June 26, 2026 – Every major U.S. lender cleared the 2026 exam. Within hours, the largest banks rushed to reward shareholders with fresh dividends and buybacks.

In Summary

All 32 large U.S. banks cleared the Federal Reserve’s 2026 stress test.

The system could absorb more than $708 billion in hypothetical losses.

JPMorgan launched a $50 billion buyback and a 10% dividend hike.

Goldman Sachs and Morgan Stanley also raised shareholder payouts.

This year’s results will not change banks’ capital requirements.

A clean sweep for the biggest lenders

The Federal Reserve handed Wall Street a confident verdict this week. Every one of the 32 large banks stayed above its minimum capital requirements. Moreover, the regulator said the system could keep lending through a deep recession.

The annual exercise measures how lenders cope with severe stress. Banks must hold enough high-quality capital to absorb heavy losses. This year, every firm cleared that bar with room to spare. As a result, several giants moved quickly to reward their investors.

The test springs from the 2010 Dodd-Frank law. That rule forces regulators to probe big bank resilience each year. JPMorgan ranks as the largest U.S. bank by assets. Its swift response, therefore, set the tone for rivals.

Inside the doomsday scenario

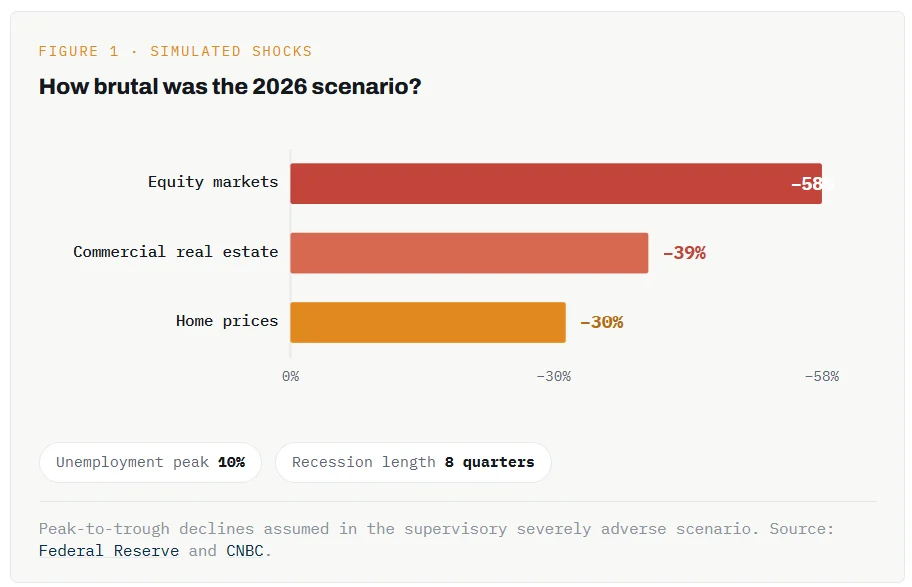

The Fed deliberately designed a harsh hypothetical recession. It assumed commercial real estate prices would crash 39%. House prices would tumble 30% during the same shock. Meanwhile, equity markets would sink sharply as output shrank.

These assumptions sit near the top of the Fed’s historical range. Therefore, passing the exam signals real balance sheet strength. The scenario remained broadly as severe as last year’s.

The shock also ran across eight straight quarters. In effect, the model simulated a long and grinding slump. Such depth makes the clean result more striking. Banks rarely face this scale of pressure in real life.

Where does the $708 billion in losses land

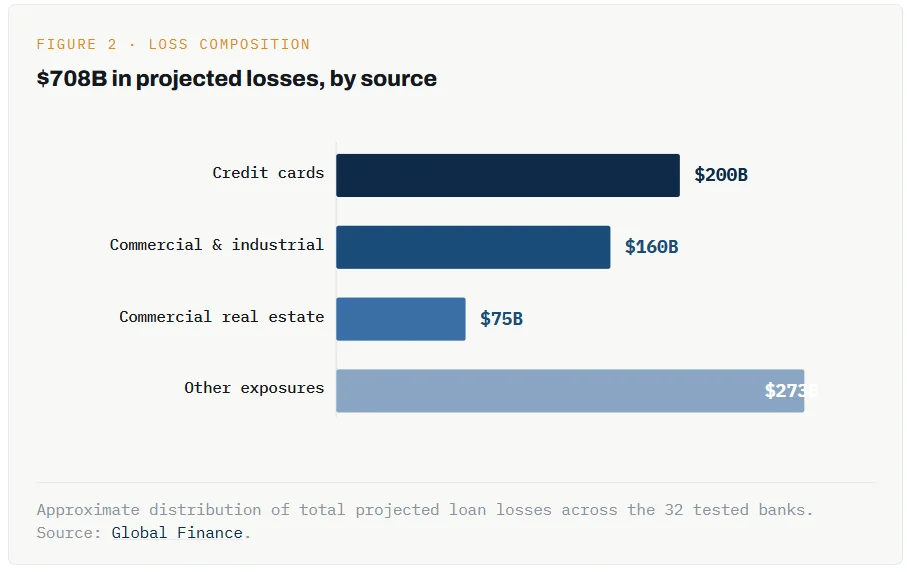

Under that stress, the 32 banks would book more than $708 billion in projected losses. Credit cards accounted for the largest share, at roughly $200 billion. Commercial and industrial loans added about $160 billion more. Furthermore, commercial real estate contributed close to $75 billion.

The rest of the damage spread across mortgages and trading books. Even so, the banks absorbed the blow and stayed standing. That outcome reinforced the regulator’s message about resilience.

Credit cards topped the list for a clear reason. Consumer borrowing tends to sour fast in a downturn. Business loans followed as defaults climbed within the model. Property loans rounded out the three biggest pain points.

Capital cushions held firm

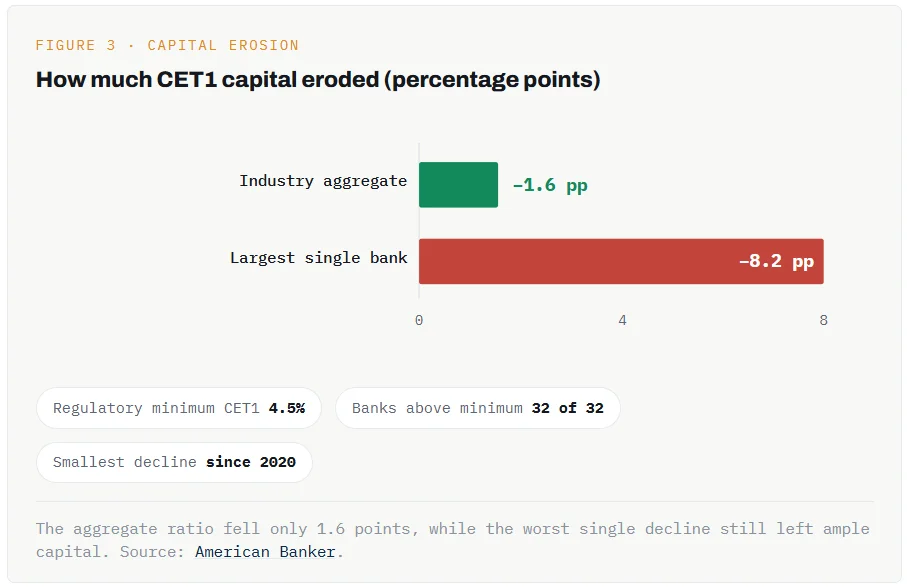

Capital strength sits at the heart of the Fed stress test. The industry’s aggregate common equity tier 1 ratio fell just 1.6 percentage points. Notably, that drop marked the smallest decline since the framework’s 2020 overhaul. Every bank also stayed comfortably above the 4.5% minimum.

Today’s results underscore the strength of the banking system.

-Michelle Bowman, Fed Vice Chair for Supervision

Even the weakest performer kept a healthy buffer. Deutsche Bank’s U.S. unit posted the largest capital decline. Consequently, markets treated the whole report as a vote of confidence.

What moved the numbers this year

The Fed pointed to three forces behind the 2026 figures. First, larger loan balances pushed projected losses higher. Second, smaller assumed rate declines trimmed gains on securities. However, stronger interest income offset much of that pressure.

Recent bank earnings clearly fed into the result. Still, six lenders scored slightly worse than in 2025. Custodial banks such as State Street saw modest setbacks, too. These shifts stayed small against the sector’s wide cushions.

Banks reward shareholders fast

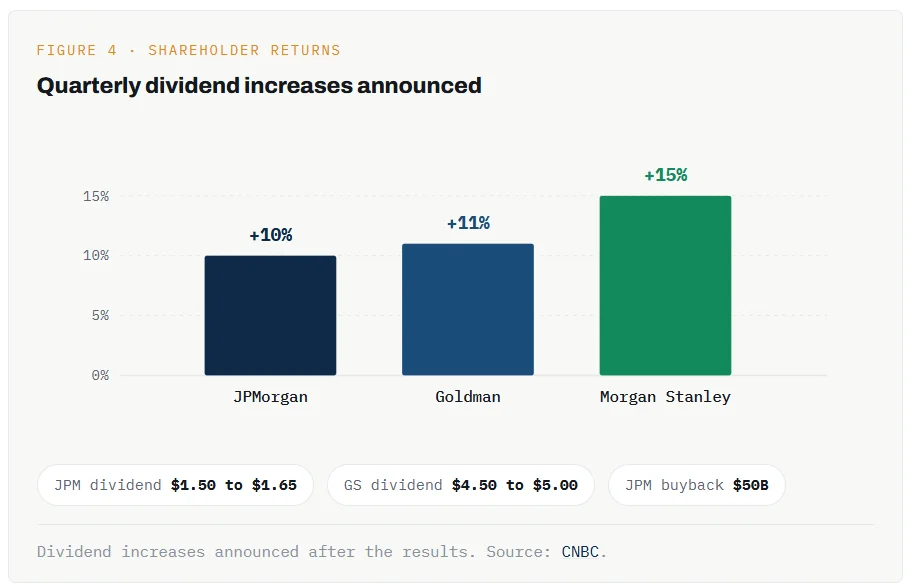

JPMorgan acted within hours of the release. The bank authorized a new $50 billion share repurchase program. It also plans to lift its quarterly dividend 10% to $1.65. That buyback takes effect on July 1, pending board approval.

Rivals quickly followed JPMorgan’s lead. Goldman Sachs raised its dividend 11% to $5 per share. Morgan Stanley went furthest and boosted its payout 15%. All three cited strong earnings and solid capital positions.

Chief executive Jamie Dimon welcomed the dividend plan. He tied the move to steady investment and strong results. The buyback also gives JPMorgan flexibility on future capital. Bank shares then ticked higher in after-hours trading.

The transparency battle behind the test

A quieter dispute shapes this year’s exam. In late 2024, big banks sued the Fed over the process. They demanded more insight into the models and scenarios. Since then, the Fed has offered early previews and feedback.

Bowman has also pledged to curb wild swings in results. Critics warn the changes could soften the test. Some describe the new approach as an open-book exam. Supporters counter that clearer rules build lasting trust.

Why does this year’s test carry less weight?

This round arrived with an unusual twist. Unlike past years, the results will not reset capital requirements. The Fed froze stress capital buffers back in February. Those buffers will now stay fixed through 2027.

Regulators are also rewriting the testing methodology. They want more transparency and fewer wild swings in outcomes. Therefore, banks already knew their capital rules this week. Analysts at KBW even called the exercise “going through the motions.”

What comes next

The bigger fight still sits further ahead. Investors are now watching the pending Basel III Endgame proposal. That rule could reshape how much capital banks must hold. Until then, strong results give lenders room to spend.

For now, the message reads simple and upbeat. The largest U.S. banks look sturdy under heavy pressure. They also feel confident enough to return billions to investors. The next Fed stress test will test that confidence again.

For investors, the result offers a clear signal. Healthy buffers usually point to steadier payouts ahead. Buybacks can also lift earnings per share over time. Yet the $708 billion figure still demands real caution.