPI data this week will test whether energy inflation from the Iran war is spreading.

Q1 2026 earnings season is off to a powerful start. Goldman Sachs kicked off Monday with results that beat every major estimate. Net revenues hit $17.23 billion, up 14% from a year ago. Net earnings rose 19% to $5.63 billion. Earnings per share landed at $17.55, versus the $16.47 consensus, a 6.5% beat.

These figures ranked as the second-highest quarterly totals in Goldman’s history. The firm’s equities desk drove much of the outperformance. Equities revenue reached a record $5.33 billion, a 27% year-over-year surge. Prime brokerage and cash equities were the key growth engines.

Goldman’s Record Quarter in Detail

Investment banking fees surged 48% year over year to $2.84 billion. Completed mergers and acquisitions drove advisory revenues 89% higher. Not everything shone, however. Fixed income, currency, and commodities revenue fell 10% to $4.01 billion. Interest-rate products and mortgage trading weighed on that segment.

Goldman delivered very strong performance for our shareholders this quarter, even as market conditions became more volatile.

— Goldman Sachs Q1 2026 Earnings Release, April 13, 2026

The firm’s annualised return on equity reached 19.8%. Book value per share rose to $361.19, up 1.0% year to date. Goldman also returned $6.38 billion to common shareholders in the quarter. Despite the strong numbers, shares fell 3.06% in pre-market trading. That disconnect reflects broader market anxiety around geopolitical risk.

What to Watch: JPMorgan, Bank of America, and J&J

Several of the biggest names on Wall Street report this week, with JPMorgan Chase kicking off on Tuesday before the market opens. Analysts expect EPS of $5.45, a 7% year-over-year increase. Revenue consensus sits at $49.13 billion. The bank has beaten analyst estimates consistently in recent quarters.

Johnson & Johnson also reports on Tuesday. Analysts project EPS of $2.68 and revenue of $23.54 billion. That revenue figure would represent 7.5% year-over-year growth. J&J has beaten EPS estimates in nine of the past ten quarters. Shares are up 14.8% year to date, ranking among the Dow’s top performers.

Bank of America follows on Wednesday. Analysts and Morningstar note that loan demand through February rose 10–11% annually. Commercial and industrial loan growth came in at a strong 22%. HSBC upgraded Bank of America to Buy, citing fixed-asset repricing and balance sheet growth. The bank has a historical earnings-beat rate of 81%, per Bespoke Investment Group.

Netflix: Ad Revenue and Pricing Power in Focus

Netflix reports Thursday after the closing bell. Analysts project Q1 revenue of $12.17 billion, up 15.3% year over year. Consensus EPS stands at $0.76, a 15% gain from Q1 2025. Netflix guided net income to reach $3.26 billion for the quarter. Operating margin is expected at a strong 32.1%.

Two big catalysts are in focus for Thursday’s print. First, advertising. Analysts project ad revenue to grow from $1.5 billion in 2025 to $4.5 billion by 2027. By 2030, ad revenue could approach $9.5 billion annually. Second, pricing power. In March 2026, Netflix raised its premium ad-free tier to $26.99. JPMorgan estimates the price hikes alone could add $1.7 billion in annualised revenue.

Macro Watch: PPI and the Iran Inflation Risk

Beyond earnings, producer price index data arrives this week. Energy inflation linked to the ongoing U.S.–Iran conflict is expected to lift the headline PPI. Zacks analysts note that S&P 500 Q1 earnings are expected to grow 13.1% on 9% higher revenues. That would mark the sixth consecutive quarter of double-digit profit expansion. Still, investors will watch for any guidance that signals supply-chain pressure is spreading.

Goldman’s record equities beat confirms that volatile markets boost trading desks. The question for JPMorgan, Bank of America, and Morgan Stanley is whether investment banking can hold. Late-quarter slowdowns in deal timelines, driven by geopolitical uncertainty, may compress fee growth. Net interest income guidance will be the most closely-watched line in every bank’s release.

With the Federal Reserve unlikely to cut rates in 2026, asset repricing tailwinds remain. The week’s data from earnings to PPI will set the tone for the rest of Q2.