April 28, 2026 – Iran’s yuan ultimatum at the Strait of Hormuz is more than a diplomatic gambit. It is the most operationally specific challenge to the petrodollar since 1974, and the data shows why it matters.

In Summary

Iran’s Yuan ultimatum conditions Strait of Hormuz access on yuan payment, the first such demand in modern oil history.

Yuan trade share rose from under 1% in 2012 to 3.7% in 2024, with 30% of China’s $6.2T trade now yuan-settled.

The CIPS network now connects 1,500+ banks across 110 countries, with volume tripling since 2024, bypassing SWIFT entirely.

UAE and India have both signalled or executed yuan-based oil transactions, cracking the Gulf’s petrodollar consensus.

The dollar remains dominant at 57% of global reserves; the yuan holds just 2–3.5%, but the direction of change is unmistakable.

A single waterway now carries two battles. The Strait of Hormuz, through which roughly one-fifth of global oil flows, has become the frontline of a currency war. Iran has reportedly offered limited tanker access on one condition: payment in Chinese yuan.

The move is deliberate. It is surgical. And it is backed by a financial architecture already in motion.

The Strait as a Currency Checkpoint

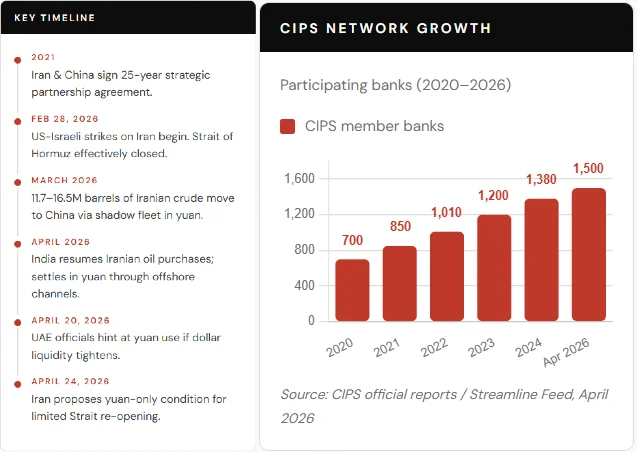

Since late February 2026, Iran has effectively closed the Strait to most commercial shipping. US military operations against Tehran triggered the blockade. But Iran’s response was not purely military. Between 11.7 and 16.5 million barrels of Iranian crude have since moved to China via shadow fleet, all settled in yuan. China’s tankers move freely. Everyone else is locked out.

Tehran is now offering to formalise that arrangement. Pay in yuan, and passage opens. The proposal reframes what was a military choke point into a monetary toll booth.

“This is not merely a tactical maneuver. It is the latest manifestation of a structural realignment gathering momentum for over a decade.”

— Economist Antonio Bhardwaj, Foreign Affairs Forum

The Yuan’s Quiet Rise in Numbers

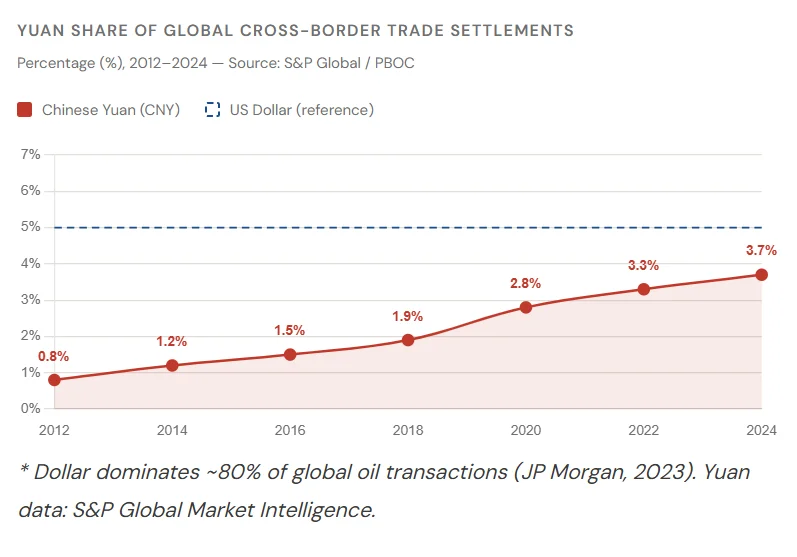

To understand the stakes, look at the trajectory. The yuan’s share of global cross-border trade settlements has risen sharply. It stood at less than 1% in 2012. By 2024, that figure reached 3.7%, according to S&P Global.

That still sounds small. But the direction of travel is consistent. And the pace is accelerating.

Inside China’s own trade network, the shift is more dramatic. Deputy PBOC Governor Zhu Hexin confirmed that yuan now settles 30% of China’s $6.2 trillion in global goods trade. Beijing is no longer piloting yuan internationalisation. It is executing it at scale.

The CIPS Network: A Shadow SWIFT

Iran and China do not rely on Western financial infrastructure. They use the Cross-Border Interbank Payment System, CIPS. Beijing built it as an alternative to the SWIFT network. It now spans over 1,500 banks across 110 countries, as of April 2026. Daily transaction volume has tripled since 2024.

The practical result: sanctioned economies can move money without touching US-controlled rails. Iran reportedly conducts over 80% of its oil trade with China in yuan. That figure would have seemed impossible five years ago.

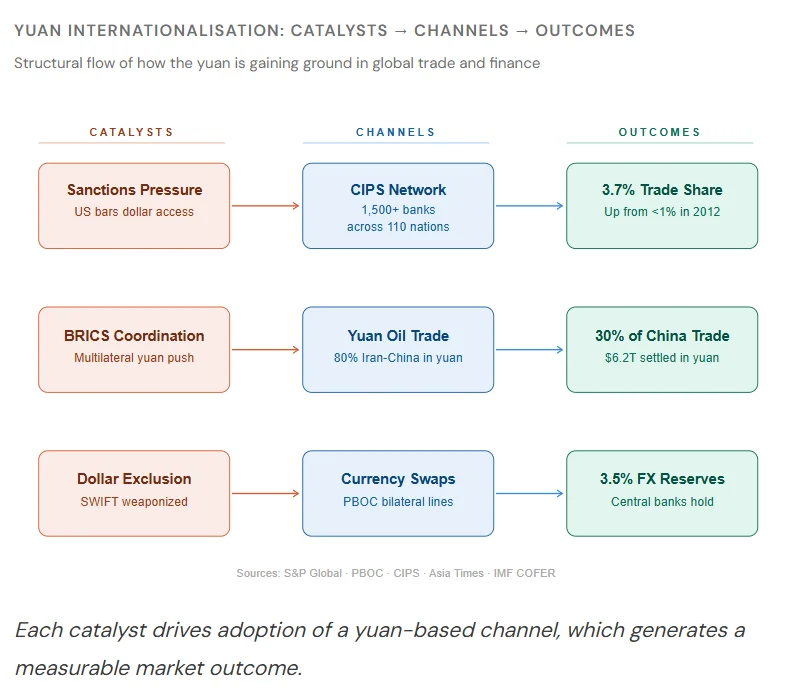

How Yuan Acquires Global Market Share

The yuan’s expansion follows a three-stage architecture. External pressure forces countries to seek dollar alternatives. Purpose-built channels move value in yuan. The result is measurable shifts in the data.

Cracks in the Gulf’s Petrodollar Pact

The petrodollar system was formalised in 1974. Saudi Arabia priced its exports in dollars. That created a self-reinforcing loop. Every oil importer needed dollars. Every central bank held dollars. The arrangement has governed global finance for fifty years.

Now the edges are fraying. UAE officials have privately raised the possibility of using yuan for oil transactions if dollar liquidity tightens. The UAE holds $270 billion in foreign-exchange reserves. But Iran’s blockade has damaged its energy infrastructure and suppressed dollar-denominated revenue. Even a hint from a Gulf state is seismic.

Deutsche Bank analysts warned last month that the Iran conflict “could worsen cracks already forming in the petrodollar regime.”

India’s Yuan Pivot: A Test Case

India has become an early case study. After a seven-year pause, Indian refiners resumed Iranian crude imports. Payments were processed in yuan through offshore banking channels to avoid US sanction exposure. The transaction was limited in scope. But it proved the mechanics work.

Dollar-denominated deals pass through the US financial system. Yuan deals do not. That distinction is increasingly valuable to buyers and sellers alike.

What the Data Cannot Show

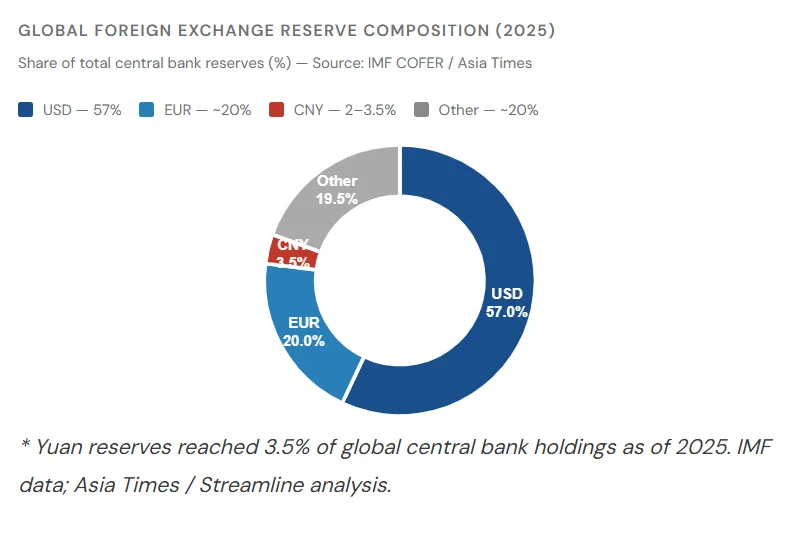

The yuan faces structural limits that are not reflected in trade volumes. China’s capital controls prevent the free flow of money across its borders. A true reserve currency must be convertible and backed by a credible legal system. The yuan meets neither criterion fully.

At just 2% of global foreign exchange reserves, the yuan lags far behind the dollar’s 57% share. Harvard economist Kenneth Rogoff puts it plainly: “the dollar isn’t about to be dethroned overnight.” Alicia Garcia-Herrero of Natixis argues the yuan’s role “adds incremental pressure and normalises alternatives in energy flows”, but stops short of reshaping the system.

The change, as consultant Dan Steinbock frames it, is “gradual erosion rather than abrupt substitution.”

The Architecture Is Already Operating

That framing may be too reassuring. The difference today is operational. Previous de-dollarisation talk was theoretical. Now there is a chokepoint, a shadow fleet, a live payment system in yuan, and no diplomatic resolution in sight.

Iran’s yuan ultimatum does not break the petrodollar today. But it forces the world’s biggest energy importers to make a binary choice at the world’s most critical chokepoint. That choice and its precedent may matter more than any single trade flow.

The petroyuan is no longer a concept. It is a corridor.