April 27, 2026 – Hong Kong is moving fast. Over $2 billion in tokenised bonds, new stablecoin licences, and a government-backed digital settlement platform signal a decisive shift, from pilot to policy.

In Summary

Hong Kong has issued over $2 billion in tokenised green and infrastructure bonds across multiple rounds.

Financial Secretary Paul Chan declared Web3, tokenisation, and AI as “building blocks of mainstream finance.”

The HKMA’s CMU OmniClear will build a dedicated digital bond settlement platform in 2026.

Hong Kong granted its first stablecoin licences to HSBC and a Standard Chartered-led consortium.

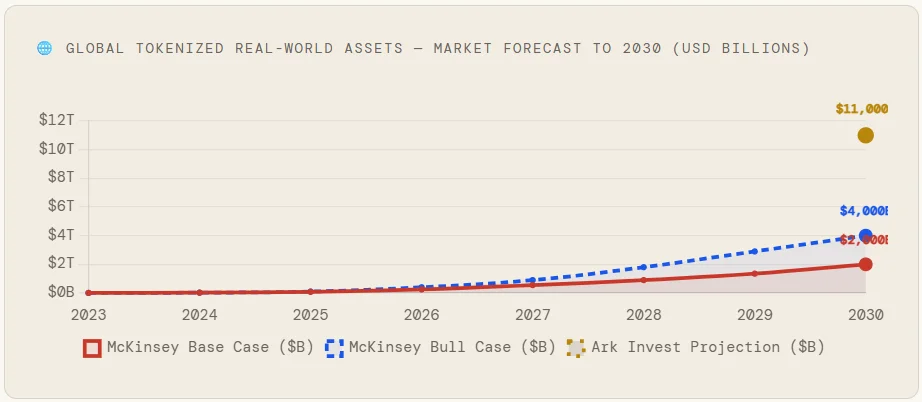

Global tokenised real-world assets could reach $2–$4 trillion by 2030, per McKinsey.

On April 20, 2026, Hong Kong sent a clear message to the world. Financial Secretary Paul Chan took the stage at the Hong Kong Web3 Festival 2026 and told a packed audience: ” Digital assets are no longer an experiment. They are infrastructure.

Chan’s remarks framed tokenisation and stablecoins as core financial tools. Specifically, he cited more than $2 billion in tokenised bonds already issued. New stablecoin licensing was also announced. Moreover, plans for a government-backed digital settlement platform were confirmed. Overall, the message was deliberate, data-backed, and unmistakably bullish.

From Pilot to Policy: The Bond Issuance Timeline

Hong Kong’s tokenised bond journey began in 2021. Notably, the HKMA launched Project Evergreen to test blockchain in capital markets. In collaboration with the BIS Innovation Hub, an initial proof of concept was completed. As a result, tokenisation was proven to be legally and operationally viable in Hong Kong.

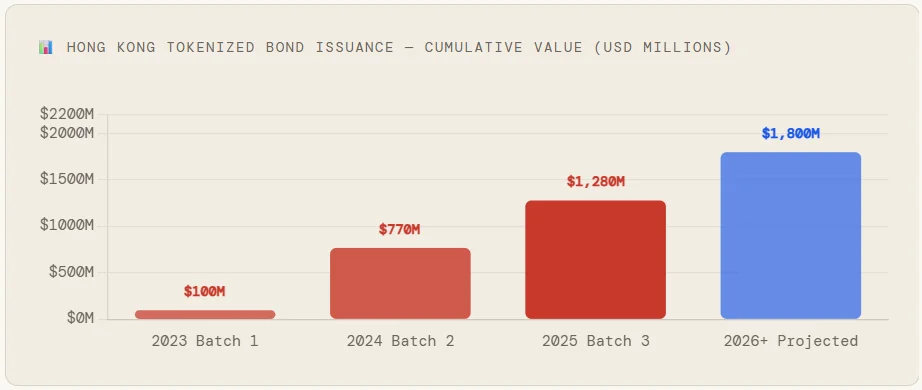

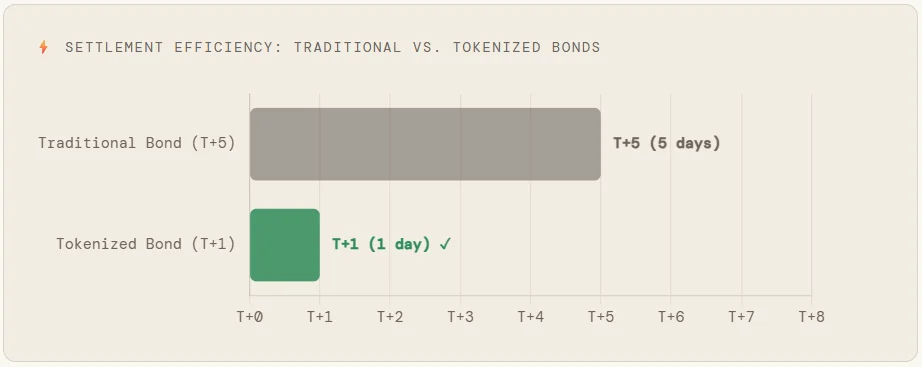

Real money followed quickly. In February 2023, the government issued the world’s first tokenised government green bond. Valued at HK$800 million, roughly US$100 million, the bond also delivered an immediate efficiency win. Specifically, the settlement cycle compressed from T+5 to T+1 on the very first attempt.

The second issuance, in February 2024, was far more ambitious. That offering became the world’s first multi-currency digital bond, raising approximately HK$6 billion. Furthermore, the transaction spanned four currencies: HKD, RMB, USD, and EUR. Global asset managers, banks, insurers, and private banks all participated.

Subsequently, the third batch, issued in Q4 2025, set a new global record. At HK$10 billion (roughly US$1.28 billion), the offering surpassed every prior digital bond. Chan confirmed this programme will now be issued on a regular, ongoing basis. In effect, Hong Kong has industrialised tokenised bond issuance.

Why Tokenisation Matters: The Efficiency Case

The numbers tell a compelling story. Traditional bond settlement in Hong Kong takes up to five business days (T+5). By contrast, tokenised bonds on distributed ledger infrastructure settle in just one day (T+1). That single improvement consequently reduces counterparty risk across the entire transaction chain.

According to the South China Morning Post, the HKMA has also launched a three-year Digital Bond Grant Scheme. Each qualifying issuance receives up to HK$2.5 million in subsidies. Therefore, the grant directly reduces barriers for first-time tokenised bond issuers. Ultimately, lower costs widen market participation; that’s the core design logic.

Fractional ownership is another key benefit. Because tokenised bonds can be divided into smaller units, mid-market investors gain access. Previously, these assets were reserved almost exclusively for large institutions. As a result, broader participation deepens market liquidity and reduces overall volatility.

The Platform Play: CMU OmniClear and Digital Infrastructure

Chan’s Web3 Festival speech built on announcements made in the 2026–27 Budget. Crucially, the HKMA’s subsidiary CMU OmniClear Holdings will develop a dedicated digital asset platform. Both issuance and settlement of tokenised bonds will be handled through this system. In addition, the platform will be interoperable with regional tokenisation networks.

This is not, however, a standalone pilot. Rather, it represents a structural upgrade of Hong Kong’s post-trade financial infrastructure. CMU OmniClear’s platform will initially focus on tokenised government bonds. Over time, the scope will then expand to include other digital asset classes.

The platform’s cross-border connectivity is also strategically significant. Hong Kong is thus positioned as a settlement hub for tokenised assets across Asia. Combined with Bond Connect access and offshore RMB capabilities, this creates considerable scale. Few jurisdictions can match Hong Kong’s combination of legal clarity and market depth.

Stablecoin Licensing: Completing the Digital Finance Stack

Tokenised bonds need a payment leg. That’s precisely where stablecoins enter the picture. Chan confirmed Hong Kong has now issued its first stablecoin licences. Recipients include HSBC and a Standard Chartered-led consortium.

Licensed stablecoin issuers can consequently operate in a compliant, risk-controlled manner. Meanwhile, the SFC has also enabled margin financing for licensed virtual asset brokers. The initial collateral framework covers Bitcoin and Ether. Together, these measures create the building blocks of a regulated on-chain economy.

The Hong Kong Securities and Futures Commission has gone even further. For instance, a framework allowing licensed platforms to offer leveraged perpetual contracts was published. Each step, therefore, expands the regulated surface area of digital finance. Overall, the policy direction is explicit: controlled expansion, not restriction.

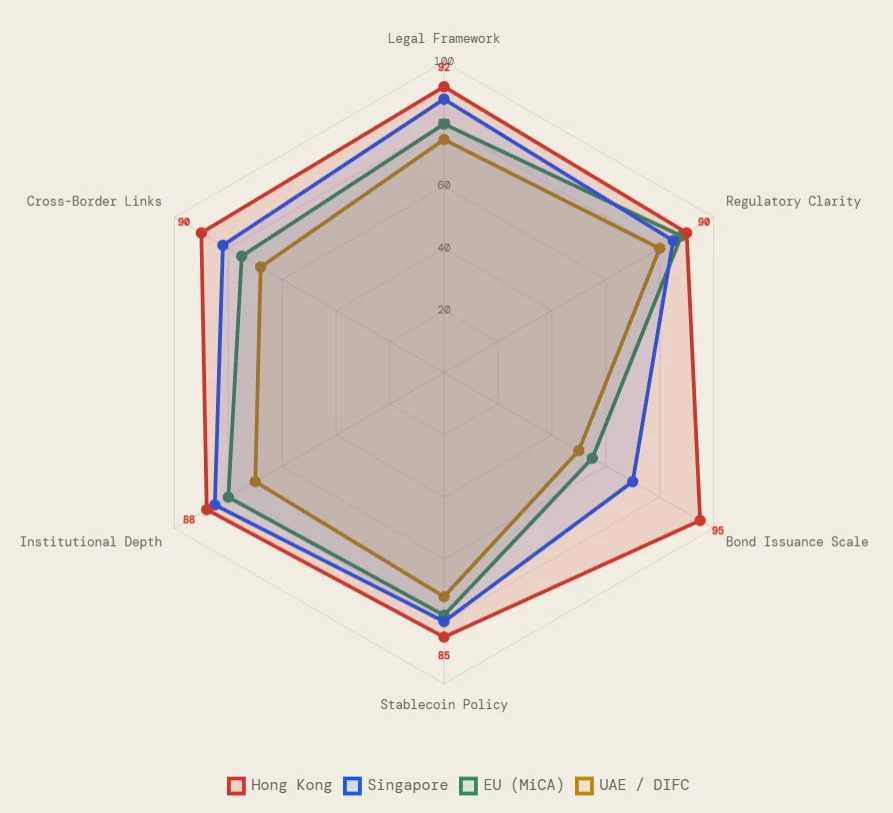

The Global Race: Where Does Hong Kong Stand?

Hong Kong is not alone in pursuing tokenisation. Singapore’s MAS, Switzerland’s FINMA, and the EU’s MiCA framework are all active. Nevertheless, Hong Kong has moved faster and on a larger scale on government bond tokenisation. Indeed, the record HK$10 billion bond issuance in 2025 remains the world’s largest.

The global prize is enormous. Ark Invest projects that tokenised assets could surpass $11 trillion by 2030. McKinsey’s more conservative estimate, however, places the figure at $2–4 trillion. Even so, the lower bound implies a 90-fold increase from today’s $24 billion market. Every jurisdiction establishing infrastructure now is consequently building a long-term competitive advantage.

Hong Kong’s primary advantage is its combination of legal certainty and institutional depth. A common law framework accommodates tokenised securities without requiring new legislation. Proximity to mainland China also opens the offshore RMB and Bond Connect pipeline. Above all, the financial regulator has demonstrated a willingness to approve, not just consult.

Bottom Line

Hong Kong is making a calculated bet on regulated digital finance. Already, it has backed the bet with real capital, real issuances, and real infrastructure. The $2 billion tokenised bond programme serves as the proof point. Furthermore, the CMU OmniClear platform will provide the delivery mechanism. And stablecoin licences, finally, complete the transactional layer.

Whether the city can sustain this momentum ultimately depends on execution. Cross-border interoperability must work at scale. Secondary market liquidity also needs to deepen. Additionally, global institutional confidence must continue to build over time.

For now, Hong Kong has done what few jurisdictions dare: put government credibility behind a technology still finding its feet. That commitment, more than any single bond issuance, is therefore what makes the Web3 Festival speech truly consequential.