May 05, 2026 – AI data company shatters forecasts, raises 2026 guidance to $7.65B as U.S. commercial revenue surges 133%.

In Summary

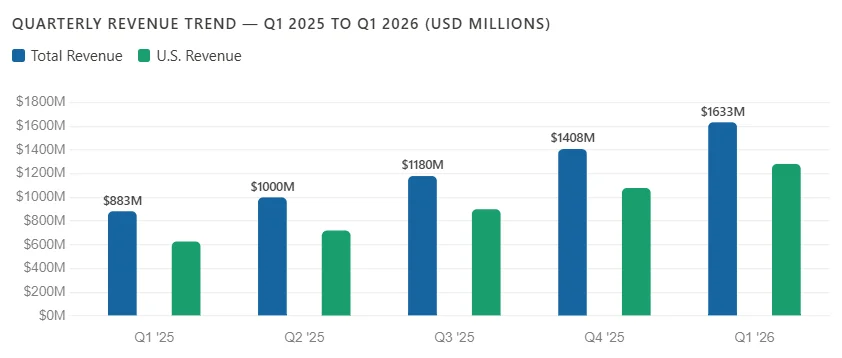

Revenue rose 85% YoY to $1.633B, beating the $1.54B analyst consensus by ~$93M.

U.S. commercial revenue surged 133% to $595M; 615 enterprise customers, up 42% YoY

GAAP net income reached $871M, a 53% margin, a fourfold jump from Q1 2025

Rule of 40 score hit 145%, nearly four times the elite software industry benchmark

Full-year 2026 guidance raised to $7.65–$7.66B, implying 71% annual revenue growth

Palantir Q1 2026 earnings shattered Wall Street expectations on May 4, 2026. The AI data company posted revenue of $1.633 billion, 85% above Q1 2025 levels. Analyst consensus had forecast $1.54 billion. The beat was nearly $100 million. CEO Alex Karp called it the best quarter in the company’s history.

U.S. Growth Dominates All Segments

The United States is now Palantir’s dominant growth engine. Total U.S. revenue grew 104% year-over-year. It reached $1.282 billion in the first quarter. That represents 78% of all company revenue.

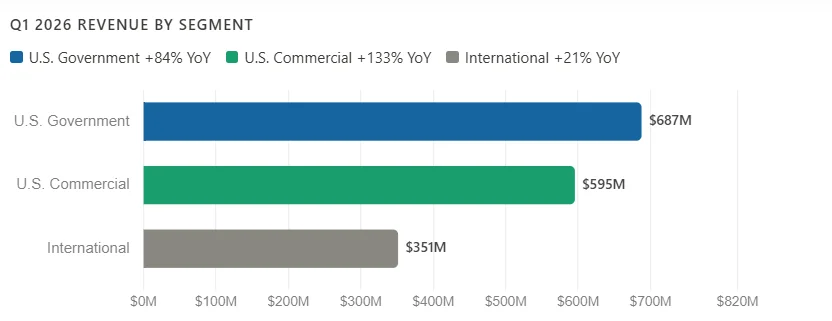

The U.S. commercial segment delivered the standout performance. It grew 133% to $595 million. Government contracts contributed $687 million, up 84% year-over-year. Government growth accelerated from 66% in Q4 2025. Palantir closed 206 deals worth $1 million or more during the quarter.

The company ended Q1 with 615 U.S. commercial customers, a 42% increase from one year ago. New deals included Airbus, Bain Capital, GE Aerospace, and Stellantis. Total contract value for the quarter reached $2.41 billion.

Record Profitability Across All Metrics

Palantir’s profitability story matches its growth story. GAAP net income reached $871 million, a 53% net margin. One year ago, net income was $214 million. That is a fourfold improvement in twelve months. GAAP diluted EPS came in at $0.34, up from $0.08 in Q1 2025.

Adjusted income from operations hit $984 million, a 60% margin. Adjusted free cash flow was $925 million. Revenue per employee reached $1.5 million annualised. This efficiency benchmark is exceptional even by elite software standards.

“Palantir’s Rule of 40 score hit 145%, nearly four times the benchmark that separates elite software companies from ordinary ones.”

The “Rule of 40” score combines revenue growth rate with profit margin. A score above 40 defines elite software performance. Most leading software companies cap out near 60–70. Palantir’s 145% score places it in genuinely uncharted territory.

AIP Platform Fuels Commercial Demand

Palantir’s Artificial Intelligence Platform, known as AIP, is the core driver of commercial growth. AIP launched in April 2023. It enables enterprises to deploy AI agents using their own secure data. The platform integrates large language models into live operational workflows.

Palantir uses a “bootcamp” model to accelerate AIP adoption. Enterprises run intensive pilots. They then convert quickly to long-term contracts. This approach drove 42% year-over-year growth in commercial customers. CEO Karp confirmed to CNBC that he expects U.S. business to double again by 2027.

AIP’s proprietary Ontology layer, a knowledge graph connecting AI outputs to real business objects, creates deep customer lock-in. Once deployed, the system is difficult to replicate or replace. This structural advantage supports durable pricing power.

Guidance Raised Significantly for Full-Year 2026

Management raised full-year 2026 revenue guidance to $7.65–$7.66 billion. This implies 71% annual growth. The prior guidance range was $7.18–$7.20 billion. The revision is substantial, more than $460 million higher.

Adjusted free cash flow guidance was raised to $4.2–$4.4 billion. Adjusted income from operations guidance increased to $4.44–$4.45 billion. U.S. commercial revenue guidance was lifted to over $3.224 billion, at least 120% annual growth. Q2 2026 revenue guidance of approximately $1.8 billion surpassed analyst forecasts of $1.68 billion.

Analyst Reactions and Valuation Debate

Wall Street reactions reflect a familiar Palantir divide. The underlying results are universally impressive. But the valuation polarises analysts sharply. PLTR trades at approximately 226 times trailing earnings.

Wedbush reiterated Outperform with a $230 price target, labelling Palantir a potential “trillion-dollar AI company”. Oppenheimer initiated at Outperform with a $200 target. DZ Bank issued a Buy with a $175 target. Citi holds the Street-high target at $260.

HSBC holds a contrarian position. It was downgraded to Hold with a $151 target. The bank cited growing competition from OpenAI, Anthropic, and the proliferation of AI tooling as key risks. Investors are watching whether AIP’s moat holds as commoditised AI alternatives scale.

Bottom Line

Palantir delivered a quarter that exceeded even its most optimistic supporters’ forecasts. Revenue, profit, and guidance all beat consensus. Ten consecutive quarters of accelerating revenue confirm structural momentum, not a cyclical bump. The critical question heading into H2 2026: can AIP adoption sustain triple-digit commercial growth? The Q2 2026 earnings report will be the next key test.