April 18, 2026 – America’s $39 trillion tab is just the most visible symptom. The IMF’s spring Fiscal Monitor reveals a structural breakdown in world public finances and warns that AI may be the only path out.

In Summary

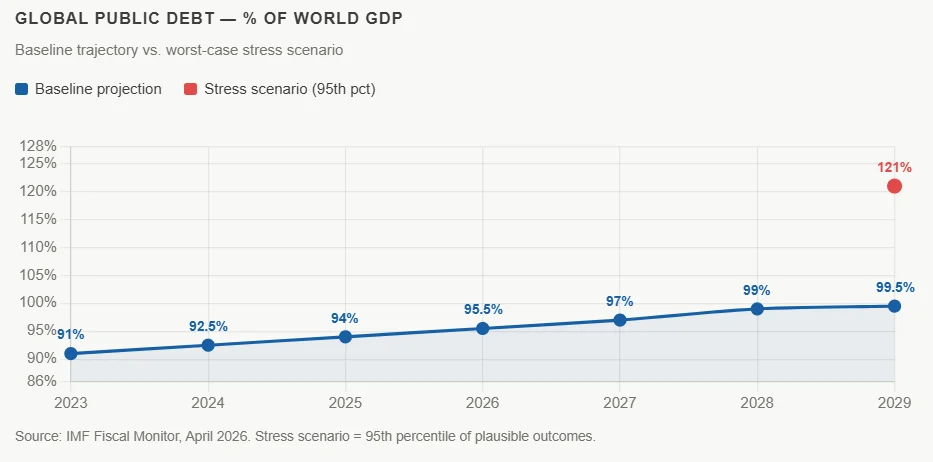

Global debt is nearing a historic threshold. The IMF projects world public debt will hit 99% of GDP by 2028. Worst-case stress scenarios put it at 121% within three years.

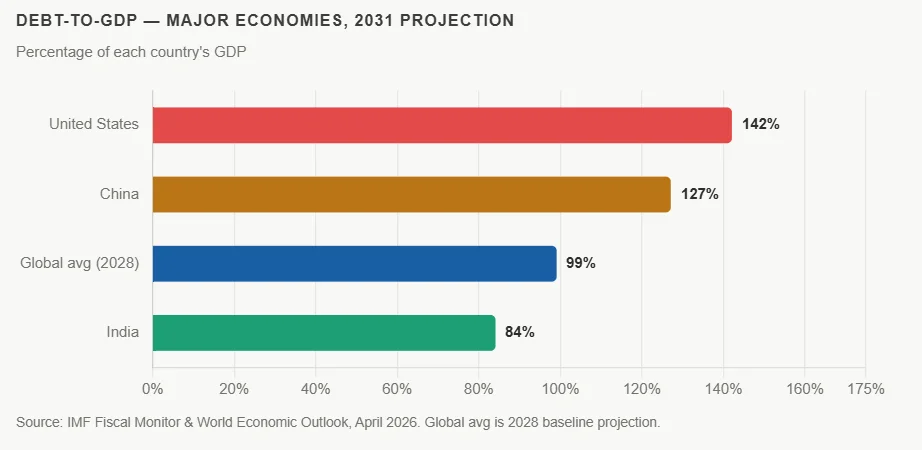

The US faces an extraordinary fiscal adjustment. With debt heading toward 142% of GDP by 2031, stabilizing the trajectory would require a 4 percentage-point of GDP tightening. Markets are already repricing US risk.

This is a structural problem, not a cyclical one. Real interest rates run 6 percentage points above pre-pandemic levels. Interest payments jumped from 2% to nearly 3% of global GDP in just four years.

Energy subsidies are the wrong response to the Middle East shock. The IMF warns that broad-based fuel subsidies are regressive and can, via spillover effects, double the original price shock globally.

AI is both a lifeline and a threat. It could boost government productivity, but risks hollowing out income and payroll tax bases. Governments must decide now whether their systems can adapt.

The International Monetary Fund issued its starkest fiscal warning in years. Crucially, global public debt is now on a collision course with 100% of world GDP. The window for orderly adjustment is closing fast.

At its spring 2026 meetings in Washington, the IMF projected global debt would hit 99% of global GDP by 2028, breaching the 100% threshold sooner than previously forecast. Under worst-case stress scenarios, the 95th percentile of plausible outcomes could spike to 121% within three years. Moreover, the IMF’s message was unambiguous: this is a structural breakdown, not a temporary blip.

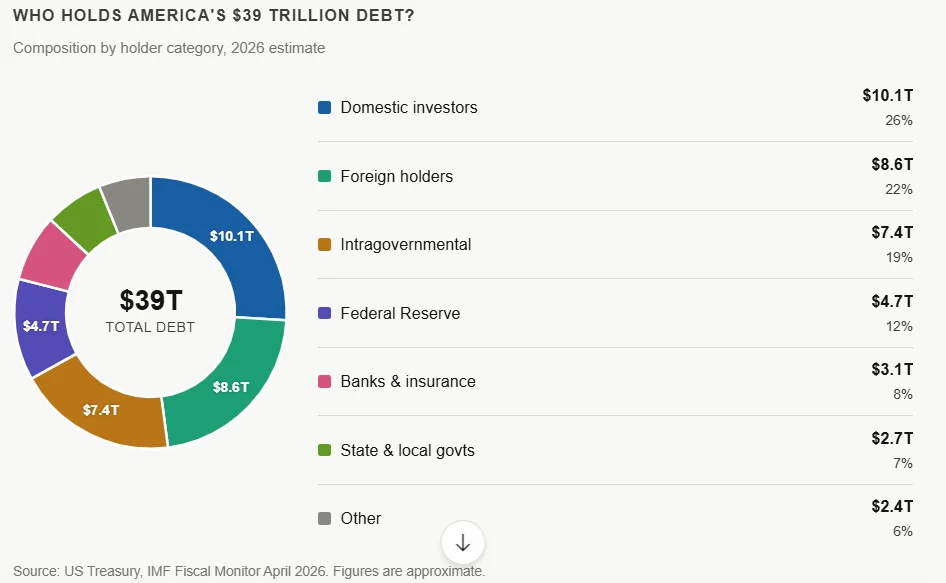

America’s $39 trillion burden

The United States remains the marquee example of fiscal dysfunction. America’s national debt has reached $39 trillion. Its deficit narrowed slightly last year, from nearly 8% of GDP to below 7%. However, that relief proved short-lived.

IMF Fiscal Affairs Director Rodrigo Valdez was direct: “Our forecast is that this deficit goes back to around 7.5% and stays there.” Consequently, US debt is on track to exceed 125% of GDP in 2026 and 142% by 2031. Stabilizing that trajectory would require fiscal tightening of 4 percentage points of GDP, one of the largest peacetime adjustments in modern history.

“This cannot wait forever.”

— Rodrigo Valdez, IMF Fiscal Affairs Director

Indeed, bond markets are already reflecting this anxiety. The premium US Treasuries once commanded over other advanced-economy debt is narrowing. As a result, markets are no longer as forgiving as they were even two years ago.

A global disease, not a US aberration

Nevertheless, Washington’s problem looks almost manageable against the full global picture. The IMF’s World Economic Outlook flags fiscal deficits worsening by about 2.6 percentage points of GDP during a typical defense-spending surge, and that trend is accelerating worldwide.

The fiscal gap, the distance between current primary balances and stabilization targets, has worsened by one percentage point compared to the five-year pre-COVID average. Additionally, real interest rates now run 6 percentage points above pre-pandemic levels, compounding the burden of every existing dollar of debt.

Furthermore, interest payments have surged from 2% to nearly 3% of global GDP in just four years. China’s debt, meanwhile, is projected to approach 127% of GDP by 2031. Consequently, every year of delay makes the eventual reckoning significantly worse.

Energy subsidies are making it worse

The ongoing Middle East conflict is adding a new fiscal trap. In response, many governments are reaching for broad-based energy subsidies and excise tax cuts. However, the IMF warns this is precisely the wrong tool, subsidies distort price signals, prove regressive in practice, and are nearly impossible to reverse once in place.

When half the world shields consumers from higher energy prices, the other half absorbs the entire demand shock. Therefore, IMF modeling suggests these spillover effects could double the original price shock for non-subsidizing countries. Instead, the fund prescribes targeted, temporary support for the most vulnerable, not blanket relief for everyone.

AI: the only wildcard left

In a briefing otherwise defined by grim arithmetic, artificial intelligence emerged as the closest thing to a lifeline. IMF Deputy Director Era Dabla-Norris argued that AI could boost productivity, tighten tax administration, and fundamentally reshape how governments deliver public services.

Yet AI is a double-edged sword. On one hand, it offers governments new tools to raise revenue efficiently. On the other hand, it concentrates wealth, disrupts labor markets, and risks hollowing out the very income and payroll tax bases on which modern welfare states depend.

Dabla-Norris posed the pivotal question: “Are our current tax systems and our current social protection systems fit for purpose?”

In short, with total global debt already above 235% of world GDP, the margin for error is razor-thin. Governments that delay will ultimately face far harder choices than those that act decisively today.