May 23, 2026 – Record Q1 profits meet an AI spending surge. Investors want clear answers on returns, and they are not getting them yet.

In Summary

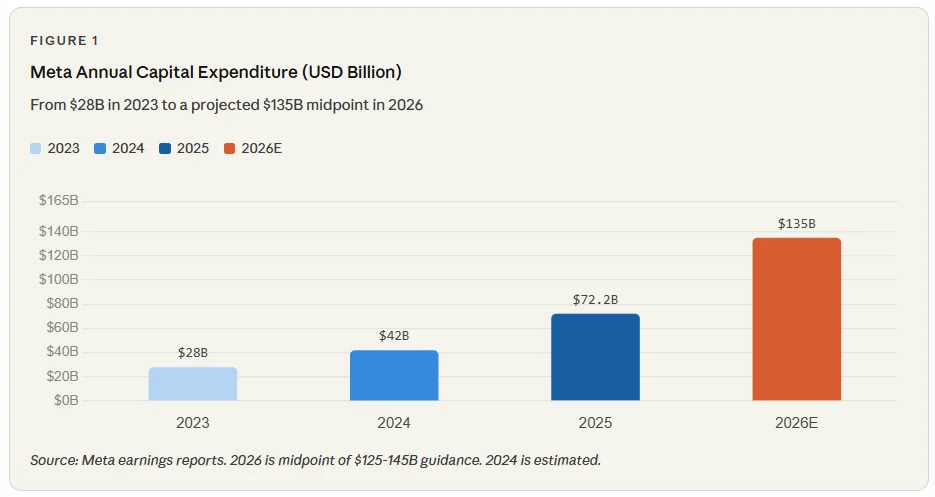

Meta raised 2026 capex guidance to $125-145B, nearly doubling its 2025 spend of $72.2B.

Q1 revenue grew 33% to $56.3B, but the stock dropped 6% after hours on a capex shock.

DRAM memory prices surged 17 times in one year, fuelling a new trend analysts call “chipflation.”

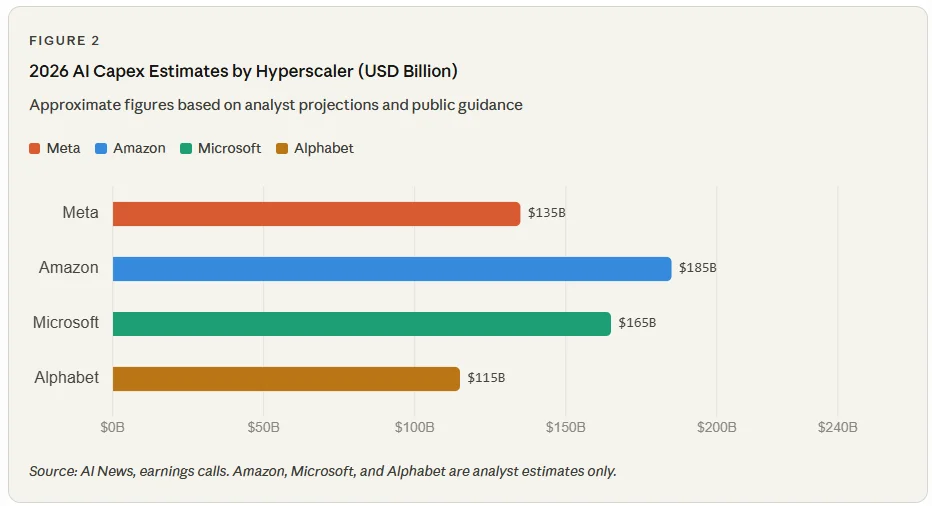

Big Tech’s combined AI capex for 2026 is projected to exceed $640B across four hyperscalers.

Meta is cutting 8,000 jobs while simultaneously scaling AI infrastructure spending.

Meta Platforms is spending like never before. The company raised its 2026 capital expenditure guidance to $125-$145 billion. This nearly doubles the $72.2 billion in capex Meta spent in 2025. Yet investors are not applauding.

The stock fell 6% in after-hours trading after the earnings release. Year-to-date, shares remain roughly 6.5% lower. Wall Street stopped caring about strong profits the moment Mark Zuckerberg opened the capital expenditure firehose.

Strong Q1, Two Very Different Stories

Meta’s Q1 2026 earnings looked exceptional on paper. Revenue surged 33% year-over-year to $56.3 billion. Operating income climbed 30% to $22.9 billion. Profits jumped 61% to $26.8 billion, partly boosted by an $8 billion tax benefit.

The advertising engine remains formidable. Ad impressions rose 19% in Q1. Furthermore, average ad prices climbed 12% over the same period. North American average revenue per user (ARPU) reached $15.82, up 28.2% year-over-year. Daily active users hit 3.56 billion, up 4% across all platforms.

However, total Q1 expenses ballooned 35% to $33.4 billion. Infrastructure costs and employee compensation drove most of that rise. CFO Susan Li confirmed this on the earnings call. The gap between revenue strength and cost growth is closing fast.

In 2023, Meta spent just $28 billion on capex. By 2025, that figure had risen to $72.2 billion. The 2026 midpoint guidance now stands at $135 billion. Therefore, capital expenditure has grown nearly five times in just three years.

Chipflation Is Driving Costs Higher

CFO Susan Li cited “higher component pricing” as the primary cost driver behind the guidance increase. According to BlackRock research, DRAM memory prices surged 17 times over the past year. This reverses decades of steady declines in semiconductor prices tied to Moore’s Law.

Analysts now call this trend “chipflation.” It describes a demand shock so intense that trillion-dollar companies pay steep premiums. Consequently, the more AI products Meta builds, the more expensive they become to build.

“Scale the product first, then monetize later.”

-Mark Zuckerberg, Meta CEO, Q1 2026 Earnings Call

Meta is responding by diversifying its hardware stack. Zuckerberg confirmed the company is deploying over 1 gigawatt of custom silicon co-developed with Broadcom. Additionally, Meta is scaling commitments with AMD, Nvidia, AWS Graviton, and other compute providers. The strategy aims to reduce reliance on any single supply chain.

Big Tech’s $640 Billion Arms Race

Meta is not fighting this battle alone. Microsoft, Alphabet, Amazon, and Meta collectively committed an estimated $630- $ 650 billion in AI capex for 2026. This is the largest single-year infrastructure buildout in corporate history.

However, Alphabet stands out as the cleaner story. Google Cloud revenue jumped 63% to $20 billion in Q1. Its cloud backlog nearly doubled to over $460 billion. This gives Alphabet a measurable, fast-growing return on its AI spending.

Amazon similarly pointed to strong AWS growth as direct evidence of AI return on investment. Meta, by contrast, still relies largely on advertising optimization for near-term returns. Its AI-powered ad platform, Advantage+, remains the most direct revenue link so far.

Jobs Out, AI Machines In

While pouring billions into AI infrastructure, Meta is simultaneously cutting staff. The company plans to reduce its workforce by roughly 8,000 employees, or about 10% of total headcount. These are the largest layoffs since the “Year of Efficiency” cuts in 2023. The company is, in effect, replacing human workers with AI machines.

Moreover, multi-year infrastructure contract commitments surged by $107 billion in a single reporting period. This locks in massive future costs before AI revenue has scaled meaningfully. It also signals that Zuckerberg views this infrastructure build-out as a non-negotiable priority.

The ROI Question Remains Open

Investors pressed Zuckerberg on the AI return on investment during the earnings call. His response raised eyebrows. He called the question “very technical” and quickly reverted to Meta’s long-standing playbook: scale first, then monetize.

That strategy worked well for Facebook and Instagram. However, committing up to $145 billion before proving AI revenue is an entirely different order of risk. Furthermore, CFO Li admitted that the company may continue to underestimate computing needs as AI adoption accelerates. That is a significant and candid admission.

For now, Meta’s advertising business provides a strong financial cushion. However, full-year expenses are expected to reach $162-169 billion. That leaves a narrowing gap between revenue and total costs. Investors will grow more impatient with each passing quarter. They need AI to move from a cost center to a revenue driver. Until that happens, the capex question will shadow every single earnings call.