May 01, 2026 – BNP Paribas holds a 12.8% CET1 ratio. Société Générale sits 320 basis points above its regulatory floor. Morgan Stanley says both lenders can weather tighter rules and still reward shareholders.

In Summary

Morgan Stanley reiterates a bullish stance. The broker backs BNP Paribas and Société Générale despite rising ECB regulatory capital requirements.

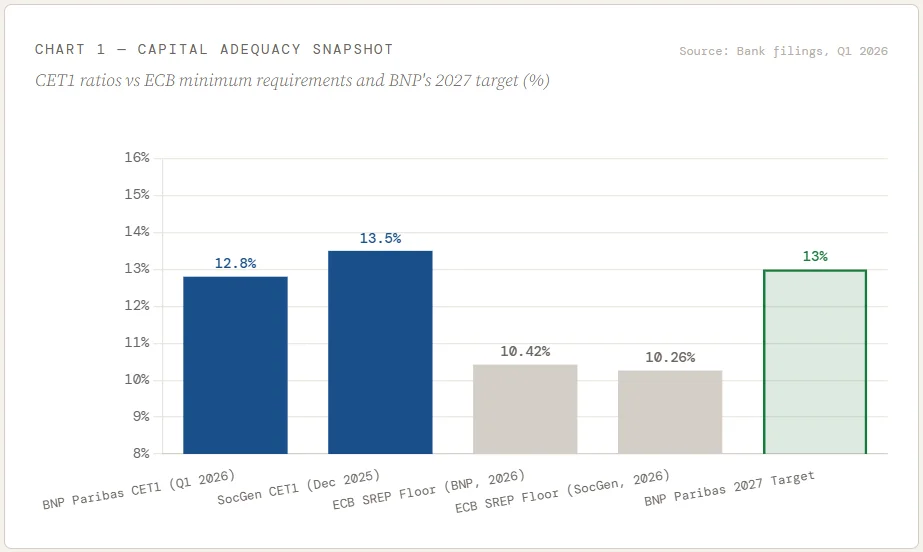

BNP Paribas’s CET1 reached 12.8% in Q1 2026, 238 basis points above the 10.42% SREP floor, with a 13% target by end-2027.

Société Générale’s CET1 stands at 13.5%, some 320 bps above its minimum. Record 2025 net income of €6.0bn rose 43% year-on-year.

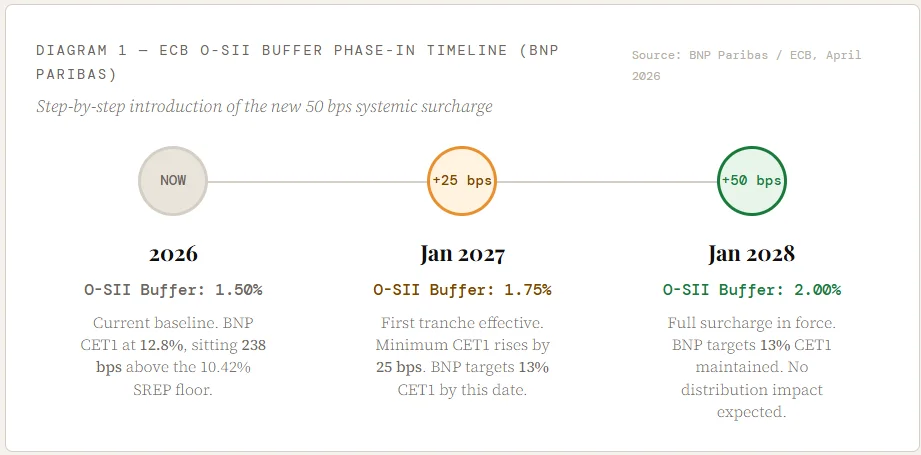

The ECB’s new O-SII surcharge adds 50 basis points to BNP Paribas’s capital requirement, phased in as +25 bps in January 2027 and +25 bps in January 2028.

Neither bank’s shareholder returns are at risk. Both confirmed no change to distribution or buyback policies following the ECB announcement.

Morgan Stanley has reaffirmed its positive view on France’s two largest listed banks. The Wall Street firm says BNP Paribas and Société Générale are well placed to absorb rising regulatory capital demands. Both lenders carry strong capital cushions. Both continue to grow earnings. And, crucially, neither looks likely to cut shareholder payouts.

The catalyst is the European Central Bank’s updated Other Systemically Important Institutions (O-SII) framework. Under this regime, the ECB assigns each major bank a systemic risk score. Higher scores mean higher mandatory capital buffers. For France’s biggest lenders, the new rules bite harder from 2027 onward.

What the ECB’s New O-SII Rules Mean

On 28 April 2026, the ECB published revised systemic buffer scores for eurozone banks. BNP Paribas received an O-SII score of 911 points, placing it in Bucket 8 of the ECB’s floor methodology.

The result is a new 2.0% O-SII buffer requirement, a 50-basis-point increase in CET1 capital demands. The rules phase in gradually. Twenty-five basis points take effect on 1 January 2027. A further 25 basis points follow on 1 January 2028.

The phased approach matters. It gives banks time to adjust without forcing sudden capital raises. Morgan Stanley views this as manageable. The broker sees no risk to dividend or buyback programmes.

BNP Paribas: Steady Capital Generation

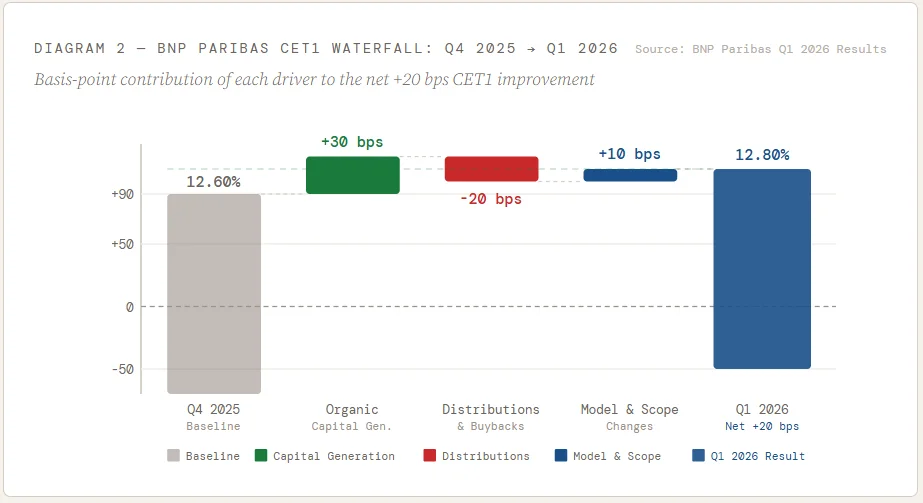

BNP Paribas enters this period from a position of strength. Its CET1 ratio reached 12.8% as of 31 March 2026, 20 basis points higher than at the end of 2025, and well above the SREP floor of 10.42%.

Organic capital generation contributed 30 basis points in Q1 alone. Distribution activity reduced the ratio by 20 basis points. Model and scope changes added a further 10 basis points.

“The bank targets a CET1 ratio of 13% by end-2027, even after absorbing the new O-SII surcharge.”

BNP Paribas said the ECB’s updated buffer requirement had already been factored into its capital trajectory. The bank confirmed that there was no impact on its leverage ratio or shareholder distribution policy. The 50-basis-point increase is spread over two years. BNP Paribas had anticipated this outcome well in advance.

Société Générale: Restructuring Pays Off

Société Générale tells a different, but equally compelling story. The bank ended 2025 with a CET1 ratio of 13.5%, roughly 320 basis points above its regulatory minimum. That is a substantial cushion.

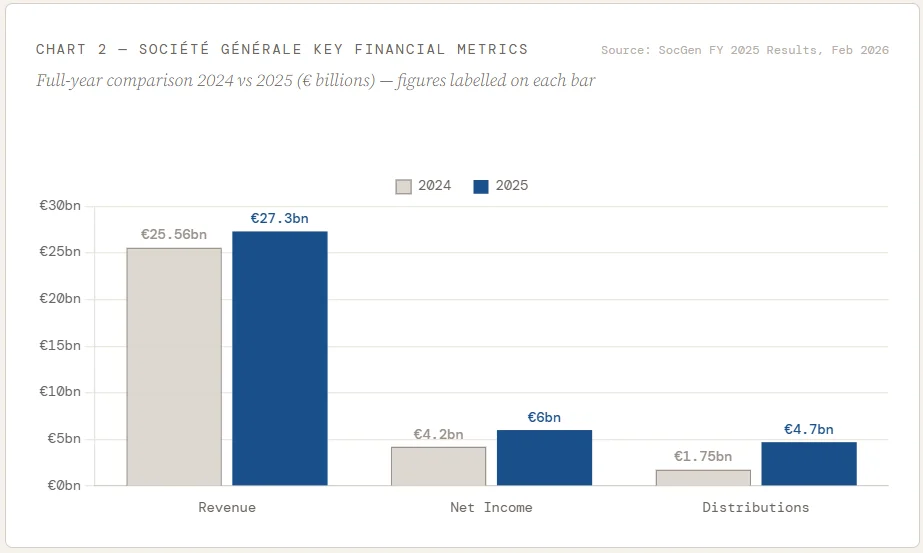

Full-year 2025 results reinforced the bank’s recovery narrative. Record revenues of €27.3 billion rose 6.8% year-on-year. Group net income surged 43% to €6.0 billion. Total shareholder distributions reached €4.7 billion, up 169% versus 2024.

Morgan Stanley views the bank’s ongoing restructuring as a credit positive. Costs fell 2.0% in 2025. The cost-to-income ratio dropped below 65%. The bank now targets a ROTE above 10% in 2026. Improving profitability cushions any incremental regulatory demand.

Why Morgan Stanley Is Bullish, And What Investors Should Watch

The analyst’s thesis rests on three pillars. First, both banks carry genuine capital surpluses. Second, earnings momentum is improving, not deteriorating. Third, the new O-SII rules are phased in slowly enough to avoid disruption.

That said, investors should monitor several risk factors. Macroeconomic deterioration in France could lift loan-loss provisions. A sharper-than-expected rise in risk-weighted assets would compress CET1 ratios. Political instability remains a background risk for French equities broadly.

Regulatory uncertainty is never fully resolved. The ECB could revise O-SII scores again in the coming years. Capital requirements across Europe are still moving targets. But for now, the trajectory favours the bulls.

BNP Paribas trades with a clear roadmap to 13% CET1 by 2027. Société Générale already exceeds that mark. Both banks are growing earnings, cutting costs, and returning cash to shareholders. For Morgan Stanley, the French banking sector is not a risk to avoid; it is an opportunity to seize.