June 02, 2026 – Berkshire Hathaway, Veolia, and Servier anchor a blockbuster day of strategic deal-making. Full snapshots and individual evaluations for all 14 transactions.

In Summary

Berkshire Hathaway acquires Taylor Morrison for $8.5 billion in cash, taking the US homebuilder private.

Israel blocks ZIM’s $4.2 billion proposed sale over national security concerns, even post-shareholder approval.

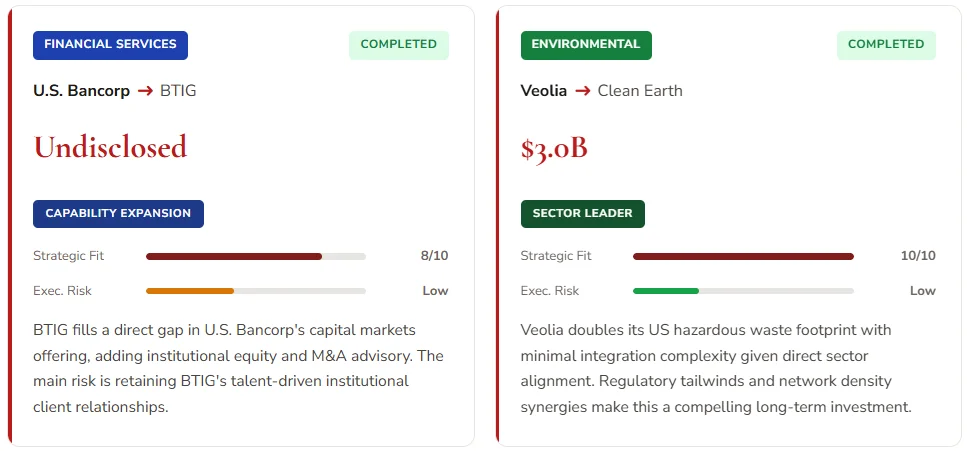

Veolia completes a $3 billion Clean Earth deal, doubling its US hazardous waste footprint.

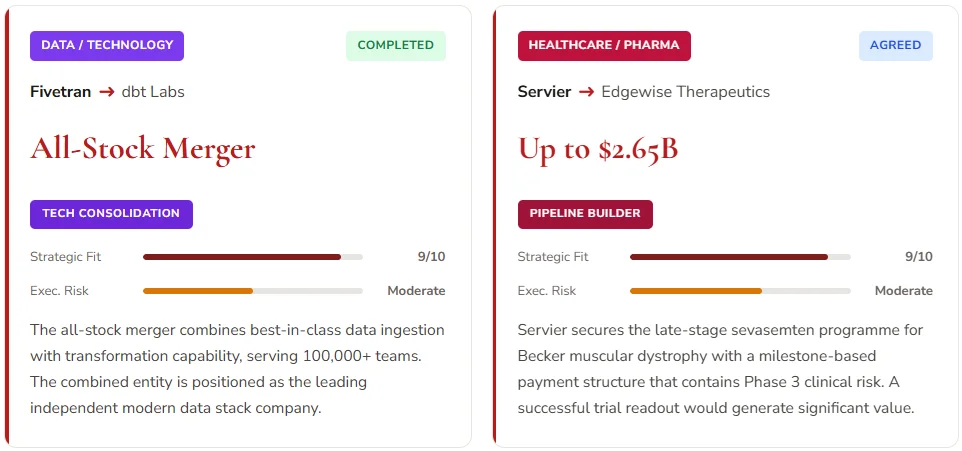

Servier pays up to $2.65 billion for Edgewise Therapeutics’ rare disease drug programme.

U.S. Bancorp, Thoma Bravo, and 26North Re expand capital markets and insurance platforms.

Global M&A activity surged to new heights by June 1, 2026. More than 14 transactions closed, advanced, or emerged formally across eight sectors. The total disclosed deal value exceeded $20 billion. This is not random activity. Rather, it reflects a deliberate strategic shift. Corporate buyers are deploying balance sheet capital with conviction. Private equity firms are building platforms with long-term consolidation logic. Together, these patterns signal a market that is both active and purposeful.

Deal-by-Deal Analysis

Individual strategic evaluation for all 14 transactions. Scores reflect strategic fit and execution risk on a 1-10 scale.

Strategic Giants Lead the Day

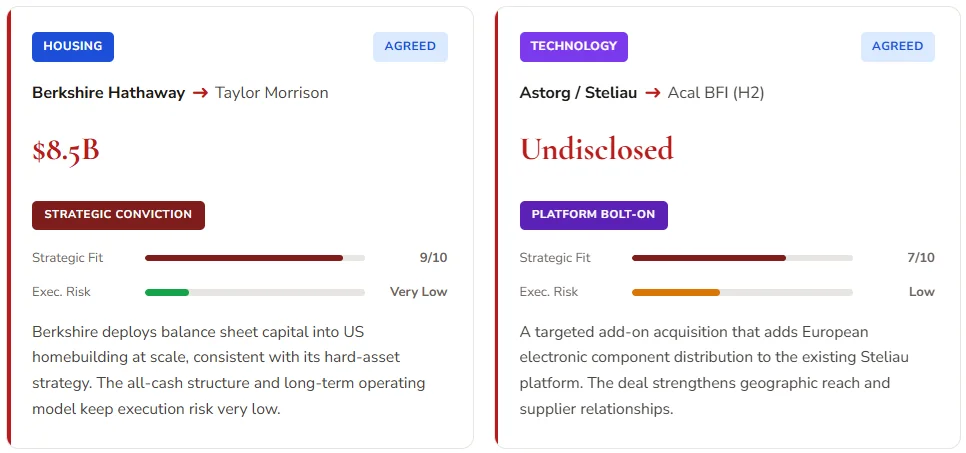

Berkshire Hathaway made the largest single announcement of the session. The conglomerate agreed to acquire Taylor Morrison for $8.5 billion in cash, per the Financial Times. This deal takes the US homebuilder fully private. Berkshire’s move reflects deep confidence in long-term US housing demand. Despite elevated mortgage rates, homebuilder margins have remained relatively strong. Furthermore, Taylor Morrison’s land bank and community pipeline offer lasting asset value.

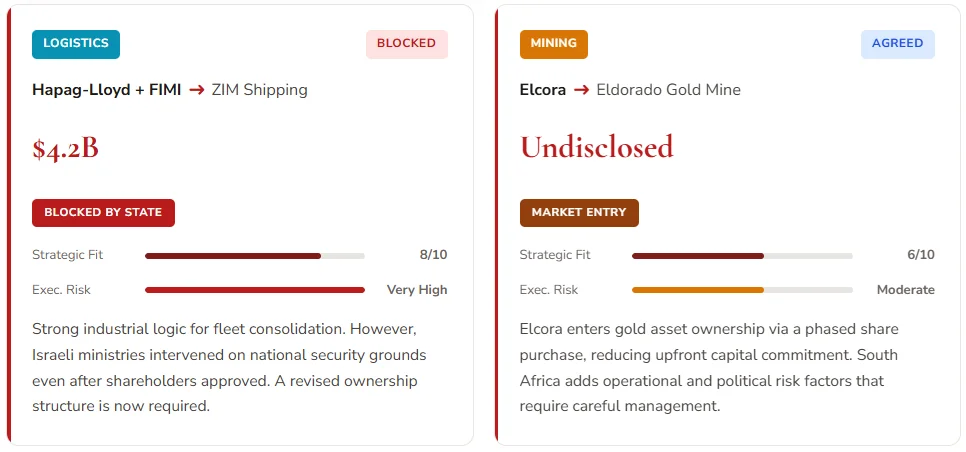

However, not every major deal moved forward without friction. Israeli ministries moved to block ZIM’s $4.2 billion proposed sale, per The Jerusalem Post. The transaction would have split ZIM between Hapag-Lloyd and private equity firm FIMI. Authorities cited national security concerns as the central reason for intervention. This move came even after shareholders had formally approved the sale. Therefore, ZIM now faces real uncertainty about its future ownership structure.

Deal Spotlight: Geopolitical Risk

The ZIM case signals a wider trend. Governments are more actively reviewing cross-border transactions in the shipping, energy, and infrastructure sectors. Acquirers must now factor political risk into deal timelines as a core variable.

Environmental Services and Natural Resources

Veolia completed a landmark acquisition in the US environmental market. The company finalized its $3 billion purchase of Clean Earth, per Business Wire. This deal doubles Veolia’s US hazardous waste business in a single transaction. Furthermore, it significantly expands the company’s treatment, storage, and disposal network. Growing regulatory pressure on industrial hazardous waste makes this a well-timed acquisition. Veolia now holds a stronger, scaled position in a fast-growing domestic market.

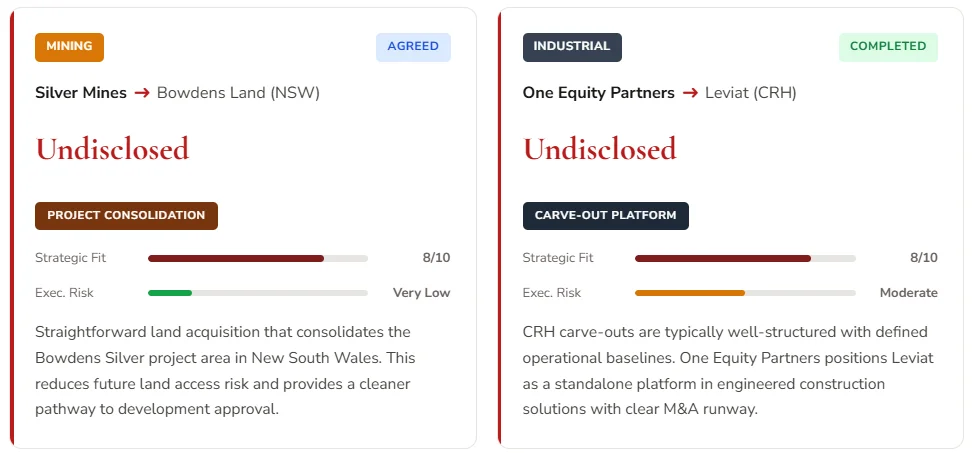

In the mining and energy space, several smaller transactions also advanced. Elcora signed a deal to acquire the South African Eldorado gold mine through a phased share purchase. Silver Mines agreed to buy adjacent freehold land in New South Wales, consolidating its Bowdens Silver project. Additionally, Drax added contracted renewable energy capacity to its portfolio. Natural resources continue to attract consistent M&A interest globally.

Pharma Bets on Rare Disease

Servier struck one of the most significant pharmaceutical deals of the year. The French company agreed to pay up to $2.65 billion for Edgewise Therapeutics’ muscular dystrophy programme, per PR Newswire. The central asset is sevasemten, a late-stage cardiac myosin inhibitor. This compound is currently progressing through Phase 3 clinical trials for Becker muscular dystrophy. Sevasemten represents a first-in-class mechanism for addressing the condition. No existing approved therapy currently targets this disease with a similar approach.

Rare disease drugs carry growing strategic value for pharmaceutical companies. Regulatory bodies, including the FDA, offer accelerated approval pathways for orphan designations. Moreover, these drugs command premium pricing due to their unmet need status. Through this acquisition, Servier significantly strengthens its rare neurology pipeline. This deal positions the company as a serious competitor in rare muscle disease medicine.

Capital Markets and Data Infrastructure

U.S. Bancorp completed its acquisition of BTIG, per Business Wire. The deal adds institutional equity sales, trading, electronic markets, and ECM advisory. It also brings M&A advisory capabilities into the bank’s expanding platform. U.S. Bancorp now competes more directly with full-service investment banks. This move reflects a broader industry trend. US regional banks are building capital markets capabilities to diversify their revenue base.

In the technology sector, Fivetran and dbt Labs completed an all-stock merger. Together, the combined entity now serves more than 100,000 data teams worldwide. This deal creates an end-to-end data pipeline and transformation platform. Consequently, the modern data stack now has a clear, well-capitalised, independent leader. Both companies held complementary positions in data infrastructure. Their combination creates significant competitive scale against cloud-native rivals.

Sponsor Activity: Building Platforms

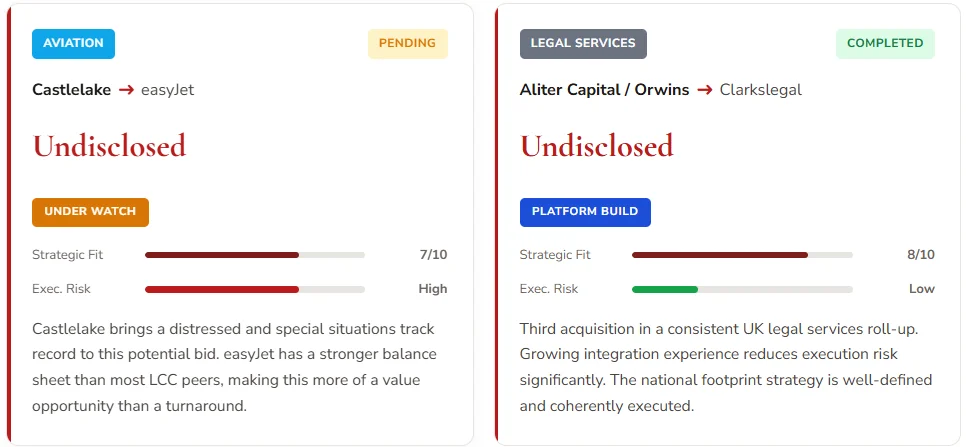

Private equity activity exhibited a strong, deliberate consolidation theme throughout the day. Astorg-backed Steliau acquired H2’s Acal BFI, the European electronic component distributor. This bolt-on adds meaningful scale to an existing sponsor-owned platform. Aliter Capital-backed Orwins completed its third law firm acquisition by purchasing Clarkslegal. Furthermore, One Equity Partners acquired Leviat, a global engineered solutions provider carved out from CRH.

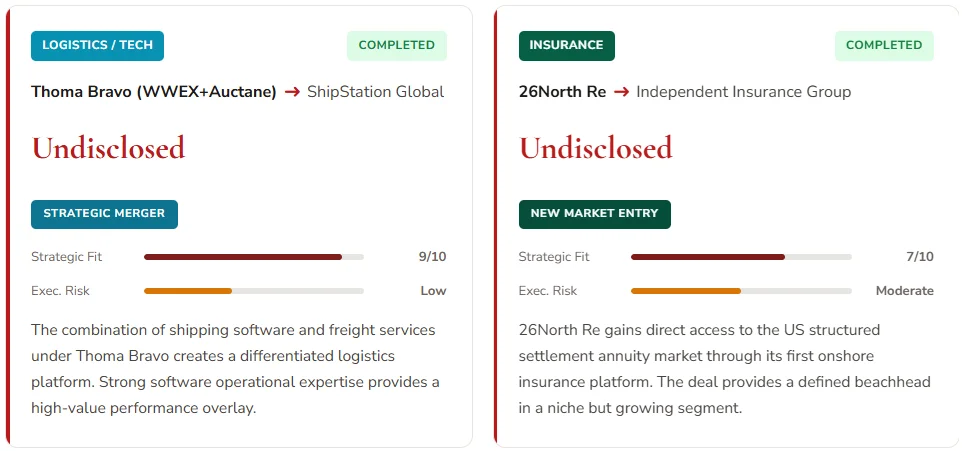

Thoma Bravo backed the formation of ShipStation Global via the merger of WWEX Group and Auctane. This new entity combines shipping software with freight services under one brand. Moreover, 26North Re acquired Independent Insurance Group, entering the US structured settlement annuity market. Together, these sponsor-backed transactions reflect a deliberate platform-building philosophy.

Each of these deals follows the same disciplined playbook. First, a sponsor secures a core asset with a clear investment thesis. Then, the platform adds adjacent bolt-on acquisitions to build meaningful scale. Finally, it expands into new customer segments and geographies. This approach reduces integration risk while compounding long-term value creation.

Analyst Note: Sponsor Playbook

Today’s sponsor activity confirms a consistent strategy: build a platform around a defined core asset, acquire adjacencies at speed, then expand addressable markets. This reduces execution risk compared to large transformative mergers.

What the Numbers Show

The disclosed deal values provide a clear picture of today’s activity. Berkshire’s $8.5 billion Taylor Morrison deal leads the leaderboard by a wide margin. ZIM’s blocked $4.2 billion transaction is the day’s second-largest by disclosed value. Veolia’s $3 billion Clean Earth deal ranks third in absolute terms. Servier’s $2.65 billion acquisition of Edgewise closes out the top four. Together, these four transactions account for more than $18 billion in disclosed value.

Sector diversity is equally notable. Financial services, logistics, and energy each contributed three deals. Healthcare and housing each added two deals. No single sector dominated the day’s activity. Therefore, this reflects a broadly active market rather than a sector-specific surge.

What to Watch Next

Castlelake is reportedly considering a potential bid for easyJet. A final decision is expected by June 26. If confirmed, this would add aviation to the day’s already diverse deal wave. Furthermore, sponsor activity in legal services, logistics, and data infrastructure shows no signs of slowing.

The broader takeaway is straightforward. Strategic capital is moving at scale and with clear conviction. Private equity firms are executing with discipline and a long-term platform logic. However, geopolitical risk is an emerging variable that dealmakers cannot ignore. Investors should closely monitor state intervention trends in cross-border infrastructure.

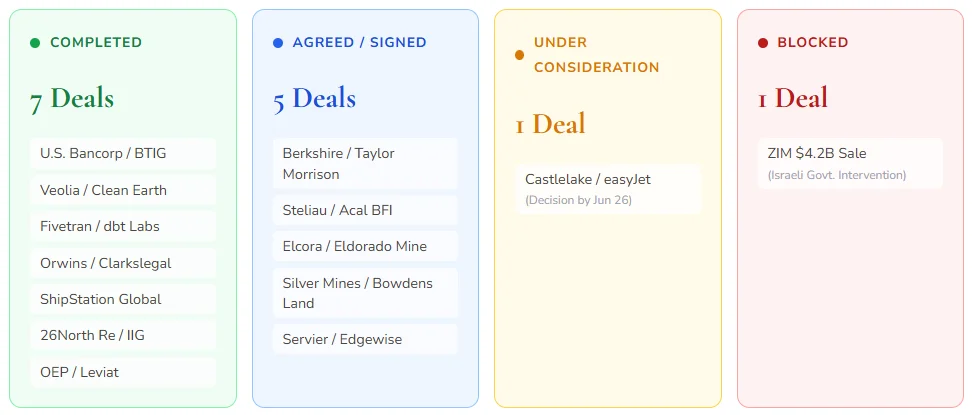

Deal Status at a Glance

All 14 transactions categorised by current deal status as of June 1, 2026