June 15, 2026 – Industry leaders say drained inventories could push pump prices sharply higher this summer. The White House disagrees.

In Summary

Oil executives warn that global inventories are nearing “tank bottom” levels.

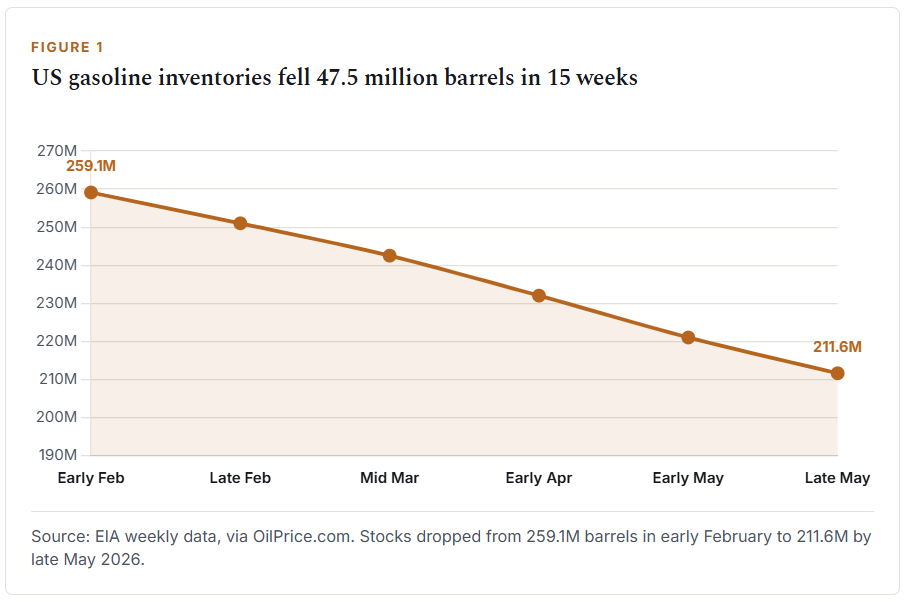

US gasoline stocks fell 47.5 million barrels, the steepest such drop since 1990.

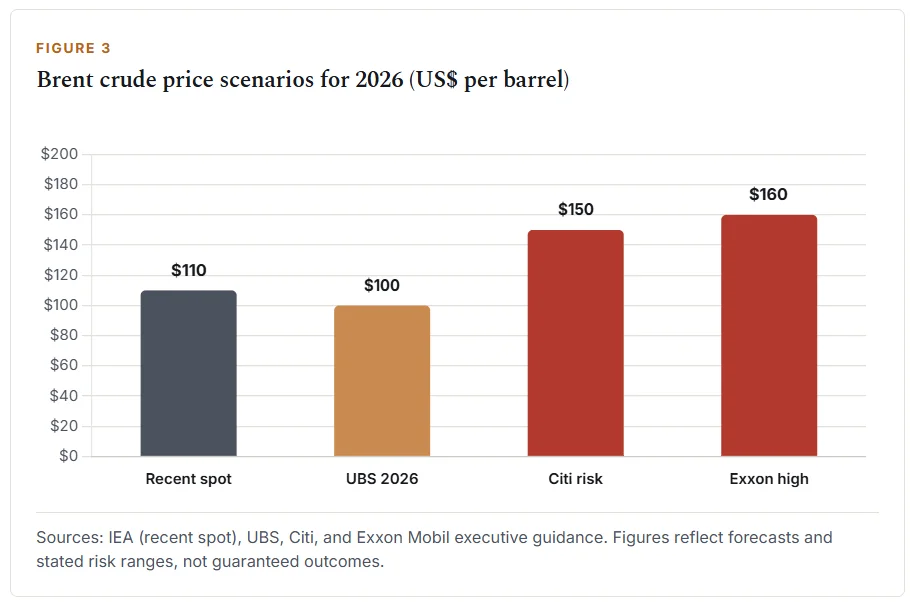

Exxon says Brent crude could reach $150 to $160 per barrel.

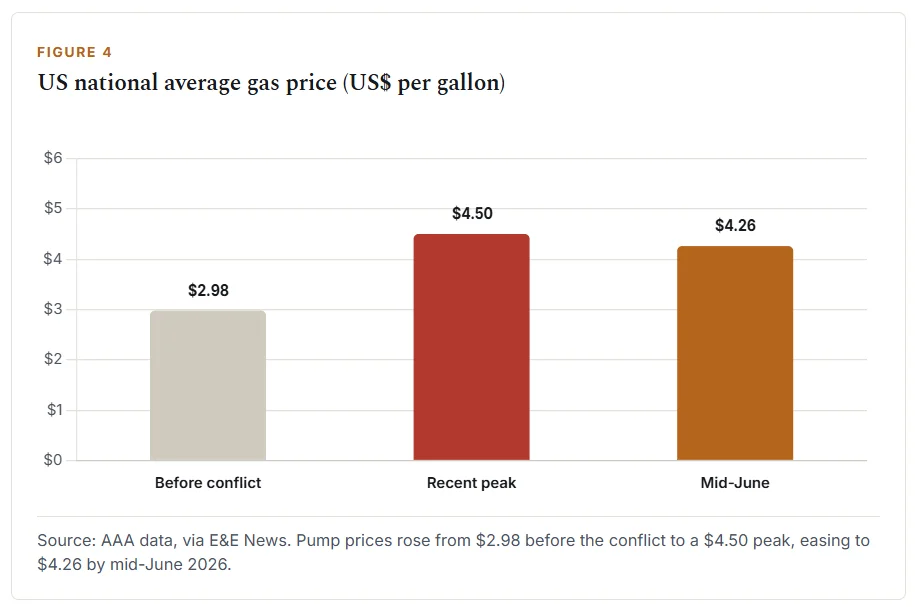

The national average gas price sits at $4.26, up $1.28 since the conflict began.

Oil executives have delivered a stark warning to American drivers. They say global petroleum inventories are running dangerously low. One industry leader described the situation simply as hitting “tank bottom”. Furthermore, that warning came with a specific deadline of mid-to-late June, according to E&E News.

Four oil executives reportedly raised these concerns with officials in Washington. Two of them have since repeated the message publicly. The White House, however, pushed back firmly. Administration officials said no such inventory discussions ever took place. Consequently, a sharp dispute now divides the industry and the government. The stakes in that disagreement are high. Pump prices touch nearly every household budget.

Inventory data shows a record drawdown

The roots of this squeeze trace back to the Strait of Hormuz. Iran effectively closed the waterway after US and Israeli strikes in late February. That strait normally carries about one-fifth of global oil supply. As a result, the world began burning through its stockpiles fast.

US gasoline inventories fell by 47.5 million barrels between early February and late May. Moreover, that marks the steepest February-to-May drawdown in federal records since 1990, according to OilPrice.com. Commercial crude stocks have also declined for several straight weeks. They now sit roughly 3% below the five-year average.

Global figures look just as severe. The International Energy Agency reported supply losses above 14 million barrels per day, according to the IEA. Therefore, the oil market remains in deficit heading into peak demand. Burkhard of S&P Global called the pace stunning.

The strategic reserve absorbs the strain

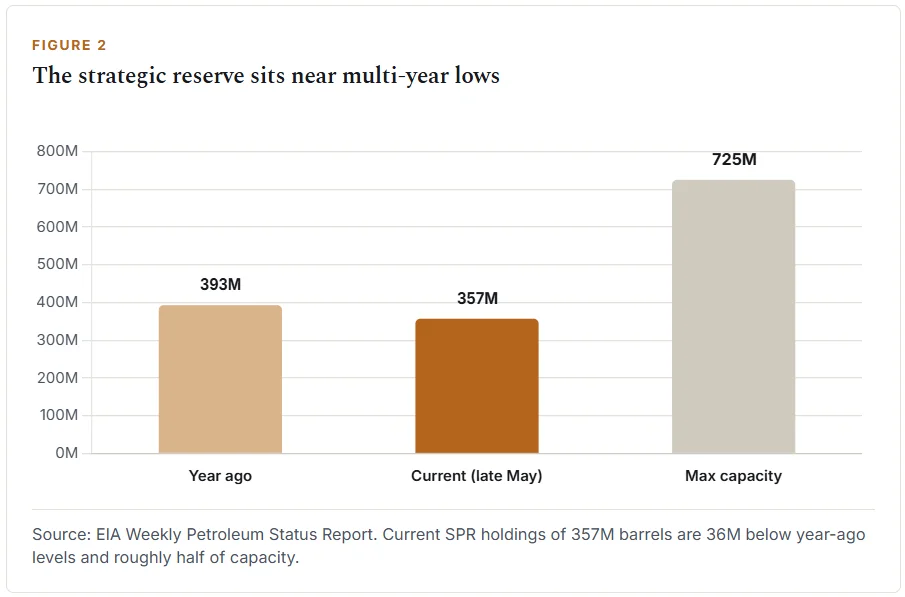

The Strategic Petroleum Reserve has cushioned much of the shock. SPR holdings fell to about 357 million barrels by late May. Notably, that level sits far below the reserve’s maximum capacity near 725 million barrels. Recent weekly withdrawals also rank among the largest ever recorded.

Analysts say the cushion alone has kept prices from spiking. However, that buffer cannot last forever. The federal EIA outlook echoes this tightening supply picture. Without fresh barrels, the margin for error keeps shrinking.

Brent forecasts point toward $150 oil

Named executives have now joined the warning. Exxon Mobil’s Neil Chapman told investors that Brent could reach $150 to $160 per barrel. He framed that figure as what the models imply once the cushion runs dry. Meanwhile, the American Petroleum Institute urged urgent action on the Strait of Hormuz.

Major banks share similar concerns. UBS expects Brent near triple digits for the rest of 2026. Citi has warned of $150 oil if Hormuz flows stay disrupted. Separately, Brookings analysts describe the event as a supply shock near 20% of global output, per Brookings. US oil output has stayed roughly flat near 13.6 million barrels per day. Therefore, domestic drillers cannot easily replace the lost imports.

Why the squeeze reaches beyond the pump

Higher crude prices rarely stay contained to gasoline. Instead, they feed quickly into transport, freight, and grocery costs. US consumer prices rose 4.2% in the year to May. That reading ranked among the hottest since 2023. Energy gains drove much of the increase. Consequently, the Federal Reserve has turned more cautious on rate cuts.

Diesel adds another layer of risk. Distillate stocks remain below normal for the season. Diesel powers trucking, rail, farming, and construction. As a result, tight supplies can ripple across the broader economy. Jet fuel on the West Coast faces a separate squeeze. That regional shortage never shows up in national gasoline averages.

The buffers have thinned on almost every front. Combined commercial crude and reserve stocks have dropped near 90 million barrels from their peak. Earlier in the crisis, the IEA coordinated one of its largest emergency releases ever. Even so, those barrels only slowed the slide. One strategist likened the drained tanks to an iceberg underwater.

Summer driving season raises the stakes

Timing makes this dispute especially urgent. The national average gas price stood at $4.26 in mid-June. That figure is $1.28 higher than before the conflict began. Prices have since eased from a recent peak near $4.50. Still, peak summer driving season is now arriving.

Higher demand now collides with the lowest inventories of the conflict. If Brent climbs toward Chapman’s range, pump prices would likely follow. GasBuddy has projected one of the most expensive summers at the pump in years.

What happens next

The core disagreement is not really about direction. Both sides accept that prices could rise. Instead, they clash over how loudly to warn the public. Executives argue that Americans deserve early preparation. By contrast, the administration says loud warnings risk a self-fulfilling spike.

The coming weeks should settle this debate. Both sides are watching the same mid-to-late June window closely. This fight also lands in a charged political season. Gasoline prices now sit near the top of the agenda. Both parties track the pump closely. Whichever view proves correct will shape what drivers pay all summer. For now, the data points firmly toward a tighter market.