June 25, 2026 – Lawmakers back the ECB framework, setting up a 2027 pilot and a possible 2029 launch for Europe’s public digital money.

In Summary

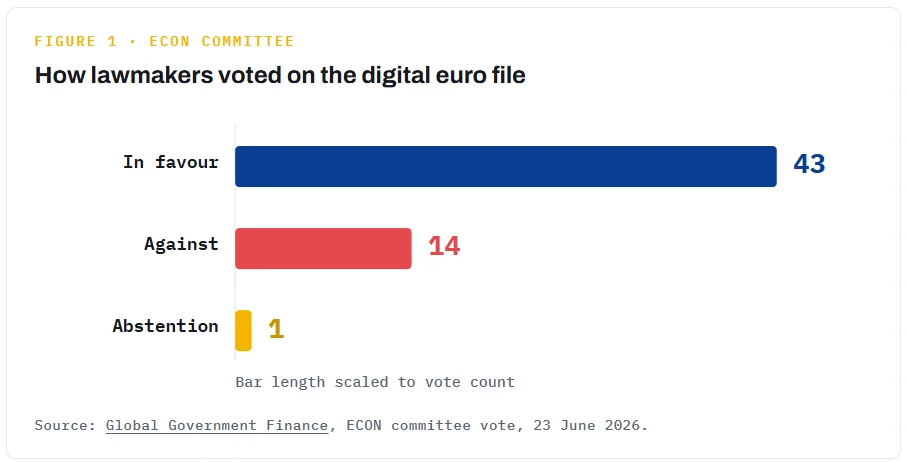

The European Parliament’s economic committee backed the digital euro by 43 votes to 14.

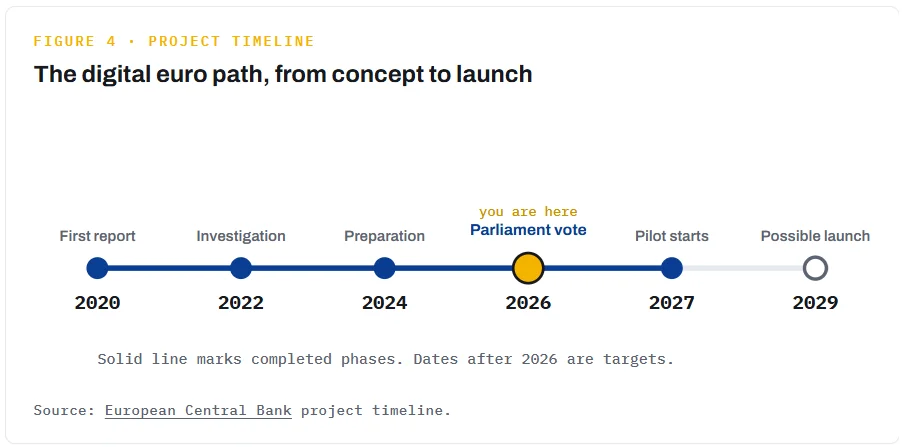

The ECB plans a 12-month pilot from mid-2027, with a possible launch in 2029.

A proposed holding cap of €3,000 aims to shield commercial bank deposits.

Europe wants to cut its reliance on Visa and Mastercard for everyday payments.

Europe moved closer to its own digital cash this week. On Tuesday, the European Parliament’s economic committee backed the legal framework for a digital euro. The vote ended three years of friction between the European Central Bank and commercial banks. Moreover, it opened the door to final negotiations on the law.

A vote three years in the making

The Economic and Monetary Affairs Committee adopted its position on 23 June. Lawmakers approved the digital euro file by 43 votes to 14, with one abstention. French lawmaker Aurore Lalucq chairs the panel that steered the package. Her committee now sends the text into trilogue talks with member states. Therefore, the project clears its toughest political test so far. The bill still faces debate before it becomes law. Even so, the direction of travel now looks clear.

Why Europe wants its own payment rail

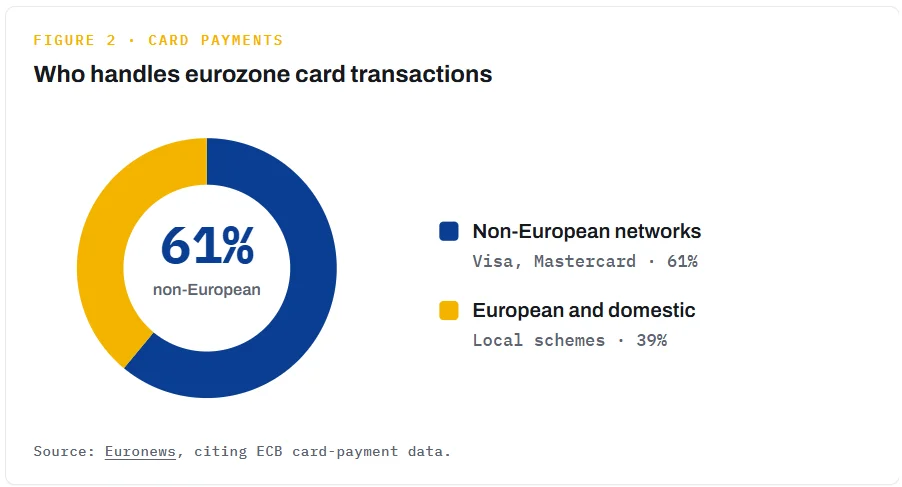

Officials frame the digital euro as a question of sovereignty. Today, non-European firms handle most card payments across the euro area. Visa and Mastercard sit at the heart of that system. In fact, they process about 61% of eurozone card payments. Furthermore, 13 of the 21 eurozone countries lack a national card scheme. EU lawmaker Markus Ferber called payment resilience a “geopolitical necessity”. Trade tension with Washington has sharpened that worry. In 2025, US sanctions even cut a French judge off from his Visa card. Such cases turned an abstract risk into a concrete one.

We can no longer accept that digital payments are largely dependent on a few foreign providers.

-Markus Ferber, ECON committee member

The numbers worry policymakers across the bloc. Card payments make up roughly 56% of cashless transactions in the EU. Each tap can send data outside the European jurisdiction. ECB President Christine Lagarde has called the gap urgent. Consequently, payments now rank beside energy and defence as a strategic concern.

How the digital euro would work

The digital euro would behave like an electronic wallet. The central bank would guarantee it, while banks and fintechs would distribute it. Users could pay online and in person. An offline mode would copy the privacy of cash. In that mode, the ECB could not see what citizens buy. In addition, a holding cap would limit how much each person keeps. Regulated crypto firms could also distribute the currency. Basic services, such as opening a wallet, would stay free. Merchant fees would be capped below current card charges.

The fight over the price tag

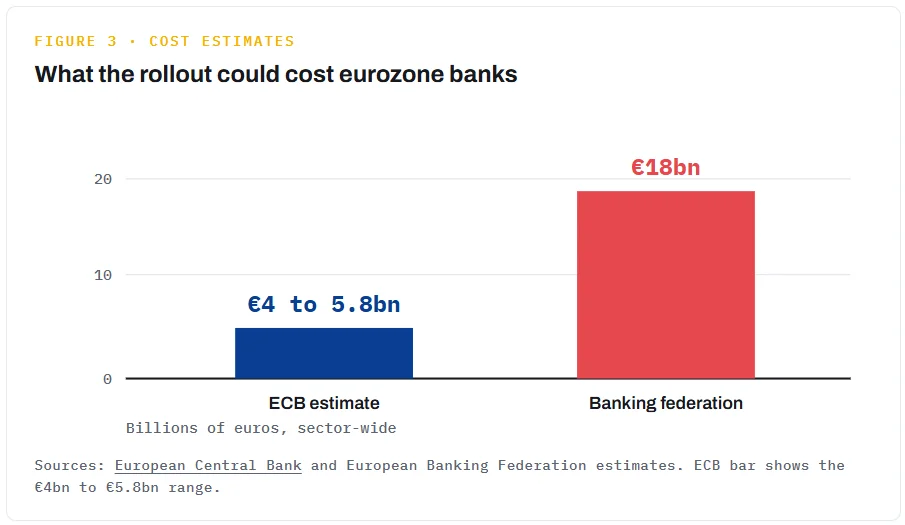

Banks still worry about cost and lost deposits. The European Banking Federation estimates the sector bill at €18 billion. However, the ECB puts the figure far lower. Its own analysis points to between €4 billion and €5.8 billion. Co-legislators asked the ECB to test holding limits up to €3,000 per person. Even at that cap, deposit outflows would stay below 2% of retail deposits. Crucially, these balances would earn no interest. A “waterfall” feature would also link wallets to a bank account. Payments above the cap would then automatically draw on that account.

Piero Cipollone framed the cost as small for lenders. He put it at about 3% of annual bank IT spending. Merchants, meanwhile, would save on capped transaction fees. The ECB itself faces a setup bill of nearly €1.3 billion. Running costs would then add roughly €300 million each year.

Industry pushback remains

Not everyone in finance welcomes the plan. Banks fear competition for Wero, their own payment app. Some warn that the digital euro duplicates private services. Others question its added value for ordinary consumers. These objections now move into the trilogue debate. Supporters counter that public money needs to be in digital form.

What happens next

Trilogue talks now begin between the parliament, the governments and the Commission. EU leaders want the law agreed before the end of 2026. After that, the ECB plans a 12-month pilot starting in 2027. A first issuance could follow in 2029. Notably, Europe moves as the United States restricts a Fed digital dollar. The two blocs now head in opposite directions. Stablecoins add further pressure on policymakers, too. A digital euro would give Europe a public answer.

For now, the project still depends on a final political deal. Negotiators face hard questions on privacy, fees and bank stability. Yet the committee vote gives the plan real momentum. The next test arrives when the trilogue talks open in Brussels.