April 29, 2026 – With conditional OCC approval secured, Mercury moves toward becoming a full national bank. Its $650M revenue and 300,000+ customers make it one of the most credible fintech charter applicants in history.

Mercury, the fintech serving over 300,000 businesses and individuals, cleared a landmark regulatory hurdle on April 27, 2026. The Office of the Comptroller of the Currency (OCC) granted the company conditional approval for a national bank charter. Mercury now moves toward establishing Mercury Bank, N.A., a federally chartered institution headquartered in Utah.

CEO Immad Akhund framed the milestone in direct terms. “Our customers have been asking for Zelle, for expanded lending, for payment infrastructure we actually control,” he said. “We couldn’t give them those things without a bank charter.”

Mercury’s Scale Makes the Case

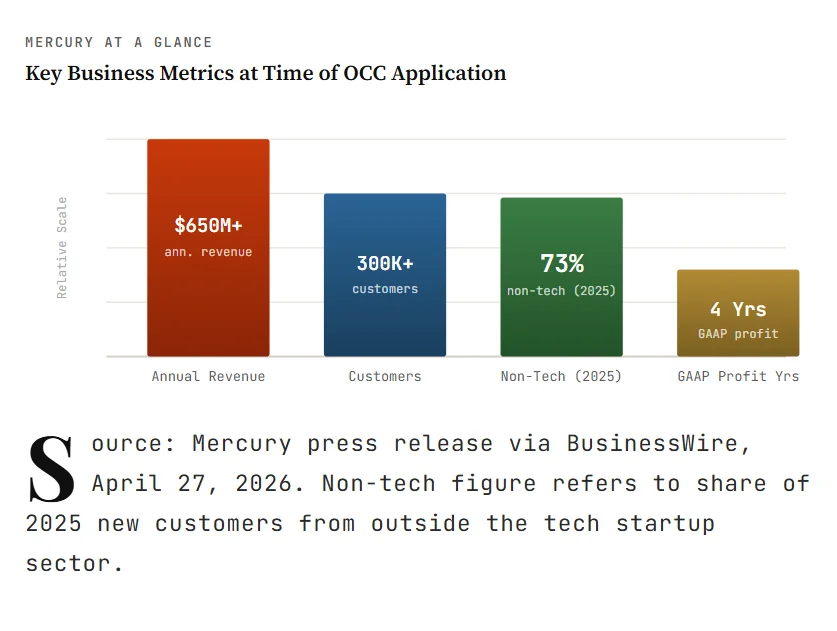

Mercury is not a startup chasing regulatory status. It is a scaled, profitable platform. The company generates more than $650 million in annualised revenue. It has maintained four consecutive years of GAAP profitability, rare in fintech. One in three U.S. startups currently banks with Mercury.

Yet 2025 revealed something bigger. That year, 73% of Mercury’s new customers came from outside the tech startup sector. Its appeal is broadening. Mercury is no longer just a tool for founders; it is becoming a mainstream business bank.

What Changes With the Charter

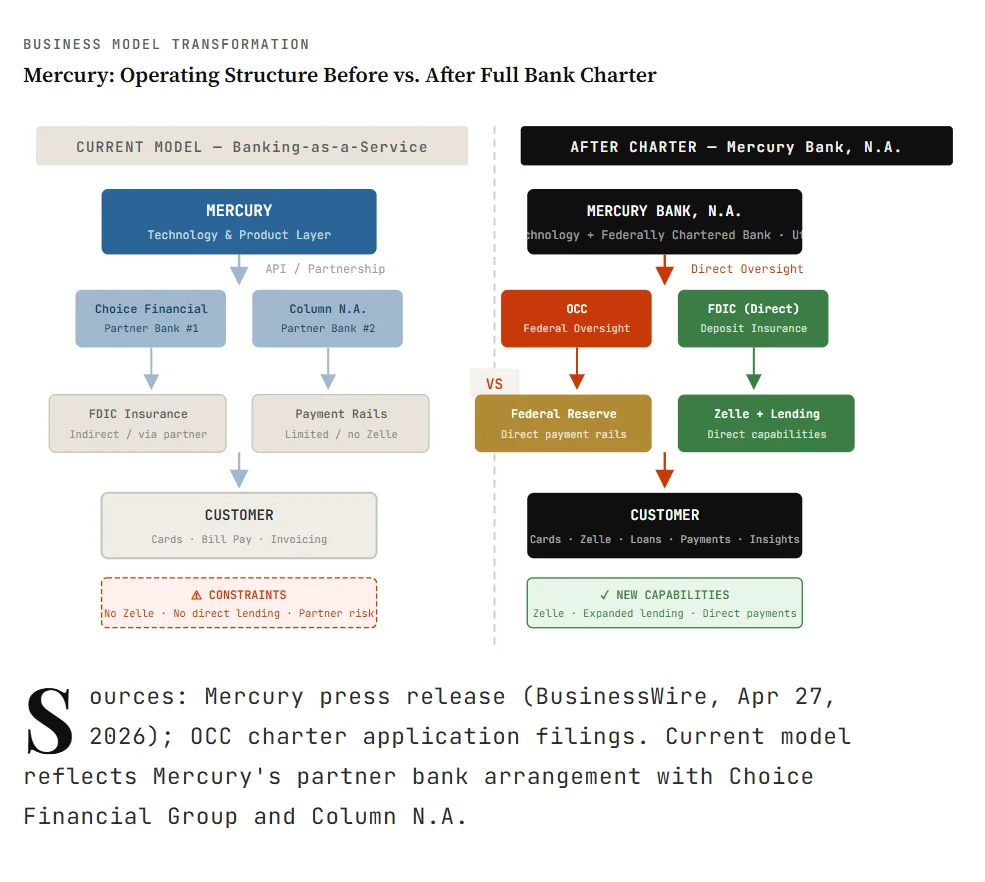

Today, Mercury operates through partner banks, Choice Financial Group and Column N.A. That model offers agility but also fragility. Partner banks can change terms. Regulators can shift rules. Customers face limitations that a direct charter removes.

Mercury Bank, N.A. will change this entirely. Customers will gain Zelle for business and personal payments, an expanded lending suite, and a deeper payments infrastructure. Mercury will control how money moves, not a third party.

Three Regulatory Hurdles Remain

Conditional approval begins a process; it does not end one. Mercury now enters the OCC’s bank organisation phase. It must satisfy all remaining OCC requirements. FDIC deposit insurance approval and Federal Reserve bank holding company status must also follow. Only then will Mercury Bank, N.A. become fully operational.

Jon Auxier will serve as Mercury Bank’s CEO and President. He previously led SoFi’s charter implementation as CFO of SoFi Bank. That hands-on experience is directly relevant. Mercury Technologies, Inc. will separately file with the Federal Reserve to become a bank holding company.

The Fintech Charter Wave: Context

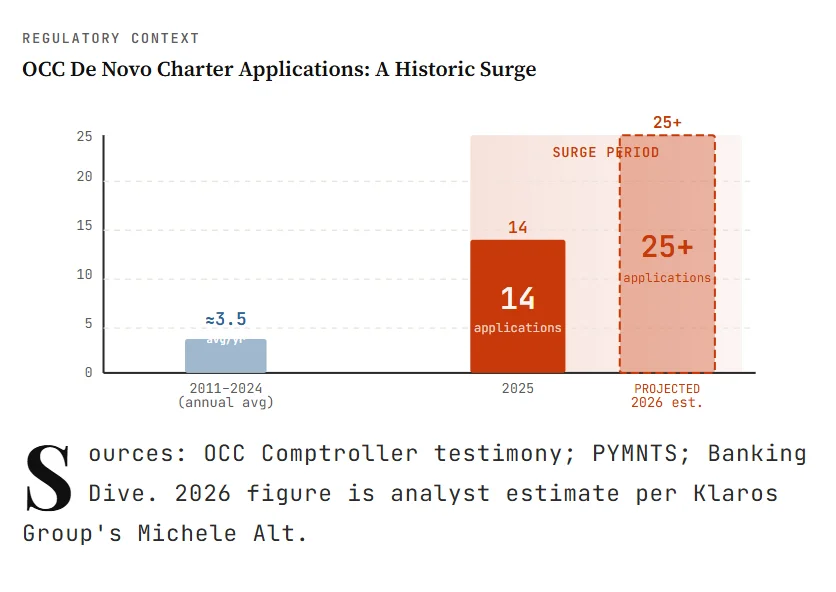

Mercury’s approval does not exist in isolation. The OCC received 14 de novo applications in 2025 alone, nearly matching the combined total from the prior four years. Before 2025, the OCC averaged fewer than four applications per year from 2011 to 2024. A regulatory reset is underway.

The Trump administration’s pivot toward financial deregulation has unlocked this demand. New OCC leadership under Comptroller Jonathan Gould signalled openness. Fintechs responded. Analysts at Klaros Group project 25+ applications in 2026. The door is open, and many are walking through.

Yet Mercury is different from most charter seekers this cycle. The majority of 2025–2026 applicants sought limited-purpose national trust charters. These do not allow deposit-taking or lending. Mercury is applying for a full-service FDIC-insured national bank charter. That places it in far rarer company.

The Financial Case for a Charter

Beyond products, the economics are compelling. QED Investors’ research shows a charter can improve a fintech’s cost of funds by up to 200 basis points. Every 1-percentage-point improvement in cost of funds boosts pre-tax ROE by roughly 6 percentage points for a lender at a 15% Tier 1 leverage ratio.

SoFi, which successfully obtained its own charter, estimated a 170-basis-point improvement in its cost of funds as of mid-2025. Mercury’s $650M+ revenue base and proven lending ambitions make similar gains realistic. A charter is not just a regulatory achievement; it is a structural profit driver.

The Bottom Line

Mercury’s conditional OCC approval is more than a regulatory checkpoint. It marks a structural shift in U.S. financial services. Scaled, profitable fintechs can now compete directly with traditional banks, not around them. The era of “banking-as-a-service” workarounds is giving way to something far more permanent. As Freshfields noted, 2026 will test how wide regulators are prepared to leave the door open, and Mercury just walked through it.