July 18, 2026 – The GenAI funding slowdown intensified in Q2 2026. Yet the decline masks a deeper shift toward concentrated capital and public listings.

In Summary

Application companies raised about $70 billion across 18 deals during Q2 2026.

Anthropic captured roughly 93% of that quarter’s reported funding.

First-half funding reached $217.7 billion, nearly twice the full-year 2025 total.

Public listings could finance compute, acquisitions, and employee liquidity at a greater scale.

A sharp fall after an exceptional quarter

The GenAI funding slowdown looks severe because the comparison period was unusually strong. Application companies secured about $70 billion across 18 second-quarter deals.

That total fell approximately 53% from an estimated $147.7 billion during Q1. The estimate subtracts Q2 funding from the reported first-half total.

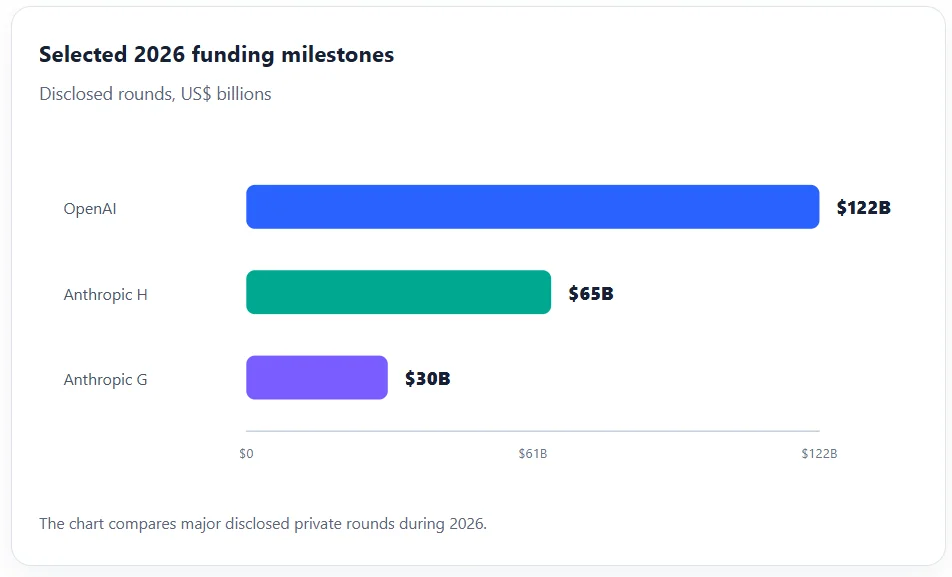

OpenAI closed $122 billion in committed capital during March. The round valued the company at $852 billion after the investment.

That single transaction dominated the first quarter. Therefore, Q2 represents normalisation after a megadeal, rather than a broad investor retreat.

Still, deal activity remained narrow. Eighteen transactions cannot support the growing number of companies seeking expensive compute and specialised talent.

Capital concentration reaches a new extreme

Anthropic raised $65 billion in May at a $965 billion post-money valuation. The company also reported run-rate revenue above $47 billion.

Its round represented about 92.9% of Q2 application funding. That left only $5 billion for the other 17 reported deals.

An even distribution would equal about $294 million per remaining transaction. Actual funding likely varied widely across those companies.

This concentration changes how investors should read the headline total. Strong aggregate funding does not prove healthy access across the sector.

Instead, capital now favours companies with leading models, enterprise distribution, and long-term infrastructure agreements. Smaller developers face tougher proof requirements.

Anthropic’s valuation equalled about 20.5 times its reported revenue run rate. That multiple assumes fast growth and stronger operating leverage.

However, compute spending could delay that leverage. Model training, inference, power, networking, and data-centre contracts remain highly capital-intensive.

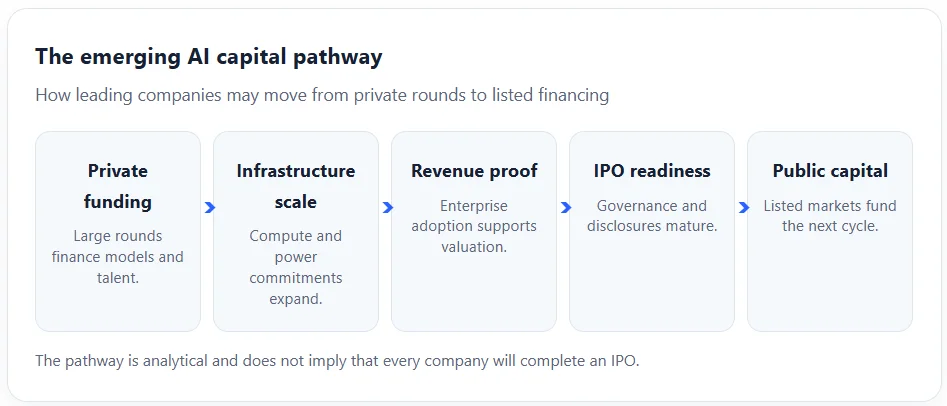

Public markets become the next funding channel

The private market may struggle to fund repeated rounds of this size. Public markets offer deeper liquidity and broader ownership.

Anthropic confidentially submitted a draft S-1 registration statement in June. The filing gives the company flexibility to pursue an offering.

A separate public S-1 from SpaceX shows another capital-heavy technology group testing listed markets. That direction matters for AI-linked assets.

Public listings can provide four advantages. They create acquisition currency, employee liquidity, access to debt, and continuous price discovery.

Yet those benefits come with stricter disclosure. Investors will examine margins, customer concentration, related-party agreements, and infrastructure commitments.

Quarterly reporting may also expose volatile spending patterns. Private valuations can absorb uncertainty more quietly than listed shares.

Therefore, public-market readiness depends on financial controls, governance, and predictable revenue. Technical leadership alone will not guarantee support.

Revenue growth supports the funding case

The largest rounds are not based only on future promises. Both leading developers reported substantial commercial traction.

OpenAI said revenue had reached $2 billion monthly. It also said enterprise activity generated more than 40% of revenue.

Anthropic reported a revenue run rate above $47 billion. Enterprise coding and workflow products remain central to that expansion.

These figures suggest businesses are paying for measurable productivity. Coding, research, customer service, and automation drive repeat usage.

However, revenue quality matters more than headline growth. Investors need retention, contract duration, gross margin, and customer diversification.

Heavy users may account for a large share of consumption. That creates upside, but it also creates concentration risk.

Pricing pressure could also increase. Open-source models continue improving, while cloud providers package competing tools into existing contracts.

As a result, model companies must defend differentiation. They can compete through accuracy, safety, distribution, workflow integration, and lower unit costs.

What investors should watch next

The first test will be public offering performance. Strong demand could validate private valuations and reopen the technology listing pipeline.

Weak debuts would produce the opposite effect. Private investors could demand lower entry prices and stronger protection.

Second, investors should compare revenue growth against infrastructure spending. Rapid sales growth can still destroy value when serving costs remain high.

Third, market participants should track funding outside frontier models. Application companies need capital to build distribution and proprietary customer data.

Finally, regulators will influence timing. Disclosure reviews, governance standards, and national-security concerns could complicate large offerings.

The market is rotating, not retreating

First-half application funding reached $217.7 billion. That amount was roughly double the entire 2025 total.

Yet Q2 depended heavily on one company. The combination reveals a market with abundant capital and limited breadth.

The GenAI funding slowdown therefore signals a transition. Venture rounds are giving way to public financing, strategic partnerships, and consolidation.

Successful listings could widen access to AI growth. They could also transfer valuation and execution risk to public shareholders.

For investors, the central question has changed. Capital availability matters less than capital efficiency, durable revenue, and credible paths to profit.