July 12, 2026 – Eight agents topped the classic balanced portfolio in simulation. The bank that built them is telling clients not to be impressed.

In Summary

JPMorgan built eight AI agents that shift between stocks and bonds. All eight beat the 60/40 portfolio on a risk-adjusted basis across roughly two decades of backtests.

The strongest agent added 0.7 percentage points per year, with smaller price swings. Sharpe ratios ranged from 0.74 to 0.95, against 0.61 for the benchmark.

The agents ran on off-the-shelf models from OpenAI and Anthropic, not a bespoke in-house market model. That lowers the cost of copying the approach.

The bank warned clients against trusting the result. No agent has managed real money, and backtests are prone to overfitting and look-ahead bias.

Supervisors in the UK and at the Financial Stability Board already flag AI-driven herding as a systemic risk if many firms converge on similar models.

JPMorgan AI agents outperformed the classic 60/40 portfolio across two decades of backtests. The bank’s cross-asset team built eight of them. Furthermore, all eight topped that benchmark on a risk-adjusted basis. Strategists led by Thomas Salopek shared the work in a July 9 client note.

Then the bank did something odd. It told clients not to trust the numbers. Salopek and his team warned against confident, in-sample answers from a machine. Back tests show what a strategy would have done. However, they say little about what it will do next.

The test still matters. After all, the asset mix is the core of what a fund manager sells.

How the JPMorgan AI agents make a call

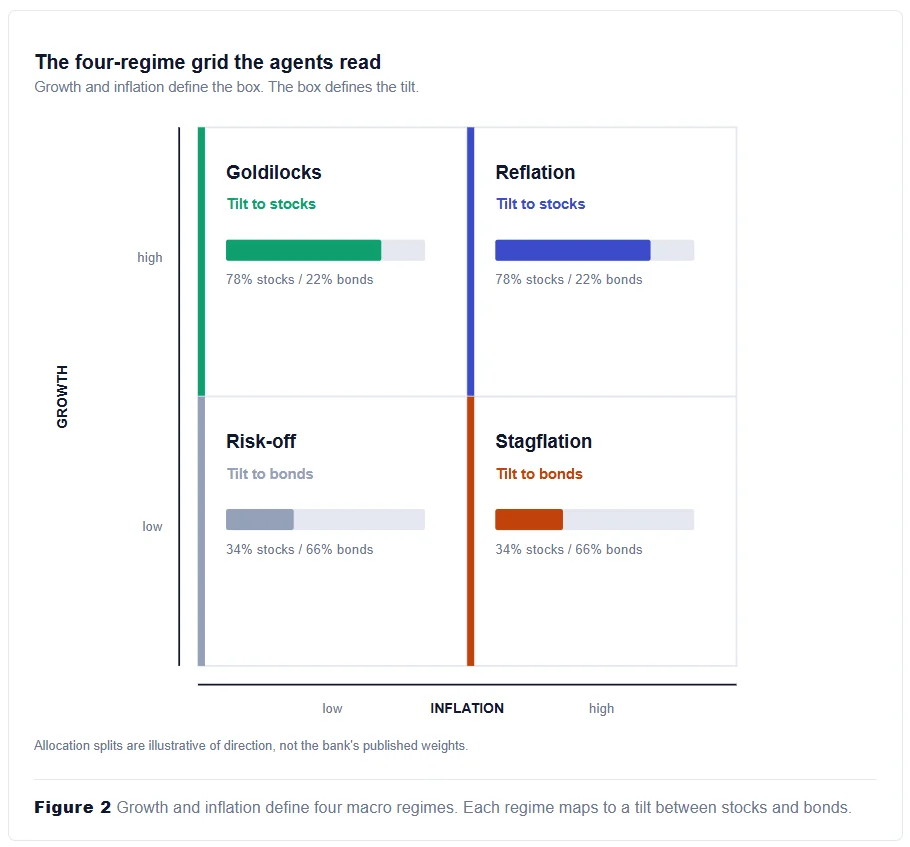

The design fits in one line. Each agent sorts the market into one of four macro regimes. Growth and inflation set the grid. Goldilocks, reflation, stagflation and risk-off fill the four boxes.

Next, the agent tilts the book. Strong growth pushes weight into stocks. Meanwhile, a weak outlook puts pressure on bonds. That logic mirrors what human allocators already do each quarter.

Notably, the JPMorgan AI agents ran on off-the-shelf models from OpenAI and Anthropic. The bank built no bespoke market brain. Instead, it wrapped general-purpose reasoning in a strict, rules-first process. That choice matters more than the headline score. Because the parts are cheap and shared, smaller firms can copy the trick.

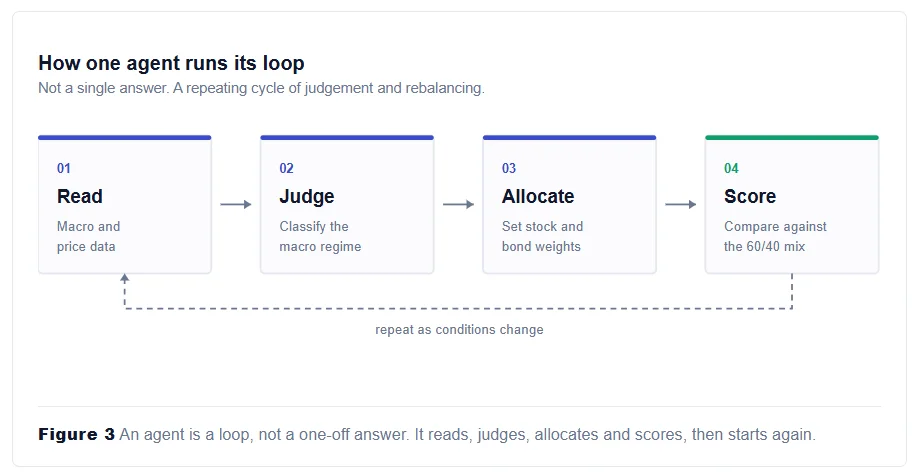

Here lies the real shift. An agent does not just answer a question. Rather, it runs a loop: read the data, judge the regime, set the weights, repeat.

The numbers behind the claim

The best agent beat the 60/40 mix by 0.7 percentage point a year. It also ran with smaller price swings. Sharpe ratios across the eight agents ranged from 0.74 to 0.95. By contrast, the 60/40 mix scored just 0.61 over the same span.

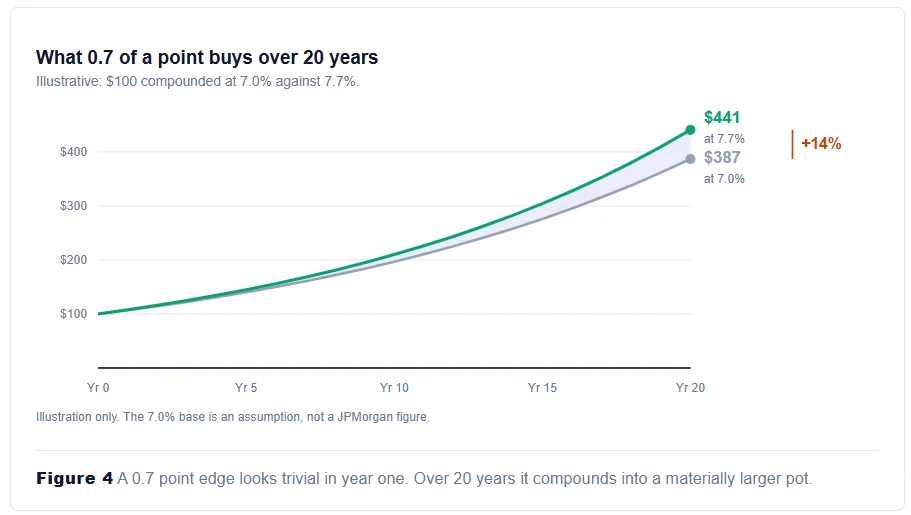

Such a gap looks small on paper. Yet compounding turns thin edges into wide ones. Take a 7% base return over 20 years. An extra 0.7 point then lifts the final pot by roughly 14%.

Crucially, the agents also beat JPMorgan’s own rules-based regime model. Therefore, the test cleared a real bar inside the bank. That older model already shapes live advice on where client money goes.

JPMorgan strategists described themselves as “wary to hand off asset allocation decision-making to an agent”.

-JPMorgan cross-asset strategy team, client note, 9 July 2026

Scale explains the stakes. JPMorgan closed 2025 with about $4.8 trillion under management. Even a tiny edge on that base moves real money.

Timing helps the pitch too. The 60/40 mix stumbled badly in 2022, when stocks and bonds fell as one. Since then, clients have asked for something smarter than a fixed split.

Why do back tests flatter machines

Paper gains come cheap. Researchers showed this more than ten years ago. Test enough setups, and one will shine through luck alone. They named the trap backtest overfitting.

Language models add a fresh twist. These systems learn from text that covers the test years. So an agent may simply recall that 2008 ended badly. Quants call this look-ahead bias, and it quietly puffs up scores.

Costs pose a second problem. Dynamic strategies churn far more than static ones. Spreads, slippage and taxes all bite. Real money also moves prices, while paper money never does. An edge of 0.7 points leaves thin cover for those frictions.

Watchdogs already see the risk

Supervisors spotted the trend early. The Bank of England’s Financial Policy Committee warned that AI-led investors may crowd into the same trades. Shared models plus shared data breed shared bets.

Herding looks like a skill in a calm market. During a selloff, though, it looks like a stampede. The Financial Stability Board reached much the same view. It flagged market correlations, model risk and third-party reliance as systemic weak spots.

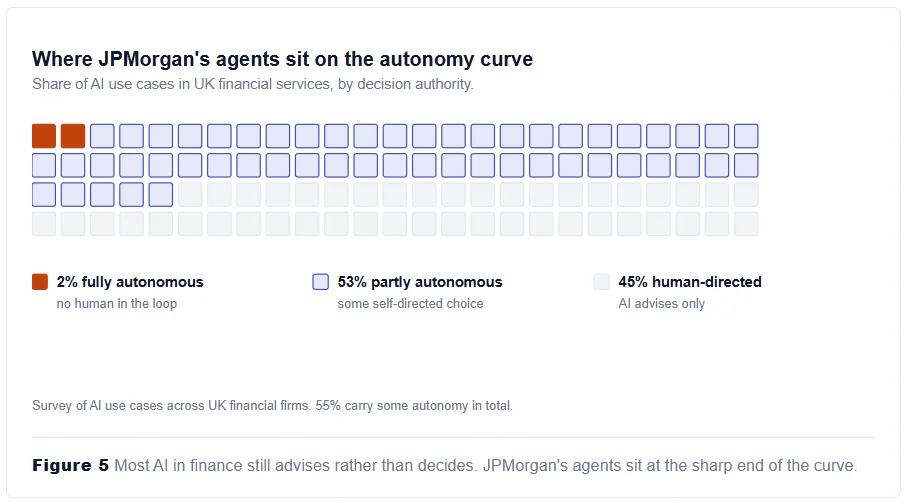

Uptake data sharpens the point. A survey by the Bank of England and the FCA found that 55% of AI use cases involve some self-directed choice. Only 2% run with no human in the loop. The JPMorgan AI agents sit at that thin edge.

The gap between the lab and the ledger

JPMorgan knows how to scale AI in-house. Its LLM Suite reached 200,000 staff within eight months of launch. Drafting and summing up, though, carry no market risk. Nobody loses a pension because a chatbot writes a clumsy line.

Asset mix works differently. One bad regime call costs clients hard cash. Salopek’s team put the tension plainly. They sound keen on agentic AI, yet wary of handing it the wheel.

Note the quiet detail in that stance. The bank shipped the research, not the product.

So the caution reads as the true finding. Eight JPMorgan AI agents cleared a tough benchmark in a test. None of them has ever run a dollar.

Investors should therefore watch one thing. Live, out-of-sample returns are the only proof that counts. Until a real track record lands, that 0.7-point edge stays a claim. For now, the 60/40 mix keeps its job.