May 01, 2026 – Oil briefly touched $130 a barrel. Central banks in Frankfurt and London are now edging toward tightening. Here is what the data reveals about Europe’s stagflation risk.

Europe’s two most powerful central banks are under pressure. The European Central Bank (ECB) and the Bank of England (BOE) are now signalling a hawkish turn. Energy prices sparked by the Middle East conflict are the driving force. A potential rate hike as early as June is now on the table.

According to the International Energy Agency (IEA), North Sea Dated crude briefly traded near $130 a barrel. That is $60 above pre-conflict levels. The scale of the oil supply shock is historic. The IEA estimates an initial loss of about 10 million barrels per day in global supply.

The Hawkish Pivot

Both central banks held rates steady at their most recent meetings. But the tone is shifting fast. CNBC reports that markets are pricing nearly 40 basis points of BOE tightening by year-end. For the ECB, money markets now price in more than two quarter-point hikes in 2026.

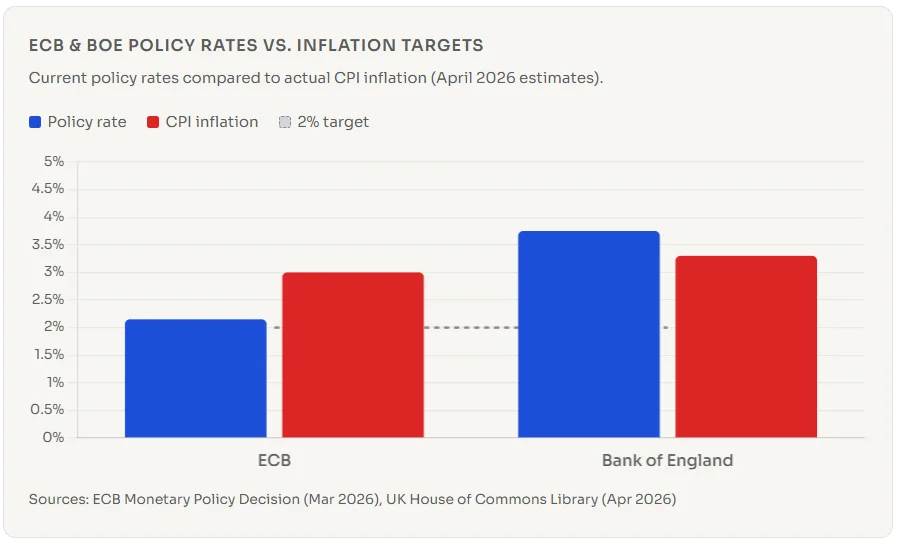

The BOE’s current rate stands at 3.75%. The ECB’s main refinancing rate sits at 2.15%. The UK House of Commons Library confirms that pre-conflict rate cuts are now firmly off the table. Hikes are now a real possibility.

“The question is not whether inflation will rise. The dilemma is whether tightening policy to ensure a swifter return to 2% is worth the estimated loss in growth.”

— Morgan Stanley economists

The Stagflation Threat

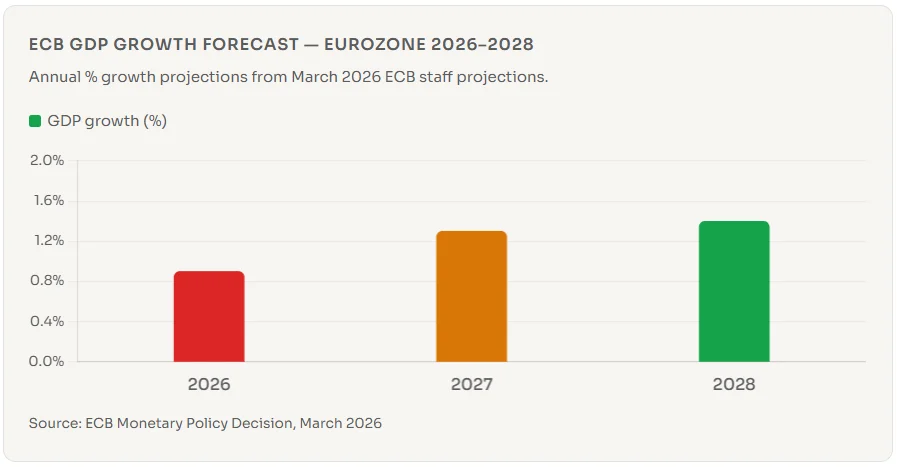

The energy shock is not just about prices. It is also squeezing growth. The ECB’s own projections now show GDP growth of just 0.9% for 2026. That is a sharp downward revision. Meanwhile, eurozone inflation is projected at 2.6% for 2026, well above the 2% target.

The eurozone economy expanded only 0.1% in Q1 2026. This near-stagnation feeds fear of a stagflationary scenario. Higher inflation and weak growth present a classic central bank dilemma. Raising rates fights inflation but risks deepening the slowdown.

The UK faces the same bind. The House of Commons Library warns that household gas bills are likely to rise further in late 2026. Petrol prices have already climbed sharply. CPI is now expected to stay between 3% and 3.5% through Q2 and Q3. That is materially above the BOE’s 2% target.

The Energy Shock in Numbers

The World Bank’s April Commodity Markets Outlook puts the crisis in stark context. Global energy prices are projected to surge by 24% in 2026. That is the highest level since Russia’s invasion of Ukraine in 2022. Overall commodity prices are forecast to rise 16%.

The Strait of Hormuz is the flashpoint. It handles roughly 35% of the global seaborne crude oil trade. Attacks on shipping and energy infrastructure triggered a record oil supply shock. Physical crude prices surged to near $150 a barrel at peak, far above futures markets.

World Bank Chief Economist Indermit Gill framed the danger clearly. “The war is hitting the global economy in cumulative waves,” he said. Higher energy prices lead to higher food prices. Then come higher interest rates. Then, the more expensive debt. It is a compounding crisis.

What Comes Next?

A June rate decision remains uncertain. Most economists do not yet call it a done deal. Oxford Economics warns that energy prices are “not far enough above ECB forecast assumptions” to force immediate action. A short conflict could change the calculus entirely.

But the signals are clear. Both the ECB and the BOE are closely watching second-round effects. If workers demand higher wages in response to rising prices, that embeds inflation. That is the scenario that could push policymakers to act sooner rather than later.

For markets, the message is already landing. Bond yields in both the UK and the eurozone have risen. Mortgage rates in the UK jumped sharply through March. The financial system is repricing for a world of higher-for-longer rates, even before a single hike is delivered.