May 30, 2026 – The bank’s strategists now expect the 10-year US Treasury yield to stay elevated through 2026. The Fed under new Chair Kevin Warsh is seen as done cutting rates, reshaping the bond market outlook.

In Summary

Deutsche Bank raised its 10-year US Treasury yield forecast for end-2026

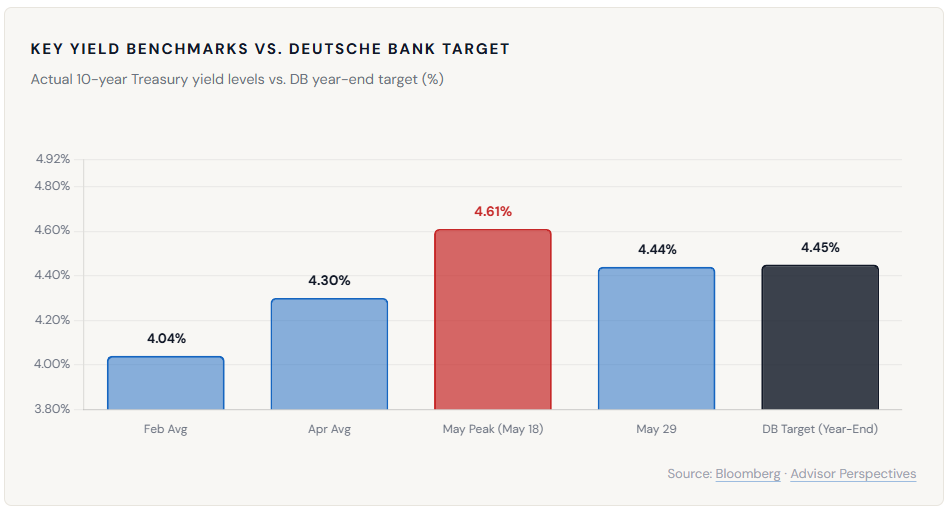

The bank recommends shorting Treasuries, targeting a yield of 4.45% with a stop at 3.90%

Fed Chair Kevin Warsh is expected to hold rates steady or hike, ending the easing cycle

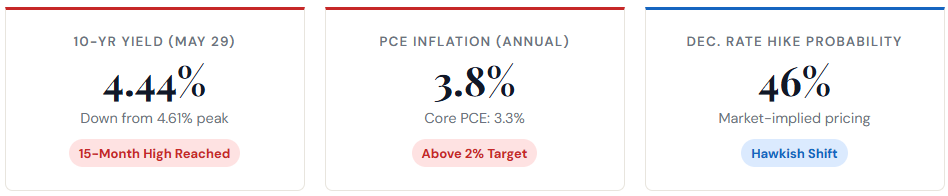

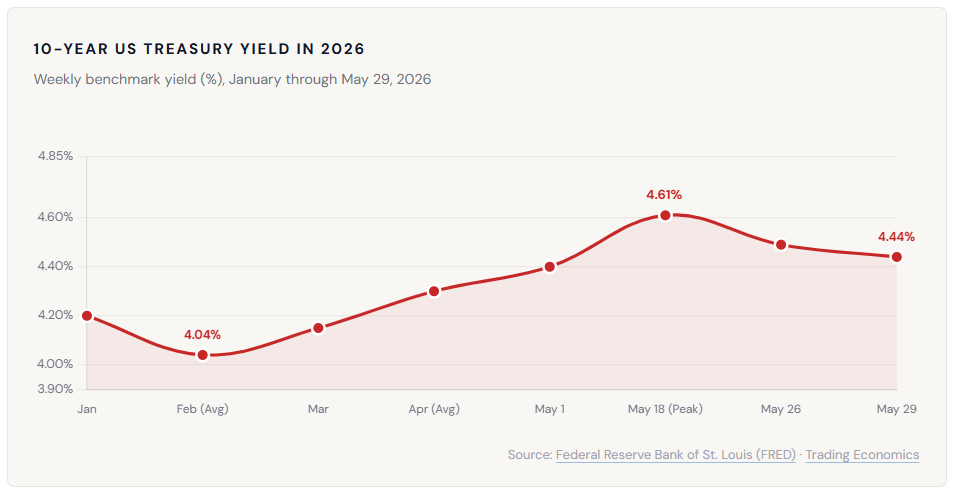

The 10-year yield hit 4.61% on May 18 – a 15-month high – before easing to 4.44%

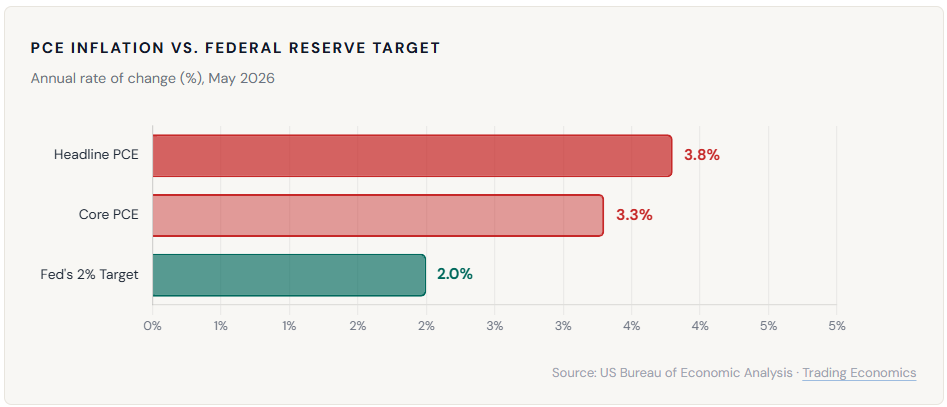

Annual PCE inflation runs at 3.8%, far above the Fed’s 2% target

Markets now price in a 46% probability of a Fed rate hike by December 2026

Deutsche Bank raised its forecast for the 10-year US Treasury yield this week. The bank’s interest-rate strategists now expect yields to remain elevated through year-end. This revision reflects a fundamental shift in Federal Reserve leadership and direction.

What Deutsche Bank Is Saying

Interest-rate strategists at Deutsche Bank AG boosted their year-end Treasury yield target. The revision followed a clearly hawkish turn in the Federal Reserve’s outlook. Furthermore, the bank formally recommended shorting Treasury bonds at current levels. Strategists set a yield target of 4.45% and a protective stop-loss at 3.90%.

Francis Yared leads Deutsche Bank’s rates strategy team. His team pointed to strong credit survey data as a primary driver. The Senior Loan Officer Opinion Survey (SLOOS) delivered encouraging results. Bank willingness to extend consumer loans rose to the highest level since 2022. Moreover, mortgage demand grew for the first time since 2021.

These results indicate that the US economy can absorb higher borrowing costs. Therefore, Deutsche Bank views the Fed’s policy pause as sustainable. The strategists believe US growth remains close to its long-run potential. This makes a near-term rate cut from the Fed unlikely.

Kevin Warsh and the New Fed Regime

Kevin Warsh officially became Federal Reserve Chair in May 2026. He replaced Jerome Powell at a critical moment for US monetary policy. Warsh carries a long-established reputation as an inflation hawk. His nomination by President Trump in January 2026 immediately rattled global bond markets.

Warsh openly called for a “regime change” at the central bank. He proposed rethinking how the Fed manages its large balance sheet. Additionally, he moved away from the detailed forward guidance that Powell favored. This new approach has introduced significant uncertainty into fixed-income markets worldwide.

The market’s reaction to Warsh’s leadership was swift and decisive. As CNBC reported, his plans to reshape the Fed’s operational framework could affect Treasury yields, mortgage rates, and broader borrowing costs. The 10-year Treasury yield surged to 4.61% on May 18, 2026. This was the highest level in 15 months.

The 30-year bond yield also climbed sharply to 5.133%, approaching a one-year high. Deutsche Bank’s revised forecast directly aligns with this new market reality. Bond investors now face an environment with less policy predictability and sustained upward pressure on yields.

Inflation Gives the Fed No Easy Exit

Inflation data offers the Fed little justification for easing interest rates. The Personal Consumption Expenditures (PCE) index showed 3.8% annual inflation in the latest reading. Core PCE, which excludes food and energy prices, came in at 3.3% year-over-year. Both figures remain well above the Fed’s stated 2% target.

However, both monthly PCE readings came in below market expectations. This provided modest relief to bond markets on May 29. The 10-year yield pulled back to 4.44% on that day. Still, the annual figures remain stubbornly elevated. Therefore, the Fed has little political or economic room to cut rates before year-end.

The federal funds rate currently sits in the 3.5% to 3.75% range. Investors expect rates to remain in this band well into 2027. This marks a sharp reversal from expectations of multiple cuts in 2026. Consequently, bond markets have had to rapidly reprice their outlook for the year ahead.

The SLOOS data is consistent with the US growing at or slightly below potential. The economy shows no sign of distress that would justify a rate cut.

-Deutsche Bank Rate Strategy Team (paraphrased via Bloomberg, May 29, 2026)

Market Implications and Investor Strategy

Markets have fully absorbed the Federal Reserve’s hawkish shift. Investors now assign a 46% probability to a rate hike by December 2026. This reflects a dramatic reversal from earlier dovish expectations. Furthermore, pricing for rate cuts has essentially disappeared from market forwards.

Higher Treasury yields ripple across all major asset classes simultaneously. Mortgage rates, corporate bond spreads, and equity valuations all feel sustained upward cost pressure. However, resilient credit conditions provide some comfort to market participants. Banks remain willing to lend, and consumer demand for credit stays firm.

Bond investors face a particularly challenging environment. Deutsche Bank recommends shorting Treasuries near current levels. Floating-rate assets may outperform traditional fixed-rate bonds in this climate. Short-duration strategies also offer better protection against further yield increases.

Equity investors are also affected. Higher yields raise the cost of capital for all companies. Growth stocks with distant cash flows face greater valuation pressure than value stocks. However, financial sector firms may benefit from wider net interest margins in a sustained high-rate environment.

The Yield Curve Tells the Story

The shape of the yield curve reveals important market dynamics. The 10-year yield at 4.44% sits significantly above the 2-year yield of around 4.07%. This “bear steepening” pattern signals that investors expect inflation to stay elevated for longer. Moreover, it reflects a growing risk premium for holding longer-dated US debt.

Bear steepening often signals concern about fiscal sustainability. The US government continues to run large deficits, requiring heavy Treasury issuance. Historical data from Advisor Perspectives shows the 10-year yield rose from 4.04% in February to 4.61% by mid-May 2026. This near-60-basis-point surge in three months reflects a substantial shift in investor sentiment.

The Bottom Line

Deutsche Bank’s revised forecast sends an unmistakable signal to fixed-income markets. The Fed rate-cutting cycle appears to be over, at least for now. Chair Kevin Warsh is unlikely to ease policy while inflation stays well above target. Furthermore, strong credit demand gives the Fed confidence to hold rates steady.

Investors should monitor several key indicators closely in the weeks ahead. First, the next PCE reading will test whether the monthly softness continues. Second, Chair Warsh’s public commentary will guide market expectations. Third, the shape of the yield curve will signal whether the bear steepening trend is deepening. The next FOMC meeting will be the critical checkpoint for all three.