March 11, 2026 – UK gilts surge as Axios reports a US-Iran peace memo is close. Oil falls sharply. Inflation bets ease. Rate hike expectations across major economies are trimmed.

In Summary

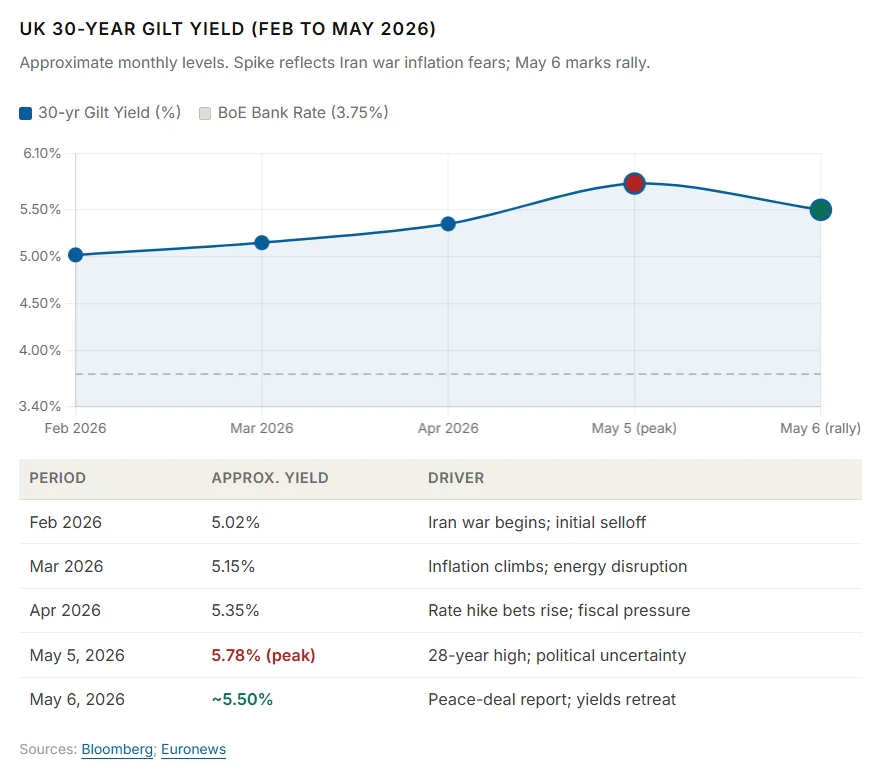

UK 30-year gilt yield peaked at 5.78%, its highest since 1998, before retreating sharply.

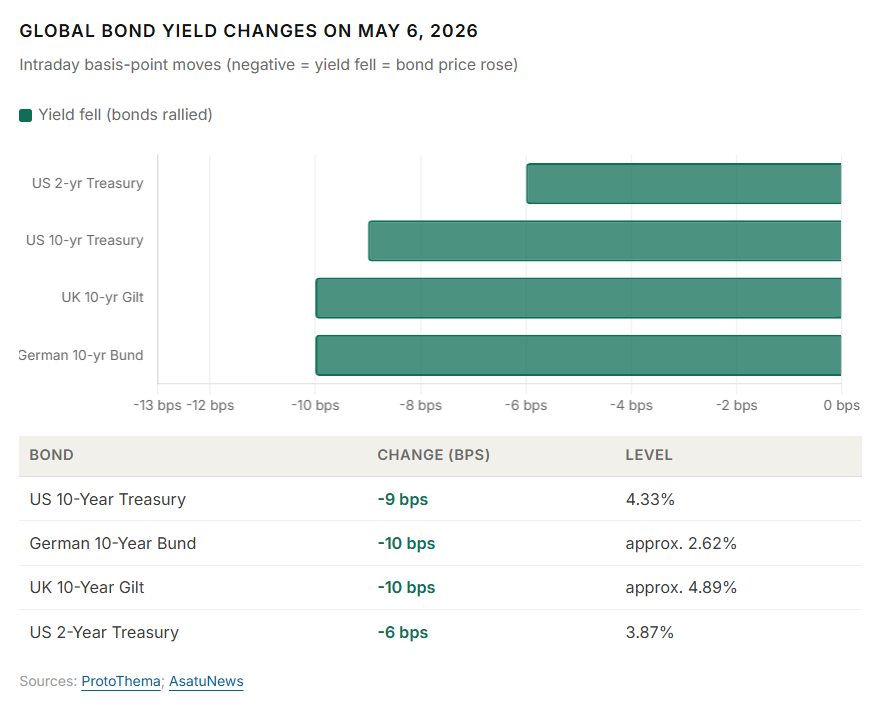

US 10-year Treasury yield fell as much as 9 basis points to 4.33% on May 6.

German 10-year Bund yield dropped approximately 10 basis points intraday.

Oil price declines eased fears of persistent inflation above target.

Markets cut bets on 2-3 Bank of England rate hikes by end-2026.

Global bond markets staged a powerful rally on May 6, 2026. The catalyst was an Axios report. It said the United States and Iran are nearing a one-page memorandum to end their two-month war. This prospect sent oil prices sharply lower. Lower energy costs ease inflation fears. That reduces pressure on central banks to raise interest rates.

UK Gilts Led the Charge

UK 30-year gilt yields surged to 5.78% on May 5, the highest level since 1998. That spike followed weeks of selling tied to the war in Iran. On May 6, peace-deal optimism reversed the move. Long-bond yields retreated from that 28-year peak.

The UK is more exposed than most European peers to energy shocks. It relies heavily on imported energy. A surge in oil prices hits British consumers and businesses directly. It also pushes inflation higher and slows economic growth simultaneously. This dual risk has amplified every yield spike since the Iran conflict began.

A Coordinated Global Move

The rally was not limited to UK gilts. It swept across bond markets worldwide. US 10-year Treasury yields fell as much as 9 basis points to 4.33%. German 10-year Bund yields dropped around 10 basis points. UK 10-year gilt yields, which had topped 5.10% days earlier, also fell sharply. The move showed how deeply geopolitical risk is now embedded in bond pricing.

The 2-year US Treasury yield also rallied. It fell by more than 6 basis points to 3.872%. Shorter-dated bonds are more sensitive to near-term rate decisions. Their movement showed traders rapidly unwinding tightening bets.

The Oil-Inflation Connection

Iran is one of the world’s largest oil producers. It pumps approximately 3 million barrels per day. That equals around 3% of global crude output. A peace deal would ease supply disruptions in the Persian Gulf. It would also remove the threat to the Strait of Hormuz shipping lane. Both factors would put downward pressure on global energy prices.

For the UK, this matters enormously. UK CPI reached 3.3% in March 2026, well above the Bank of England’s 2% target. Energy costs drove a large share of that overshoot. Sustained declines in oil prices could accelerate the return to the target. That would give the BoE less reason to raise rates further.

“If the conflict is resolved before the next Bank of England meeting, I believe the central bank may adopt a wait-and-see stance throughout 2026.”

Fixed income manager, Santander Asset Management (via ProtoThema)

Rate Hike Bets Scale Back

Before May 6, markets were pricing in aggressive tightening. Traders expected two to three Bank of England rate hikes by the end of 2026. The BoE held Bank Rate at 3.75% on April 30. The vote was 8-1 to hold rates steady. Chief economist Huw Pill dissented, voting to raise it to 4%.

The Federal Reserve also saw its rate-hike pricing trimmed on May 6. Traders briefly priced in a chance of a Fed cut, reversing tightening bets entirely. The European Central Bank saw similar downward pressure on rate expectations. Peace hopes, even unconfirmed ones, can move markets fast.

US Jobs Data Reinforced the Move

Bond-friendly US labour data added further fuel to the rally. The ADP National Employment Report showed 109,000 private-sector jobs added in April. That fell short of market expectations. Softer job growth reduces inflationary pressure. It also gives the Federal Reserve more room to hold rates steady. The combination of geopolitics and weak data made for a powerful bond tailwind.

What Analysts Are Saying

Strategists at Toronto Dominion Bank recommended buying 10-year gilts. They said most of the election risk had already been priced in. A short-term position in gilts, they argued, offered protection against political noise.

Thomas Pugh, chief economist at RSM UK, offered a note of caution. He said gilt yields could rise again if a new Labour leader increased spending plans. Political risk in the UK remains a background factor.

Risks Remain

Caution: The Axios report has not been confirmed by either government. Iran’s foreign ministry said it was “evaluating” the US peace proposal. The US has suspended “Project Freedom,” a military escort operation in the Strait of Hormuz. That suspension added to optimism. But a deal is not yet signed.

Markets remain highly sensitive to any reversal. A breakdown in talks would likely push oil prices sharply higher. Gilt yields would follow, with Treasury yields. Inflation expectations would re-accelerate. Rate hike bets would return. The gains of May 6 could unwind just as quickly as they arrived.

Bottom Line

May 6 was a day of relief for fixed-income investors. Peace hopes drove a coordinated global bond rally. UK gilts, US Treasuries, and German Bunds all gained. Rate hike bets fell across the world’s major central banks. The oil-inflation link remains the key variable to watch. If a US-Iran peace deal materialises, the path for global bonds in 2026 could look very different.