Table of Contents

- Table of contents will be generated automatically when the page loads.

In Summary

Private credit is non-bank lending negotiated directly between lenders and borrowers. It fills the financing gap left by post-2008 banking regulations.

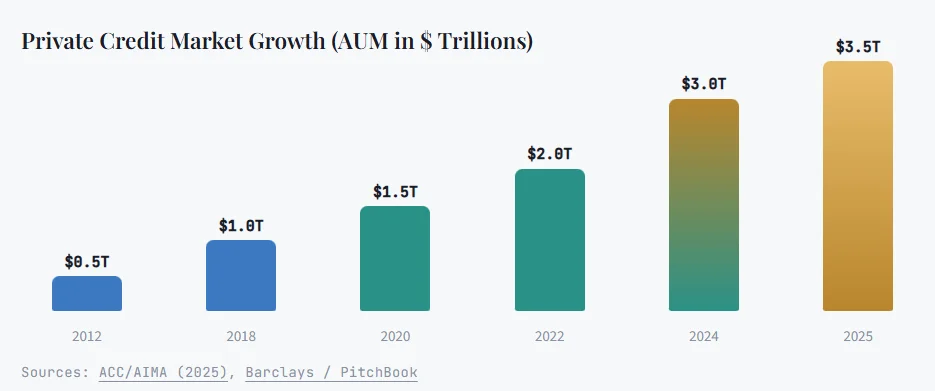

The global market has reached $3.5 trillion in AUM and is projected to hit $5 trillion by 2029 (Morgan Stanley).

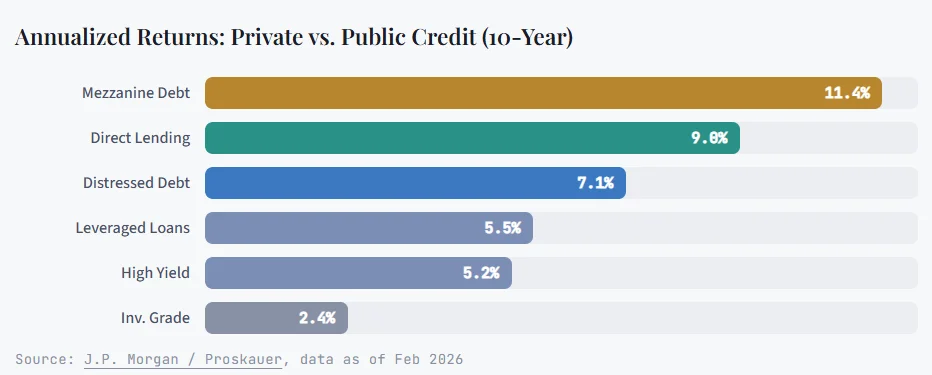

Direct lending has delivered 9.0% annualized returns over 10 years, nearly double investment-grade bonds (J.P. Morgan).

94% of institutional investors now allocate to private credit, and retail access is expanding through ELTIF 2.0 in Europe and potential inclusion in U.S. 401(k) plans.

The market is going global: Europe captured 35% of fundraising in 2025, while Asia-Pacific is growing at a 20% CAGR (With Intelligence).

AI infrastructure, healthcare, and specialty finance are emerging as the hottest sectors for private credit deployment in 2026.

Key risks include illiquidity, valuation opacity, portfolio concentration, and post-default recovery rates that may lag those in public markets.

Asset-based finance and credit secondaries are the fastest-growing sub-strategies, potentially rivaling direct lending in the long term.

Private credit has quietly become one of the largest forces in global finance. Here’s what every investor needs to know in plain English.

Imagine you run a mid-size business. You need a loan, but banks turn you down. Their hands are tied by strict regulations. So who do you turn to? Increasingly, the answer is private credit, and it’s reshaping how money flows around the world.

What Is Private Credit?

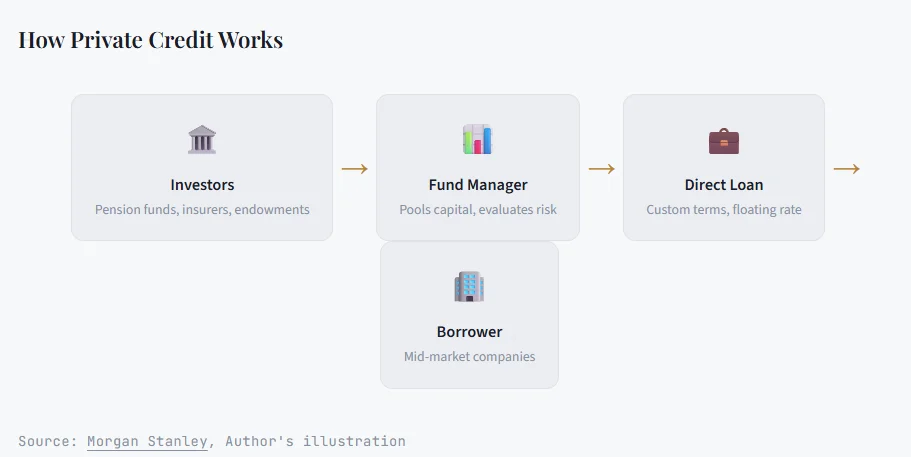

Private credit is lending that happens outside traditional banks. Instead of going through public markets or a bank, borrowers deal directly with specialized lenders, such as investment firms, pension funds, or insurance companies. The loans are privately negotiated, not traded on stock exchanges, and tailored to the borrower’s needs.

Think of it as a handshake deal rather than a mass-produced contract. The lender offers speed and flexibility. The borrower gets capital that banks won’t provide. In return, investors earn higher yields for taking on less liquidity.

Why Has It Exploded?

After the 2008 financial crisis, tighter rules (known as Basel III) forced banks to hold more reserves and lend less, especially to mid-sized firms. Private credit stepped into that gap. The market has grown from under $500 billion in 2012 to $3.5 trillion in AUM by late 2025, according to research from the Alternative Credit Council (ACC).

Capital deployment surged to $592.8 billion in 2024, a 78% jump from 2023. Morgan Stanley projects the market could reach $5 trillion by 2029. The growth isn’t just an American story either. Europe now accounts for nearly 30% of global private credit assets.

How Does It Compare to Public Credit?

The big draw is yield. According to J.P. Morgan data (as of February 2026), direct lending returned an annualised 9.0% over the past decade, compared to 5.2% for high-yield bonds and just 2.4% for investment-grade corporate debt. That premium compensates investors for giving up liquidity.

BlackRock notes that over the past decade, the average yield premium of private credit over public loans has been about 4.2%. However, that gap has narrowed recently as competition among lenders intensifies.

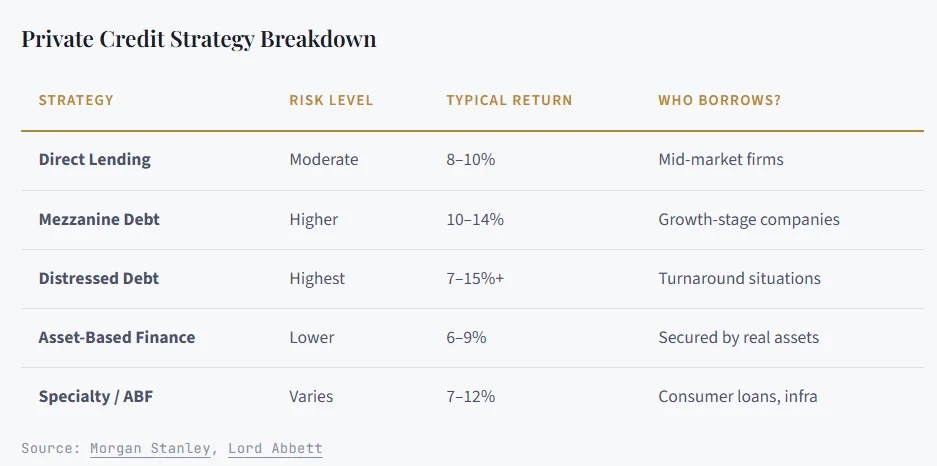

Key Strategies Within Private Credit

Direct lending, where a fund lends directly to a company, remains the dominant strategy. However, asset-based finance is growing quickly and could rival direct lending in the long run. Credit secondaries and capital solutions funds are also scaling fast.

The Global Landscape

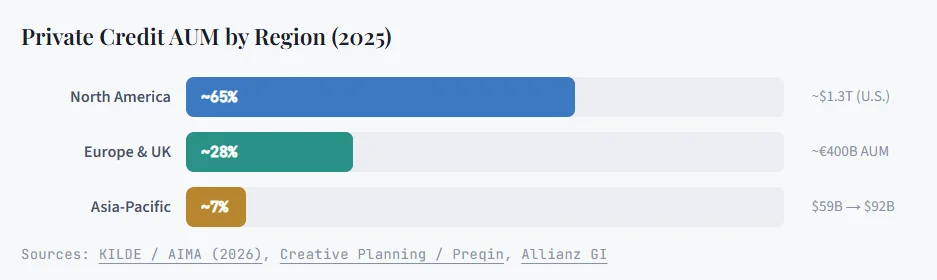

Private credit is no longer just a U.S. story. The United States still dominates, holding roughly 65% of global AUM. But Europe and the Asia-Pacific are catching up fast. In the first nine months of 2025, European funds captured 35% of all private debt fundraising, up from 24% the year before. Many analysts see this as a lasting structural shift, not a one-off spike.

Europe’s appeal comes down to one word: opportunity. Bank lending remains more dominant there than in the U.S., which means deeper room for private credit to grow. European deals also offer a premium of over 200 basis points above public markets, according to Allianz Global Investors. Meanwhile, the Asia-Pacific region spanning over 50 jurisdictions is projected to grow at a 20% compound annual growth rate, with India, Australia, and Singapore leading the charge.

Why Asia-Pacific is different: About 90% of APAC private credit deals involve borrowers without private equity backing. The focus is on underbanked small and mid-market businesses, a fundamentally different market structure from the sponsor-heavy U.S. model. (ACC/AIMA)

Who Invests and Who’s Next?

Historically, private credit was the domain of large institutions. Pension funds, insurance companies, endowments, and sovereign wealth funds have been the primary sources of capital. According to a 2025 Nuveen survey, 94% of institutional investors now have private credit in their portfolios. The appeal is clear: higher yields, lower volatility than public bonds, and meaningful diversification.

But the investor base is broadening. Retail participation, particularly from high-net-worth individuals, has grown notably. In Europe, the revised ELTIF 2.0 framework has opened the door to semi-liquid private credit funds now managing over €20 billion. In the U.S., an executive order signed in 2025 initiated regulatory work to allow private credit in 401(k) retirement plans, a move that could unlock a $12 trillion market.

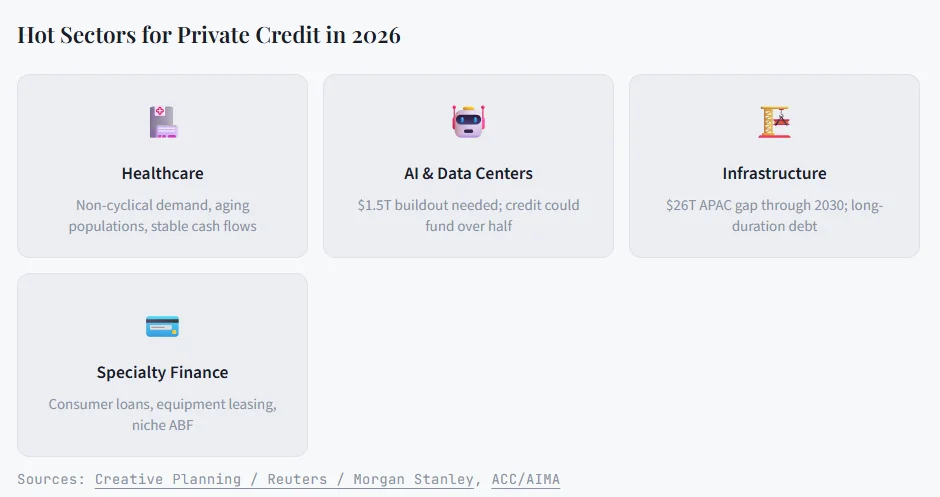

Sectors Driving Growth in 2026

As the U.S. market matures, lenders are specializing. They’re targeting sectors with recurring revenue, long-term tailwinds, and strong cash flows. Three areas stand out heading into 2026.

The AI boom is perhaps the most striking catalyst. According to a Reuters analysis cited by Creative Planning, Morgan Stanley estimates private credit could supply more than half of the $1.5 trillion needed for global data center construction through 2028. UBS data show AI-related private credit loans nearly doubled over the 12 months through early 2025.

What Are the Risks?

Private credit is not risk-free. The headline default rate has stayed below 2% for years. But once selective defaults and restructuring exercises are counted, the effective rate approaches 5%. Loans are illiquid; you can’t sell them on a whim. And as more capital chases fewer deals, underwriting standards may loosen, which is a concern flagged by multiple industry experts.

Investors also face valuation opacity. Unlike public bonds, private loans lack daily market pricing. Returns depend on third-party appraisals, which can lag reality during downturns. A Federal Reserve study found that post-default recovery values for direct loans averaged about 33 cents on the dollar, lower than the 52 cents on the dollar for syndicated loans. So while private credit controls distress earlier and more closely, the losses can be steeper when things actually break.

There’s also a concentration risk. As the market grows, investors across multiple funds may unknowingly become exposed to the same large borrowers. CNBC reports that with limited mega-deals available, portfolio overlap is becoming a real concern, undermining the diversification that investors sought in the first place.

The Bottom Line

Private credit isn’t a fad. It has evolved from a niche alternative into a pillar of modern finance. For investors willing to trade liquidity for yield, it offers a compelling proposition. But as the McKinsey Global Private Markets Report 2026 warns, the easy era is over. Success in this market now depends on discipline, selectivity, and deep due diligence.

The asset class is also entering its first real stress test. High-profile defaults in late 2025, rising payment-in-kind usage, and tighter spreads all signal that the market is maturing rapidly. As Ares Management puts it, private credit is designed to be a defensive strategy that can thrive even under challenging conditions. But only for investors who understand its mechanics.

Whether you’re an institutional allocator, a financial student, or simply curious about where the world’s money flows, understanding private credit puts you ahead of most market participants. The ecosystem is large, complex, and still growing. Getting comfortable with the basics today is the smartest investment you can make.