June 26, 2026 – A 50-bank task force wants same-day currency settlement, and regulated euro and won stablecoins sit at its center.

In Summary

Chainlink and more than 50 banks launched Project Pangea on June 23, 2026.

The coalition wants T+0, or same-day, settlement for euro and Korean won trades.

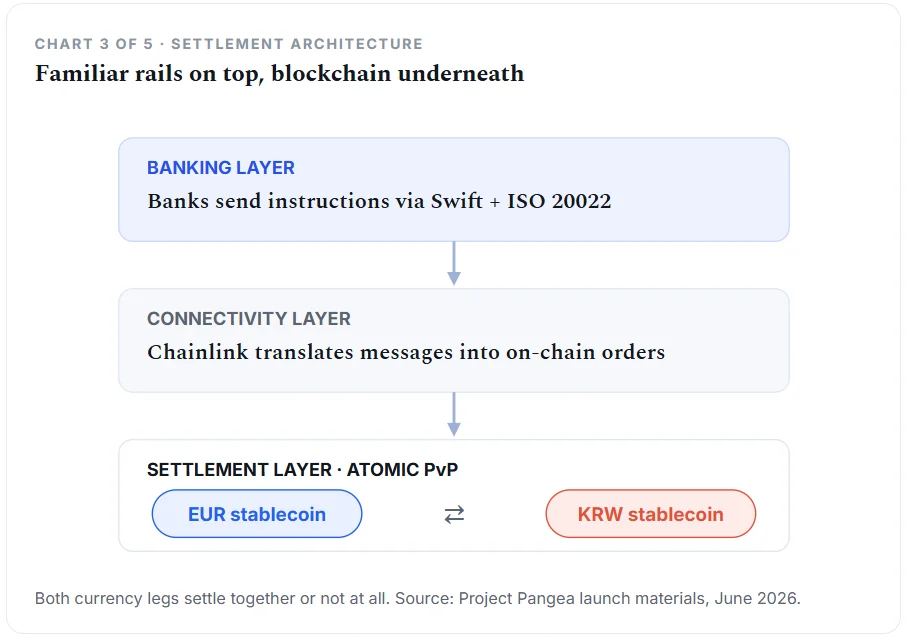

Banks keep Swift and ISO 20022 messaging, while settlement shifts on-chain.

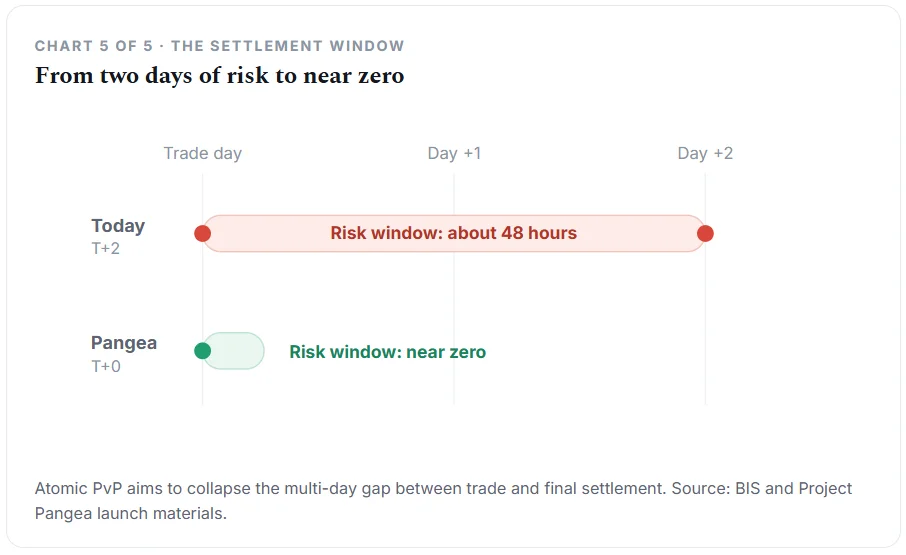

BIS data show that over $1.4 trillion in daily trades remain fully exposed to settlement risk.

An old banking problem meets a new fix

Chainlink has joined dozens of banks to rebuild how currencies settle. The group calls the effort Project Pangea. Members unveiled the plan on June 23, 2026.

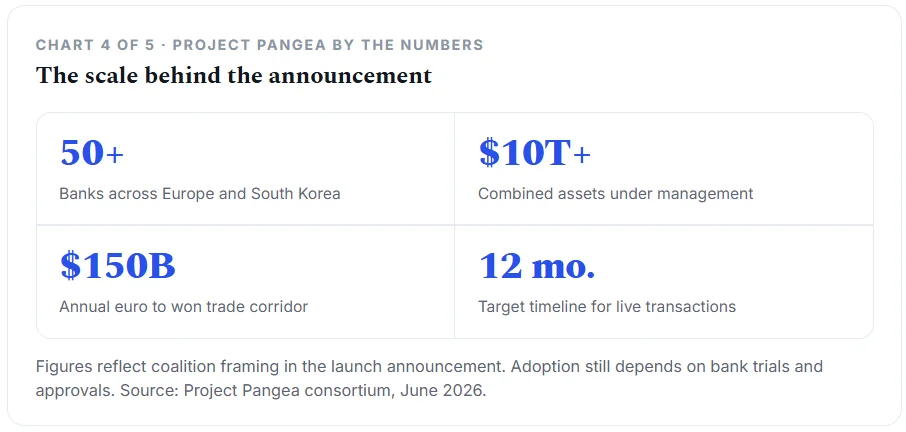

The task force spans Europe and South Korea. Together, these institutions manage more than $10 trillion in assets. Qivalis brings 37 European banks to the euro side. UniKA leads the Korean side, which includes Shinhan Bank, JB Bank, and Kbank.

Their shared goal sounds simple. They want Euro and Korean won trades to settle on the same day. Currently, many such trades still take two business days to finish.

Why settlement timing matters

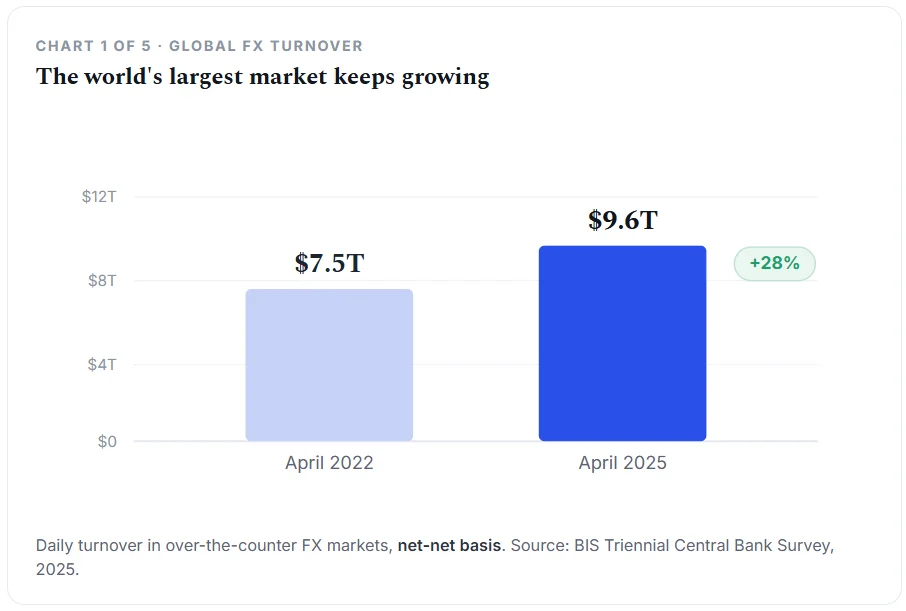

Foreign exchange is the world’s largest market. Trading reached $9.6 trillion per day in April 2025, up 28% from three years earlier. However, fast trading does not mean fast settlement.

Settlement risk lives in the gap between payment and receipt. One bank can send its currency before the other side pays. The 1974 failure of Bankhaus Herstatt first exposed this danger. Each delay also ties up capital that banks could deploy elsewhere.

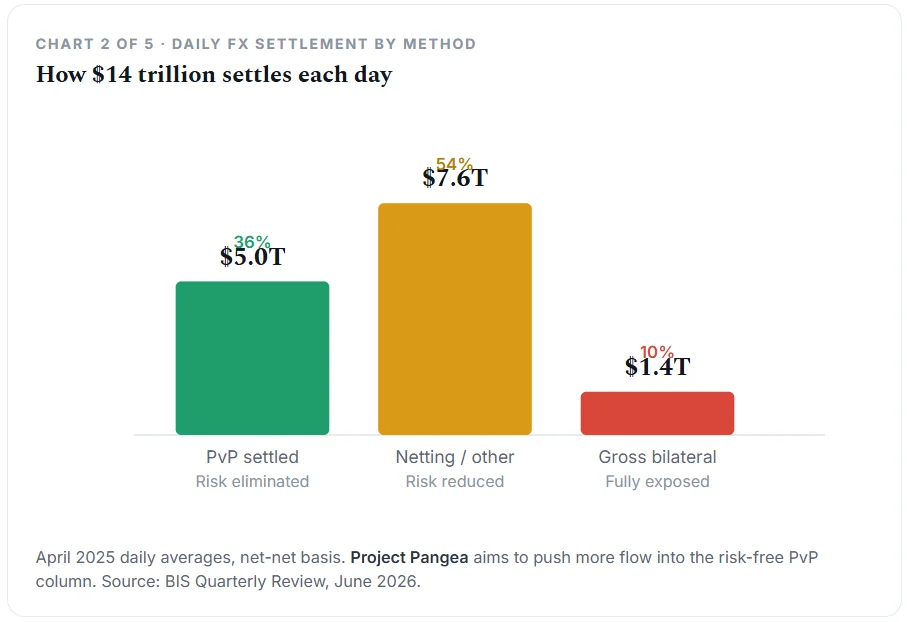

Recent figures show the problem endures. The BIS reports that more than $1.4 trillion settles daily on a gross bilateral basis. That slice, near 10%, stays fully exposed to settlement risk. Another $7.6 trillion uses methods that reduce, but do not eliminate, this risk.

How Project Pangea works

Pangea attacks this gap with atomic settlement. In plain terms, both currency legs move together or not at all. Engineers call this design payment-versus-payment, or PvP.

Importantly, banks do not rebuild their systems. They keep Swift messaging and the trusted ISO 20022 standard. Chainlink infrastructure then converts those instructions into on-chain actions. Its CCIP standard also enables tokens to move across networks.

The settlement layer relies on regulated stablecoins for each currency. A compliant euro token meets a compliant won token directly. As a result, the trade skips slow intermediary currencies, often the US dollar.

A focused trade corridor

Pangea targets a real economic link, not a generic demo. The euro-to-won corridor moves more than $150 billion in goods and services annually. Therefore, member banks gain a live setting to test the design.

Chainlink also brings a track record to the table. The network previously ran tokenization pilots with Swift and UBS. Moreover, it completed a currency swap test with Visa across Hong Kong and Australia. These pilots returned to one stubborn question. They asked how tokenized money fits existing bank workflows.

The euro and won legs still need work

Qivalis gives the euro side real weight. The consortium grew from 12 banks to 37 by May 2026. ING reported that Qivalis plans to launch a regulated euro stablecoin in late 2026, pending approval.

Still, key questions stay open. Banks have not named the exact tokens for live trades. Liquidity, redemption, and dispute rules also need clear answers. Furthermore, regulators in both regions must approve the model.

The Korean leg carries similar caveats. FairSquareLab supplies the on-chain settlement technology, while UniKA gathers the banks. Yet final rules for won settlement remain undecided.

The bigger stablecoin stakes

The project also fits a larger contest over digital money. Dollar stablecoins still dominate on-chain finance today. A working euro token could shift some of that balance. For Korea, the won could reach global markets more directly.

However, scale will decide whether this vision holds. Analysts note that announcements rarely equal adoption. Real volume, not press releases, builds market infrastructure.

Regulators are also moving faster on stablecoin rules this year. Both Europe and Korea now shape clearer frameworks. That clarity could help banks treat the tokens as real instruments. Even so, legal treatment across two regions remains complex.

What to watch next

The first signal is movement from announcement to real trials. A live test would reveal the tokens, the flows, and the safeguards. Banks expect live transactions within roughly 12 months.

The second signal is bank-grade trust in both stablecoins. Deep liquidity and reliable redemption would matter most. Without them, the framework stays a neat diagram rather than a market.

The third signal is whether familiar messaging cuts adoption friction. If teams test settlement without new systems, stablecoins gain a foothold. Therefore, the coming year will test promise against practice.

Project Pangea places regulated stablecoins against a genuine banking pain point. The technology already works on paper. The harder task is turning it into a routine settlement infrastructure.